Credit Funds Lure Big Investors Betting on a 2009-Style Rebound

Credit Funds Lure Big Investors Betting on a 2009-Style Rebound

(Bloomberg) -- Big-money investors facing steep losses are looking at credit funds to boost their returns -- just like after the last financial crisis.

The market turmoil created by the coronavirus pandemic led to declines at pension funds, endowments and foundations comparable with 2008’s meltdown. As they plot rebounds, they are looking to the likes of Howard Marks’s Oaktree Capital Group and Pacific Investment Management Co., as well as smaller hedge funds such as Diameter Capital Partners, who collectively are seeking to raise at least $38 billion.

Credit managers, who in recent years suffered as low rates hindered their strategies, are eyeing bargains created by the global slowdown and rushing to raise new funds to meet demand. The winners are likely to be those who use less leverage, according to investors, and familiar firms should also have an advantage, given the difficulty of conducting due diligence in the midst of a global lockdown.

Stay-at-home mandates and business closures enacted to combat Covid-19’s spread brought the world’s economy to a standstill, sent stocks plunging and froze credit markets. While unprecedented government support has stemmed the bleeding, few now expect a quick recovery, a situation that should help credit funds thrive.

“Corporate distressed debt is the most attractive risk-adjusted return opportunity given the likelihood of a surge in defaults and a need for capital to help good, but leveraged, companies,” said Adam Blitz, chief investment officer at the $3 billion Evanston Capital Management.

Blitz said he will be adding to these hedge funds over the next few quarters. He plans to stay away from leveraged strategies such as structured credit, collateralized loan obligations and business development companies, at least for now.

It’s a view echoed by other investors. The $54 billion Los Angeles County Employees Retirement Association plans on increasing its credit exposure, including allocating to private debt funds. And almost two-thirds of the 200-plus investors surveyed at the end of March by Morgan Stanley said they plan to give money to credit and distressed hedge fund managers.

While credit funds returned an average of 30% in 2009, outpacing other hedge funds, they held less allure to investors in subsequent years. Distressed funds in particular failed to produce hefty returns as bankruptcies were almost non-existent and even troubled companies could borrow at low rates.

Coronavirus changed all that. In just two weeks last month, the tumble in prices created nearly $1 trillion in distressed securities in the U.S.

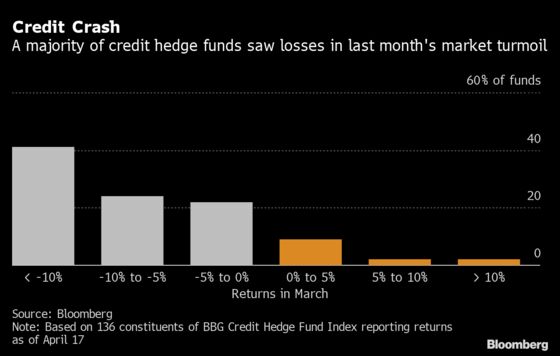

The interest in credit funds has jumped even though many funds have done poorly this year and some economists say that the market recovery might not look anything like 2009’s rebound. About four out of 10 lost more than 10% in the first quarter, and only roughly one in 10 made money, according to data compiled by Bloomberg.

That’s the widest range of performance on record, even more than in 2008, said Jon Caplis, head of PivotalPath, which provides hedge fund data and research to institutional investors. March returns swung anywhere from down 88% to up 29%, he said.

Flows have been heading into credit funds seemingly regardless of recent performance.

Diameter, a three-year-old firm with $4 billion in assets that posted a 7% gain this year, raised $500 million in its hedge fund. It’s seeking another $500 million in a new drawdown fund. Sculptor Capital Management Inc., formerly known as Och-Ziff, brought in $1 billion, even though its Credit Opportunities fund fell about 20% in the first quarter.

The Los Angeles County retirement plan has $530 million of undrawn capital commitments to private credit managers, Jon Grabel, investment head, said in a board memo last month. He expects much of that to be invested in the coming weeks and months.

The pension fund is completing due diligence on at least two more private credit managers, Grabel said, and he expects to make opportunistic investments in high-yield bonds, loans and emerging-market debt.

One investor, who manages money for wealthy families, says his firm will venture into residential mortgage-backed securities, in part because non-agency RMBS aren’t affected by the Federal Reserve’s buying program. The central bank’s recent actions have been faster and bigger than in previous crises.

The investor, who asked not to be identified, said he’d be willing to allocate to managers that suffered during last month’s market sell-off because it may be harder for those who did well to switch their portfolios to take advantage of opportunities.

While there’s high interest in credit funds, managers may have to wait for investors to commit capital, said Caplis of PivotalPath.

“Everyone believes that distressed will have tremendous opportunities in the next six to 18 months,” he said, noting that most defaults won’t happen until the second half of the year. “The consensus among investors is that they don’t need to rush.”

©2020 Bloomberg L.P.