Quant Legend Cliff Asness Is Back to Defending Value Again

Cliff Asness Is Back Doing What He Does Best: Defending Value

(Bloomberg) -- After a few glorious months, the value faithful are playing defense again. Fortunately, they’ve had quite a bit of practice -- and none more so than Cliff Asness, the godfather of quant investing and co-founder of AQR Capital Management.

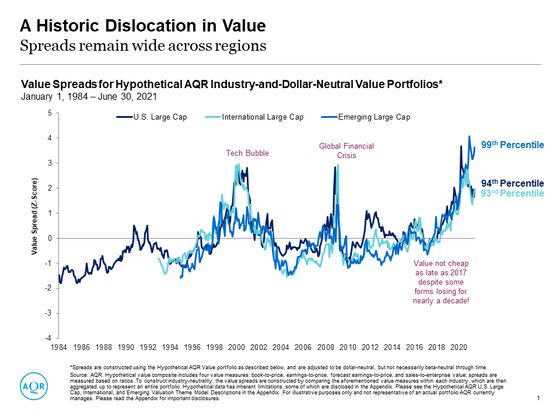

As the strategy that favors cheap-looking stocks struggles to find fresh momentum, he’s delivering a familiar refrain this week: The wide valuation spreads between the priciest and cheapest equities still point to a bright future for the value trade.

“Current value spreads -- call them at record levels,” Asness, 54, said during a webinar on Wednesday. It’s a differential that’s been inflated by ever-higher prices for growth stocks. “When it walks like a bubble and quacks like a bubble, we’ll eventually say it’s a bubble,” he said.

Sure, he’s said that before. But his past counsel seems a bit more prescient following the historic turnaround in value this year.

As hopes for a post-pandemic recovery buoyed a broad swath of shares, AQR’s funds enjoyed one the strongest starts to a year ever. Both its Long Short Equity Fund and Style Premia Alternative Fund are up roughly 20% so far.

Much of that is down to a recovery in value, which aims to buy the market’s cheap underdogs and dump its overpriced darlings. With a few record-shattering months, a long-short version surged 11% this year through mid-May, though it has since trimmed some of that gain.

That has left Wall Street names from JPMorgan Chase & Co. to Ned Davis Research debating whether the value rebound has further to run. To Asness, the story is still the same: Even after value’s rebound, spreads are wide. Meanwhile, analyst forecasts for cheap stocks’ earnings growth aren’t unusually low relative to the opposite category of growth shares.

“There’s no indication that the market is saying ‘sure, valuations may be radically different today, but it’s justified by the difference in earnings growth we expect,’” Asness said. “We’re excited about performance, but nothing goes in a straight line.”

That’s definitely been the experience for factor quants like Asness, who slice and dice stocks based on quantifiable characteristics such as how profitable they are or the momentum of their price moves. For most of the post-crisis era, equity gains were concentrated in Big Tech stocks, making broad-based quant strategies less effective and benchmarks harder to beat.

There remains much contention over why this happened. One theory holds that it’s simply down to the Faang cohort’s extraordinary success in the real world, where they dominate entire industries. Another argues that loose monetary conditions favor growth stocks -- whose long-term cash flows can be discounted at lower rates -- at the expense of value shares that tend to be more tethered to the economic cycle.

That link would seem to be validated by the fact that when bond yields started rising faster this year amid fiscal support and economic reopening, value stocks also surged. When yields started dipping in recent weeks, the strategy pulled back, falling nearly 4% from its May peak.

Even so, AQR’s research shows the long-term correlation between bond moves and value performance remains low. The past decade’s relationship is stronger, but still modest.

“To actually be negative on value moving forward because of interest rates, particularly when value spreads are at such extremes, you have to believe the correlation environment of the last 10 years will persist forever and rates will fall dramatically from this low level,” Asness said. “This is just not a very big worry for me.”

©2021 Bloomberg L.P.