Credit Investors Are All Swagger as Doubt Plagues Equities

Credit Investors Are All Swagger as Doubt Plagues Stock Markets

(Bloomberg) -- In the great market rebound of 2019, not all rallies are created equal.

The best start to a year for U.S. stocks since 1987 is plagued by doubt, seen in seemingly relentless outflows, rising premiums for the safest shares and smart-money investors cowering on the sidelines.

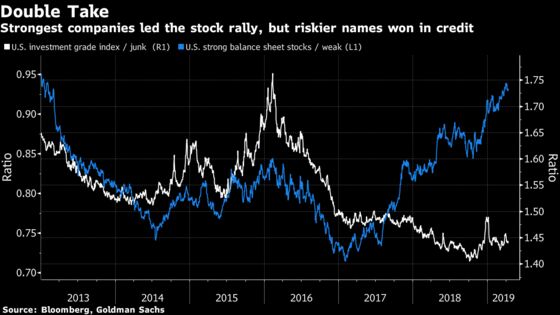

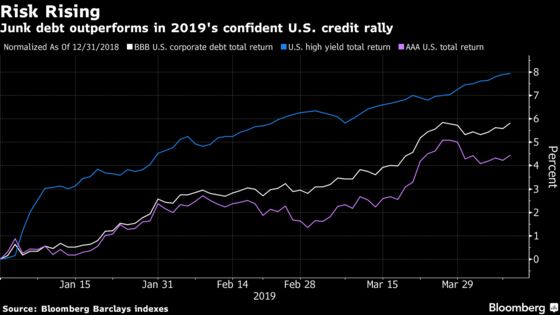

It’s a different story in credit where the strongest first-quarter in a decade has been greeted with a growing sense of conviction. Junk bonds are outperforming better-rated counterparts, while equities with the strongest balance sheets trade close to 2013 highs versus the weakest.

Add strong inflows into fixed income and the tumbling cost of default swaps, and the credit landscape is looking decidedly bullish.

All told, the self confidence of debt investors versus their insecure equity peers tells you everything you need to know about this vexed business cycle.

“We see slower growth and potential problems with leverage and balance sheets -- and therefore investors are going into low volatility and strong balance-sheet stocks,” said Willem Sels, a London-based chief market strategist at HSBC Private Bank.

There’s no shortage of ways to think about the diverging sentiment.

It’s a story of how equity investors are paying through the nose for strong companies in a world bereft of economic growth. It’s a tale of how a $10 trillion pile of global bonds with below-zero yields is forcing fund managers to accept thinner risk premiums.

And it tells you that the post-crisis hospitality for corporate leverage is easing -- helping debt potentially outperform shares along the way.

Whatever your world view, the fears for corporate profits that hang over the stock rally are effectively a sideshow for fixed income right now. Dovish central banks are reducing the risks of default and intensifying the hunger for yield.

Read more: Aramco Mega Deal Is Just a Tiny Part of the Bond Market Boom

Against this backdrop, the average premium on U.S junk bonds over investment grade is about a half a percentage point from the lowest level notched since 2007.

What’s more, fewer traders are paying up to short exchange-traded funds that track U.S. corporate bonds. The percentage of shares on loan to short sellers in the iShares iBoxx Investment Grade Corporate Bond ETF has this year fallen at a faster pace relative to same measure for the benchmark equity product.

While it makes sense for some shorts to be unwound in the rally, default swaps also point to robust confidence on the business cycle.

The Markit CDX North America Investment Grade Index, a gauge of contracts to insure corporate debt for five years, sits almost seven basis points below its five-year average.

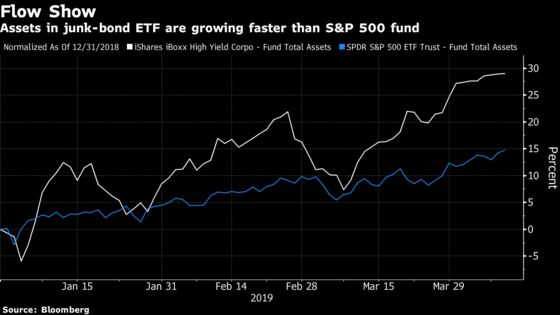

Yet in equities, caution is legion with hedge funds sitting out the $10 trillion global rally.

The iShares Edge MSCI Min Vol USA ETF, ticker USMV, has seen inflows almost every day this year, attracting more than $3.5 billion in 2019. That’s a sign of investors hedging their bets by pouring cash into low-volatility strategies that offer more protection during downturns.

Deleveraging Drive

Debt markets may even want to thank Federal Reserve Chair Jerome Powell’s hawkish pronouncement in October, which fueled the fourth-quarter meltdown and led to the central bank’s subsequent dovish capitulation.

The resulting paranoia about the longevity of the bull market continues to spur equity investors to bid up names with healthier balance sheets -- giving companies an incentive to bolster their creditworthiness.

“Are we going to see more rating downgrades or are we going to see more and more companies cutting their dividends or being forced to make disposals to cut their debt -- which benefits the bond holder at the expense of the equity holder?’’ asks Sels at HSBC.

It’s one reason why BNP Paribas SA strategists said this week that the post-crisis credit supercycle will run longer than previously anticipated, dubbing 2019 the “year of deleveraging” across America and Europe.

Still, while bonds are getting a helping hand from benign technicals like modest net supply, it’s not unabashed enthusiasm out there. Bonds rated CCC have struggled to best better-rated junk peers and valuations are looking rich across the risk spectrum.

HSBC Holdings Plc is now “mildly bearish” on both high-grade and high-yield U.S. credit given the stellar start to the year. What’s more, some investors are starting to make peace with the equity rally, with implied volatility for stocks evaporating this year alongside that of credit.

But for all that, while sentiment and positioning have scope to rise across both stocks and credit, it’s easier to make the bull case for fixed income in the lowflation climate.

“We are encouraged to fully embrace the bond market and want to be buyers of every backup in yields or widening in credit spreads,” Bob Michele, CIO and head of global fixed income at JPMorgan Asset Management, wrote earlier this month. “At some point, there should be a grudging acceptance of the new reality: It’s time to embrace your bond portfolio manager again.”

--With assistance from Eddie van der Walt, Ksenia Galouchko and Yakob Peterseil.

To contact the reporter on this story: Samuel Potter in London at spotter33@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2019 Bloomberg L.P.