CLOs Stumble After Shift From Fed, Even as Japanese Demand Remains Strong

Issuers not strongly supported by overseas investors have to either sweeten deals for a U.S. audience or offer juicier yields.

(Bloomberg) -- U.S. investors of collateralized loan obligations may be shifting to fixed-rate assets after the Fed’s recent flip on interest rate hikes while those deals benefiting from Japanese bank demand outperform.

The pullback from American buyers is causing tiering in the pricing of CLOs, meaning similarly rated bonds from separate managers with strong investor support are pricing differently, market experts say. Even some established CLO shops have endured weaker pricing in recent weeks because they rely on U.S. buyers to purchase the highest rated slices of their deals.

“Issuance has picked up, but issuers are facing limited U.S. demand for AAAs, leading to substantial AAA tiering of 15 to 25 basis points,” Wells Fargo & Co. analysts Dave Preston and Mackenzie Miller wrote in a recent client note. “We see established managers with robust issuance platforms who are nonetheless pricing AAAs in the mid-/high-140 basis-point area.”

Managers that rely on Japanese banks to buy the bulk of their AAA rated bonds, meanwhile, have been able to price as much as 10 basis points tighter. While those with a strong base of AAA Japanese investors have historically always priced with tighter spreads, the difference has become more exaggerated recently.

“There does appear to be greater differentiation between deemed ‘top tier’ versus ‘second tier’ managers with recent transactions,” said Steven Oh, head of credit and fixed-income investments at money manager PineBridge Investments, in an instant message.

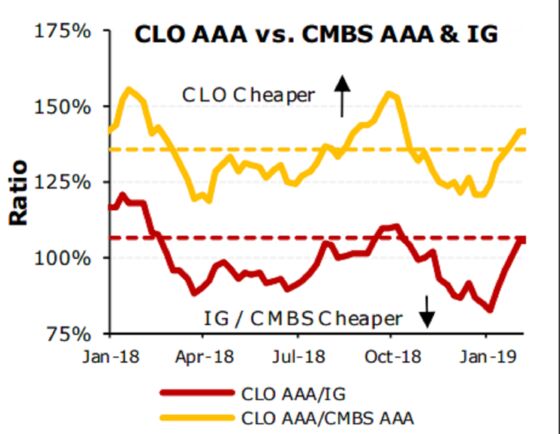

Fixed-rate assets, such as commercial mortgage backed securities and investment-grade corporate bonds got much cheaper in December, making them even more attractive now as investors pivot away from floating-rate instruments.

“IG and CMBS widened much more than CLOs in late 2018," the Wells Fargo analysts wrote in a note this week. "As a result CLO AAAs looked rich from mid-November to late January."

“Spreads across various other investment-grade bond areas have widened versus year-ago levels and while CLO debt remains very attractive, some investors have full exposure and are therefore not adding incremental exposure,” Oh said.

Wave of Supply Expected

Some issuers not strongly supported by overseas investors have had to either sweeten deals for a U.S. audience with shorter reinvestment periods or offer juicier yields. Regardless of the reason, CLO managers have encountered significantly wider spreads recently versus their prior 2018 transactions in light of this past December’s credit-market selloff.

Investcorp Credit Management, an established name in the market, recently priced the AAA slice of a deal at 147 basis points over Libor compared to +110 on its prior new-issue trade last June. Just today, Carlyle CLO Management priced its first 2019 CLO AAA at 132 basis points over Libor versus 117 basis points for a deal raised on Nov. 30, just prior to the leveraged-market swoon.

An expected wave of supply in March is also influencing investors’ decision to hold off for the time being. "I think it’s simply a function of larger potential near-term supply versus demand that has resulted in higher execution uncertainty," PineBridge’s Oh said. This requires "increased yields to compensate for the lower-tier managers or portfolios that may be considered to be of higher-risk credits," he added.

The shift away from hiking interest rates was confirmed in the Federal Open Market Committee’s policy meeting minutes released on Wednesday. Leveraged loans and CLOs rallied when the Fed was seen to be in hiking mode because they are less sensitive to rising Treasury yields as their coupons adjust to changes in rates.

To contact the reporter on this story: Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Rizal Tupaz

©2019 Bloomberg L.P.