The Potential Winners From a Crackdown on Huawei

The Potential Winners From a Crackdown on Huawei

(Bloomberg) --

The market is being driven by global growth jitters and the China-U.S. trade dispute. Amid the tensions and tariffs, there’s also a key battle going on: the fight for leadership in the next generation of wireless systems known as 5G.

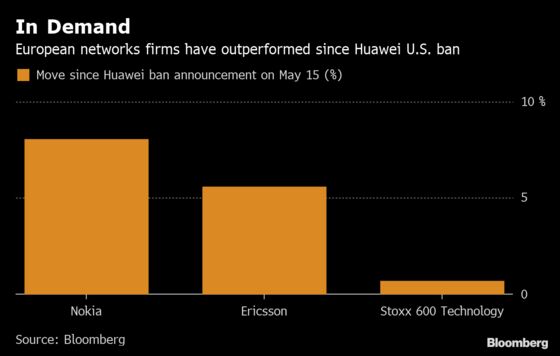

With China’s Huawei in the eye of the storm, European competitors could emerge as winners in the race for spectrum. Both Nokia and Ericsson have outperformed the Stoxx 600 Tech index since the announcement of the U.S. ban on Huawei last week.

“We expect many operators to initiate discussions with both Nokia and Ericsson in the current environment, and explore the possibility of moving equipment share to the two Scandinavian providers,” Liberum analysts write in a note to clients.

The Radio Access Networks market is very concentrated, with Huawei holding 31% of global market share in 2018, Ericsson 29% and Nokia 23%, according to research firm Dell’Oro. This puts the European firms in an ideal position to benefit from Huawei’s troubles, UBS analysts said in a recent note.

Nokia could even be the biggest winner, as telecoms operators look to balance their supply base, and the company has scope to grow in the IP/Optical market, UBS wrote.

No wonder Nordea upgraded Nokia to buy this week, saying that the Finnish company may enjoy a period of growth lasting several years. Nokia’s competitive situation has “improved considerably” due to the security concerns faced by the Chinese company, Nordea said, adding that Nokia has a 15% valuation discount to Ericsson, and most risks are priced in after its recent underperformance.

Looking at the table below, Nokia is trading at lower multiples and offers a higher upside than Ericsson, according to analysts tracked by Bloomberg.

| Name | Est. P/E | Average Analyst PT | Up/Downside Potential |

| Nokia | 14.4 | EU5.5 | 20% |

| Ericsson | 23.3 | SEK90.8 | -3.4% |

| Cisco Systems | 16.9 | $56.9 | 1.7% |

| Stoxx 600 Tech | 21.8 | - | - |

| SOX Index | 15.3 | - | - |

| Nasdaq 100 | 20.6 | - | - |

| Source: Bloomberg | |||

Things may not be quite so straightforward of course. Switching providers could be costly and trigger a delay in 5G implementation. Nokia generates about 11% sales in China and Ericsson 7%, a market where they could potentially lose some ground, UBS said.

In the meantime, Euro Stoxx 50 futures are trading down 0.2% ahead of the open.

- Watch the pound and U.K. stocks sensitive to newsflow around Brexit after U.K. Prime Minister Theresa May’s new attempt to get her deal through Parliament was received poorly. The pound has already given up most of the initial gains made following the announcement. Watch homebuilders, lenders, retailers among other sectors.

- Watch trade-sensitive sectors after the U.S. says Europeans are starting to come around to the threat posed by China’s Huawei Technologies. The U.S. administration is considering a ban on five additional Chinese technology firms, while American companies in China are now considering relocating or trimming investment.

- Watch for reaction to Fed speeches before the publication to Fed minutes. The market is signaling that the economy needs lower interest rates, but the central bank is afraid of fostering bubbles. Eric Rosengren was the latest to say that the downside risks the U.S. economy faces are enough to convince him of the patience required on policy and James Bullard thinks the hike back in December may have “slightly overdone it.”

COMMENT:

- “From here, the faster Euro-area growth acceleration expected by our economists in H2 is unlikely to be strong enough for European equities to outperform meaningfully,” Goldman Sachs strategists write in a note. “(i) political uncertainty will likely remain elevated, the US-Sino trade tensions will likely spill over to Europe, (ii) growth remains structurally lower in Europe; (iii) part of the growth improvement has already been priced.”

COMPANY NEWS AND M&A:

- Oriflame Gets $1.3 Billion Takeover Offer From Jochnick Family

- BMW CEO Future in Doubt as Tensions Erupt Over Epic Shift (1)

- Marks & Spencer Announces Rights Issue of GBP601.3m for Ocado JV

- Generali Is Said in Talks to Buy MetLife Central European Assets

- UBS Is Poised to Settle Tax Case With Italy for $110 Million

- SocGen Investment-Banking Unit Rev. Will Rise in 2020, CEO Says

- Sandvik CEO Says Trough Margin Target Would Be 18% Excluding SMT

- Belgian Tax Inspectors Take AB Inbev to Court: L’Echo

- Novartis Phase II QVM149 Asthma Treatment Meets Primary Endpoint

- Top Miner BHP Sees Coal’s Era Ending in Shift to the Battery Age

- Barrick Offers to Buy Remaining Acacia Shares in Stock Swap

- Norsk Hydro’s Albras Starts Process of Resuming Full Production

- EU Commission and Police Raid Casino, Intermarche Offices: Figaro

- Uniper Disputes Claims Made by Fortum Over Company’s Performance

- Vienna Insurance 1Q Pretax Profit 3.6% Below Est.

NOTES FROM THE SELL SIDE:

- Sandvik announced new financial targets that are broadly in line with Citi’s expectations, broker says in a note; rates stock neutral, PT SEK181. Sees Sandvik treading carefully against rich target multiples, meaning any major growth step-up is likely far ahead.

- Bankhaus Lampe cut Dialog Semi to hold from buy, with Apple-related benefits seen as fully reflected in the shares and several challenges needing to be resolved before greater multiples can be justified.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 383.3 (50-DMA); 385.7 (76.4% Fibo)

- Support at 374.5 (61.8% Fibo); 369 (200-DMA)

- RSI: 45.4

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,410 (50-DMA); 3,516 (76.4% Fibo)

- Support at 3,309 (50% Fibo); 3,272 (200-DMA)

- RSI: 46

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- DKSH upgraded to neutral at MainFirst; Price Target 62 Francs

- DSV upgraded to overweight at Morgan Stanley; PT 750 Kroner

- Norsk Hydro upgraded to buy at Pareto Securities; PT 40 Kroner

DOWNGRADES:

- Dialog Semi downgraded to hold at Bankhaus Lampe

- GEA Group downgraded to sell at AlphaValue

- Ryanair downgraded to reduce at HSBC; PT 9.40 Euros

- Sparebank 1 Oestlandet cut to hold at Kepler Cheuvreux

INITIATIONS:

- Hastings rated new sell at Panmure Gordon; PT 1.45 Pounds

- JPMorgan Japanese Investment Trust PLC/Fund new buy at Investec

- Sabre Insurance rated new sell at Panmure Gordon; PT 2.20 Pounds

MARKETS:

- MSCI Asia Pacific down 0.3%, Nikkei 225 little changed

- S&P 500 up 0.8%, Dow up 0.8%, Nasdaq up 1.1%

- Euro down 0.09% at $1.1151

- Dollar Index up 0.01% at 98.07

- Yen up 0.06% at 110.43

- Brent down 0.6% at $71.7/bbl, WTI down 0.9% to $62.6/bbl

- LME 3m Copper down 0.2% at $5983/MT

- Gold spot down 0.1% at $1273.4/oz

- US 10Yr yield down 1bps at 2.42%

MAIN MACRO DATA (all times CET):

- 10:30am: (UK) April PPI Output NSA YoY, est. 2.3%, prior 2.4%

- 10:30am: (UK) April CPI MoM, est. 0.7%, prior 0.2%

- 10:30am: (UK) April CPI YoY, est. 2.2%, prior 1.9%

- 10:30am: (UK) April CPI Core YoY, est. 1.9%, prior 1.8%

- 10:30am: (UK) April Retail Price Index, est. 287.6, prior 285.1

- 10:30am: (UK) April RPI MoM, est. 0.9%, prior 0.0%

- 10:30am: (UK) April RPI YoY, est. 2.8%, prior 2.4%

- 10:30am: (UK) April RPI Ex Mort Int.Payments (YoY), est. 2.8%, prior 2.4%

- 10:30am: (UK) April PPI Input NSA MoM, est. 1.3%, prior -0.2%

- 10:30am: (UK) April PPI Input NSA YoY, est. 4.5%, prior 3.7%

- 10:30am: (UK) April PPI Output NSA MoM, est. 0.3%, prior 0.3%

- 10:30am: (UK) April CPIH YoY, est. 2.1%, prior 1.8%

- 10:30am: (UK) April PPI Output Core NSA MoM, est. 0.2%, prior 0.0%

- 10:30am: (UK) April PPI Output Core NSA YoY, est. 2.2%, prior 2.2%

- 10:30am: (UK) March House Price Index YoY, est. 1.0%, prior 0.6%

- 10:30am: (UK) April Public Finances (PSNCR), prior 8.9b

- 10:30am: (UK) April Central Government NCR, prior 22.5b

- 10:30am: (UK) April Public Sector Net Borrowing, est. 5.1b, prior 800m

- 10:30am: (UK) April PSNB ex Banking Groups, est. 5.9b, prior 1.7b

--With assistance from Kit Rees.

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Hanna Hoikkala in Stockholm at hhoikkala@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.