Credit Liquidity Risk Is Rising Thanks to Boom in Bond ETFs

Credit Liquidity Risk Is Rising Thanks to the Boom in Bond ETFs

(Bloomberg) -- Plenty on Wall Street fear the explosive growth of passive investing will eventually store up trouble for bond portfolios. An academic from the Swiss Finance Institute has found evidence it has already begun.

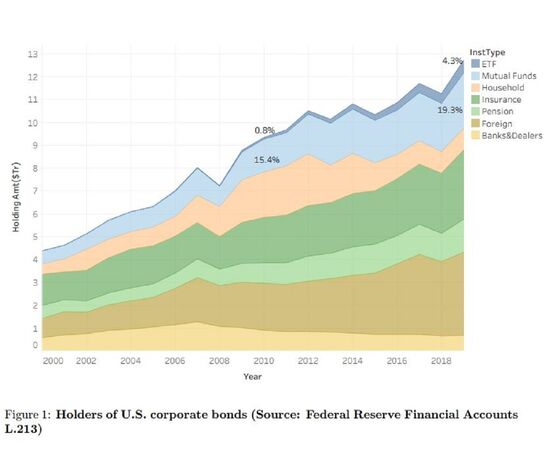

After dissecting more than 10,000 corporate bonds, Efe Cotelioglu found that high-grade securities share similar liquidity characteristics when they are heavily owned by exchange-traded funds.

That means in any market shock, fleeing investors could face the same difficulties exiting positions across all of them. To ETF critics, it’s a scenario that played out in this year’s pandemic-triggered turmoil -- until the Federal Reserve’s unprecedented intervention brought everything under control.

“Higher ETF ownership of investment-grade corporate bonds can reduce the ability of investors to diversify liquidity risk,” Cotelioglu, who is also a PhD candidate at the University of Lugano, wrote in a paper.

The ease with which bonds can be traded is a hot-button issue thanks to the drama caused by the coronavirus. Treasury liquidity suffered a shock collapse, while huge gaps emerged between the prices of ETFs and the bonds they track. Only the Fed’s action restored calm.

That return to normalcy persuaded many that concern about the viability of bond ETFs were misguided. The fear was that very liquid funds could become a destabilizing force for their less liquid underlying securities.

Cotelioglu found an “economically and statistically significant” difference between the co-movement of liquidity in investment-grade bonds in the top-quartile of ETF ownership and those in the bottom quartile. The pattern didn’t occur in high yield.

The research showed no relationship between so-called commonality of liquidity and mutual fund ownership. Cotelioglu puts this down to contrasting investor bases and structural differences. For instance, mutual funds have “discretion” in deciding how to meet redemptions, while an ETF can’t choose what assets it sells.

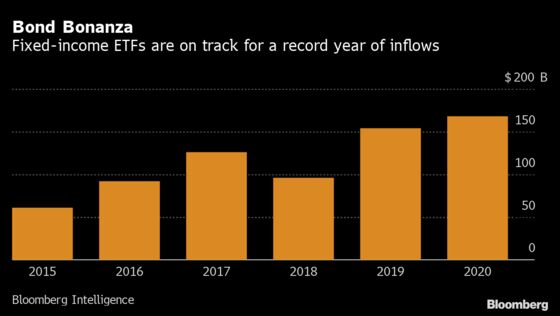

While the study used almost a decade’s worth of data through to the second quarter of 2019, the market for fixed-income ETFs has exploded in size since then.

Bond ETFs have pulled in about $170 billion in 2020, surpassing equity inflows and already beating last year’s record $154 billion haul.

©2020 Bloomberg L.P.