CLO Managers Proceed Cautiously Into 2019 After Record Year

CLO Managers Proceed With Caution Into 2019 After Record Year

(Bloomberg) -- Europe’s CLO managers are approaching the start of 2019 in a much more cautious mood than this time last year given there are many unknowns in the market that could weigh on issuance.

Among them are geopolitical risks such as Brexit, as well as more localized concerns including the end of the European Central Bank’s quantitative easing, a stretched arbitrage, portfolio health and the unfinished business that is the Securitisation Regulation.

“2019 will continue to bring uncertainties around Brexit, Italy, global trade wars and we’ll be getting closer to the end of the cycle, so higher volatility is likely to persist,” said Aza Teeuwen, a portfolio manager at TwentyFour Asset Management LLP in London.

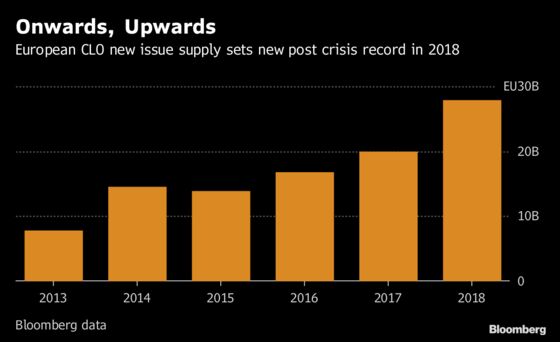

While the market notched up its third consecutive annual supply record for 2018 at 27.9 billion euros ($31.8 billion), the backdrop is less conducive than it has been over the past two years for primary activity. The pipeline is full with a lengthy list of new entrants, but how quickly new issuance restarts could depend on conditions during the first quarter.

Primary Prognosis

Supply flat-lined in December as volatility and regulation brought issuance to a halt earlier in the year than usual. Managers, as well as arrangers sitting on fuller warehouses, will no doubt welcome a swift return to primary activity early next year to start shifting the bulging pipeline. There is currently a mix of more than 30 delayed transactions and new facilities after managers rushed to open new warehouses in the final quarter of 2018.

But progress on the issuance front could be slow and hinges on a return to more stable macro conditions. The relationship between CLO liability and loan spreads, known as the arbitrage, will also be key to pricing deals.

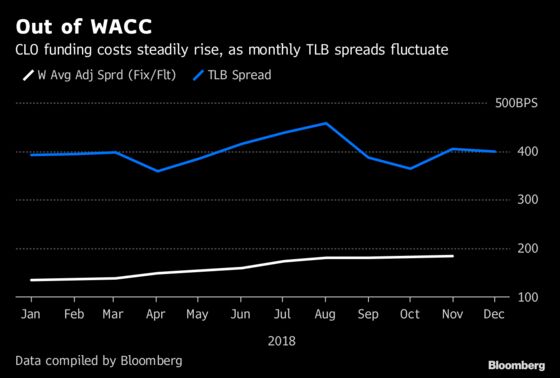

The ‘arb’ deteriorated through 2018 as spreads -- first in the top rated CLO debt tranches, and then in the bottom as the volatility hit -- pushed funding costs to 185 basis points on average in November from 134 basis points in January, according to coupon data compiled by Bloomberg. The outlook is more promising on the loan side after lenders sought higher pricing and better structures in the final three months of the year.

Any further erosion in the arb could threaten the CLO take out altogether, especially for older warehouses, or require managers to offer up fees to boost equity returns. Conversely, those able to take advantage of the secondary market weakness, by filling new warehouses with discounted assets, could command equity investors’ attention.

Wider liability spreads could also make it harder for the crop of new managers now lining up deals. As many as 15 would-be joiners may materialize in addition to this year’s five new entrants, who have expanded the issuer base to 46.

Europe’s Expanding CLO Issuer Base Boosts Post Summer Pipeline

But if the equity bid is weaker, investor-friendly documentation and higher priced bonds could maintain demand for the debt tranches of a CLO. Appetite from Japanese and Korean accounts remains, even if other relative value players have proved fickle at the mezzanine level and other investors could play CLO AAAs off the wider spreads on other ABS debt rated triple A.

Regulatory Limbo

Issuers will also have to carefully navigate the as yet unfinished Securitisation Regulation for Europe and this could act as a drag on supply, depending on when and how the unresolved rules are finalized.

CLO Managers in Limbo Ahead of Onerous European Reporting Rules

Managers say they will push ahead with new deals guided by their legal counsel, but investors, who will also need to comply with the new rules from January, may be less relaxed about funding deals until the rules are finalized.

Arrangers will also likely move cautiously by protecting themselves against increased warehouse risk on their balance sheets. Measures include caps on commitment levels in existing warehouses and the enforcement of a “one in one out” strategy, at least until the backlog is cleared.

Andante, Andante

From an investor perspective there are more reasons to proceed carefully than in previous years, given the maturing credit cycle and increasing idiosyncratic risk in CLO asset pools. Portfolio health is of particular concern to equity investors, some of whom have stepped back from the market this year.

Complying with CLO collateral tests is an ongoing struggle for managers, who will need to avoid single-name problem credits and riskier assets as they try to stay compliant with these tests.

“It is not the time for CLO managers to be adding credit risk right now,” said TwentyFour’s Teeuwen. “Credit blow ups are increasing and every manager will get a few names wrong, but for us it is how they manage that situation.”

A source of comfort over the next 12 months is an expectation of low loan default rates and the stable performance of collateral and ratings. The default rate in underlying CLO collateral also remains very limited at just 0.1 percent across 21 transactions, Deutsche Bank analysts said in their European Securitisation Outlook 2019.

Final Word

While the mood is cautious moving into 2019, conditions can switch quickly as uncertainty is eliminated. And any early year disruption to the pipeline, while frustrating, could also sow the seeds for a more productive second half if the subsequent reduced demand for loans from CLOs helps correct the arbitrage. Certainly, research analysts have hopes for another strong year with some forecasting at least 25 billion euros of new supply.

“More than in any other year the political background and general instability makes it hard to know what is in store next year,” said Colin Atkins, co-head of CLOs, head of European structured credit at Carlyle Group LP. “Equally, the experience of early 2016 shows just how quickly the market can snap back.”

--With assistance from Ruth McGavin.

To contact the reporter on this story: Sarah Husband in London at shusband@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, Charles Daly

©2018 Bloomberg L.P.