CQS Hedge Fund Says Curve Inverting on Technicals Won't Last

CQS Hedge Fund Says Curve Inverting on Technicals Won't Last

(Bloomberg) -- As sovereign bonds around the world continue their relentless climb and a closely watched segment of the U.S. yield curve inverts -- seen as a harbinger of recession -- the level of anxiety about the global economy can’t be understated. For hedge fund CQS, that caution has gone a bit too far.

“We are not quite that gloomy, in fact, we are rather more sanguine about prospects for the global economy,” Xavier Rolet, chief executive officer at London-based CQS, which manages about $18 billion, told Bloomberg TV. “There are some technical considerations at the moment that are impacting the shape of the curve. These are temporary conditions.”

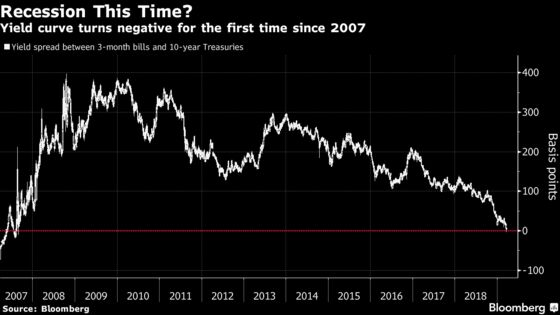

Central banks in the U.S., Japan and Europe this month all flagged growth concerns and sovereign bonds are hitting multi-year lows from Australia to Germany. The spread between yields on three-month T-bills and 10-year Treasuries evaporated for the first time since 2007 on Friday. Typically when the curve flips, with yields on short-term debt exceeding those on longer bonds, economic growth continues to slow and interest rates are cut.

Rolet’s view chimes with Morgan Stanley Investment Management, which recently said this part of the curve “is distorted” by global forces fueling demand in the long end, while increased bill supply is elevating short-end rates. There are also fundamental factors that suggest the curve inversion may not last: Financial conditions have eased since the recent peak in December, offering some degree of support to the American economy.

“We are a little bit optimistic,” Rolet said on the sidelines of a Milken Institute conference in Tokyo on Monday. “We consider that these conditions at the moment are rather technical. They are linked in part to Treasury issuance, particularly on the short-end of the curve -- the Fed’s balance sheet is essentially of a longer duration.”

Part of that optimism comes from Rolet’s view that corporate-default rates remain “at the low end” of the historical range. “The credit cycle has a few years to go,” he said.

--With assistance from Kathleen Hays, Andy Clarke and Adrian Wong.

To contact the reporters on this story: Adam Haigh in Sydney at ahaigh1@bloomberg.net;Haidi Lun in Sydney at hlun1@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Andreea Papuc, Joanna Ossinger

©2019 Bloomberg L.P.