Corporate Bonds Aren’t Worried About a Trade War

Corporate Bonds Aren’t Worried About a Trade War

(Bloomberg Opinion) -- Even before markets opened this week, President Donald Trump set the tone with a pair of tweets that threatened additional tariffs on China and lamented that a trade deal was coming along “too slowly.” Instinctively, investors’ eyes were glued to the S&P 500 Index, watching to see whether it would tumble from its recent record levels.

The benchmark hung tough on Monday, before plunging as much as 2.4 percent on Tuesday. That, in turn, sent the Chicago Board Options Exchange Volatility Index, sometimes referred to as the market’s “fear index,” to the highest since January. “‘Fasten your seatbelt and don't hold your breath’: Wall Street scrambles to figure out what's next for stocks after Trump sends shockwaves through markets” declared a Business Insider headline, effectively capturing the type of hyperbole making the rounds.

Yet all the while, it has been surprisingly smooth sailing for borrowers in the U.S. corporate bond market.

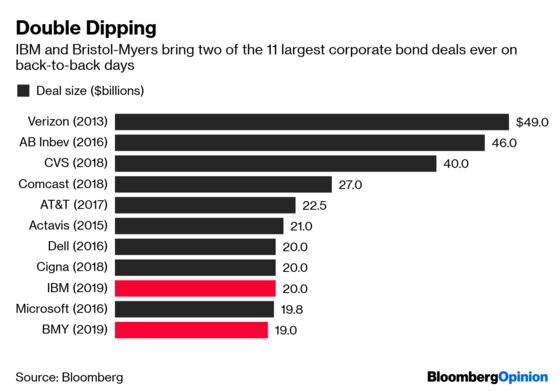

Even as the stock-market sell-off escalated, Bristol-Myers Squibb Co. on Tuesday easily issued $19 billion of bonds, the largest deal of 2019 at the time, and cut yields by as much as 15 basis points on some maturities relative to initial price talk. Then on Wednesday, International Business Machines Corp. went one better by moving forward with a $20 billion offering to help fund its acquisition of Red Hat Inc. Even the high-yield market saw $5.4 billion of debt come through on Tuesday, the most for a single day in three months. It seems as if more is on the way.

These figures are striking when compared with how those very same markets reacted to December’s rout in risk assets. As a quick refresher, not a single speculative-grade company borrowed in that month, making it the first in a decade with no sales. Investment-grade issuance wasn't much better, with only $8 billion pricing in what was the slowest December since 1995.

Of course, there’s still time for the trade war to escalate in the days ahead. But the lack of spillover from the three-day slide in equities to other markets suggests that traders expect whatever comes from negotiations will have a minimal impact on where corporate bonds are trading right now, up 6% on the year. Investors aren’t rushing indiscriminately to havens, either – the U.S. Treasury’s auction of $27 billion in 10-year notes on Wednesday drew the weakest demand since March 2009.

Some of this might have to do with seasonality: In credit markets, issuance tends to slow down during the U.S. summer months. “If you’ve got to get a deal done and there’s even a little uncertainty about the markets, that’s an additional push,” Lale Topcuoglu, senior fund manager and head of credit at J O Hambro Capital Management, told Bloomberg News’s Molly Smith and Natalya Doris. “You really have May to crank as much as you can.” When the dust settles on the month, issuance may total $120 billion, according to Bloomberg News’s informal poll of primary dealers. This week’s volume has already topped $40 billion, the high-end of projections.

More than anything, the resilience of corporate bonds shows how the overall mood across financial markets has been far too pessimistic. The latest round of company earnings could have been a lot worse. The American labor market is as strong as ever. The Federal Reserve might not be cutting interest rates, but policy makers aren’t in any rush to raise them, either. All the while, stocks remain near all-time highs. If there’s a bit of a pullback from those peaks, that’s only natural.

In the meantime, companies like Bristol-Myers and IBM need to get on with their long-planned acquisitions. IBM, in one of the 10 largest corporate-bond sales on record, lowered yields on its offering relative to initial price talk, with the sharpest tightening in the shorter-dated maturities. That seems fair: The computer-services giant has slow-but-steady revenue growth for now, but is aiming to kick it up a notch in the future with its Red Hat purchase. As my Bloomberg Opinion colleague Shira Ovide wrote back in October, “IBM and Red Hat certainly make a more compelling cloud-computing alternative as a combined force than they ever could on their own.”

In perhaps the clearest sign that bond investors aren’t fretting a broad market reversal, consider this: IBM’s sharp increase in leverage could spur the major credit-rating companies to lower the company’s grade to triple-B, according to Bloomberg Intelligence analysts Robert Schiffman and Mike Campellone. The lowest investment-grade tier, of course, was considered highly risky throughout most of last year. Yet the $20 billion sale went off without a hitch.

Maybe both the U.S. and China will raise tariffs as soon as Friday. Maybe the two sides will reach a deal. Either way, corporate bonds are sending a clear signal to panicked investors that the trade-war hysteria is overblown.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.