Credit-Market Cracks Emerge as Delta Strain Sows Reopening Angst

Credit-Market Cracks Emerge as Delta Strain Sows Reopening Angst

(Bloomberg) -- Strong corporate earnings have sent stocks on something of a tear in recent weeks. But credit markets are painting a more nuanced picture amid growing concerns of a coronavirus resurgence.

Less than a month removed from the tightest spreads of the post-financial crisis era, risk premiums for speculative-grade debt are climbing once again. Bonds of companies hurt most by shutdowns have sold off, including American Airlines Group Inc. and Staples Inc. The amount of distressed debt has even started to creep up, though defaults remain far below levels seen earlier in the pandemic.

Market watchers are divided on what it all means. Some, like Aristotle Credit Partners’ Douglas Lopez, say it’s an overdue correction.

“The market got ahead of itself in pricing in the reopening trade and continued economic strength, especially in lower quality and cyclical names whose profitability is the most sensitive to this changed outlook,” Lopez said.

Yet others, including Amundi US’s Ken Monaghan, aren’t so sure.

“What we’re seeing right now is a temporary phenomenon that relates to the markets having some questions about the delta variant and what its impact will be between now and the end of the year,” said Monaghan, a portfolio manager whose firm oversees more than $90 billion.

He expects the softness in credit markets to be fleeting as more people in the U.S. get vaccinated. “There’s a very good chance that high-yield spreads will revisit the lower levels that they had seen earlier this year,” Monaghan added.

The average spread on junk-rated bonds hit a low of 2.62 percentage points on July 6, a level not seen since 2007, and has mostly widened since, according to Bloomberg Barclays index data.

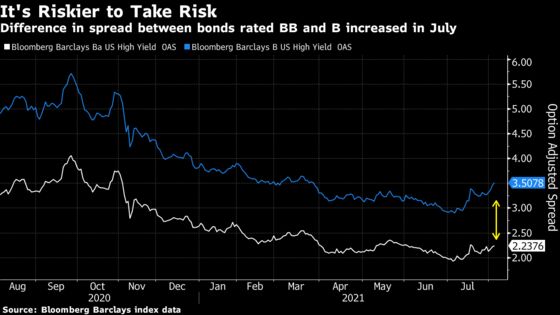

The difference in spreads between double-B rated companies -- considered the safest junk bonds -- and those rated a tier lower, or single-B, has also widened significantly. The gap expanded 26 basis points over the past month, the most since February. Investors who piled into CCC rated bonds, the riskiest tier, lost money last month for the first time in over a year, reflecting the increased risk of buying lower-quality bonds, which are more likely to be disrupted by any delay to the economic recovery.

The market firmed up Friday and spreads tightened for the first time in a week. U.S. employers added the most jobs in nearly a year, a Labor Department report showed. But companies such as BlackRock Inc. and Wells Fargo & Co. are delaying their return-to-office plans, calling into question just how quickly things will get back to normal.

Worsening sentiment is already impacting the ability of companies to tap markets at the terms they want. Multiple leveraged loans have had to up -- or “flex” -- their pricing wider in recent days, including a high-profile dividend deal by Standard Industries Holdings Inc. and a term loan from auction house Sotheby’s.

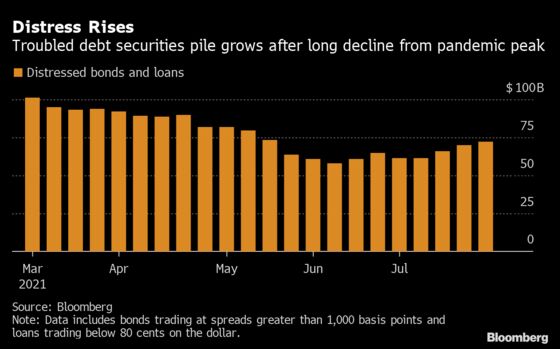

These wobbles in debt markets caused the amount of distressed bonds and loans to increase to about $72.5 billion as of Aug. 4, a nearly 25% jump over the one-year low of about $58 billion reached in early June, according to data compiled by Bloomberg. Even certain bonds of day-trader favorite AMC Entertainment Holdings Inc. are once again trading at spreads of over 10 percentage points, though those spreads remain well off their highs of the past year.

Read more in this week’s brief: Credit Markets Show Signs of Cracking

Some say increasing credit stress in China, the second-largest U.S. dollar corporate bond market in the world, is also weighing heavily. Investors have grappled with the fall-out from property company China Evergrande Group, the world’s most indebted developer, as it struggles to reassure money managers that it can make good on its debts. China’s escalating crackdown on industries from technology to education has also made investors nervous.

Despite the recent jump in troubled debt, large bankruptcy filings remain slow, helped by accommodative Federal Reserve policies that have allowed all but the riskiest companies to shore up their cash reserves. The rate of high-yield bond defaults could fall as low as 1% by year-end, a mark not seen since 2013, Fitch Ratings said last month.

Still, the recent tumult could also signal more credit weakness ahead.

“Just when people thought the economy was going to be turning back on full steam, it’s now hesitating,” said Phil Brendel, a distressed debt analyst at Bloomberg Intelligence. “That clearly can lead to accelerated depletion of cash hoards, and some companies might throw in the towel. There is higher risk of that.”

U.S.

No companies launched sales of U.S. investment-grade bonds on Friday. Estimates for next week stand at $25 billion to $30 billion, and dealers say Monday may see borrowers number in the double digits, according to an informal survey of debt underwriters.

- In high yield, Bally’s Corp. is in line to price a $1.5 billion bond offering Friday, and Infrastructure and Energy Alternatives Inc. is also on the day’s docket after setting talk on $300 million of eight-year debt

- In leveraged loans, SeaWorld Parks & Entertainment Inc. launched a deal to refinance debt, and International SOS, a provider of health and security services to corporate and government employees, had to increase pricing on a loan that will refinance debt and fund an acquisition

- For deal updates, click here for the New Issue Monitor

- For more, click here for the Credit Daybook Americas

Europe

Credit spreads are tightening for the second straight day and heading for a weekly decline, the Markit iTraxx Europe index shows. Commerzbank strategists reined in their spread targets once again this year, with updated ECB guidance pushing back the timeline for QE tapering.

- It’s a quiet day in Europe’s primary market, which is heading for the eighth zero-sales day of the year. Things will accelerate next week as Becton, Dickinson & Co. begins calls on Monday about a four-part euro deal

- Europe’s CLO market continues to be active. After a record month for new issuance in July, two new deals have priced this week in the region. The activity brought volumes for new CLOs this year to 20.7 billion euros ($24.5 billion), according to data compiled by Bloomberg

- Neuberger Berman Europe Ltd. priced its 306.3-million euro Neuberger Berman Loan Advisers Euro CLO 2 on Thursday. Triple-A spreads printed at 103 basis points over Euribor

Asia

No issuers marketed offerings or hired banks for potential sales Friday.

- Note sales in Asia excluding Japan fell to $3.7 billion this week from $5.6 billion a week earlier, the lowest issuance since the period ended June 18, according to Bloomberg-compiled data

©2021 Bloomberg L.P.