Citigroup Shows That Banks Can’t Depend on Traders

Citigroup Shows That Banks Can’t Depend on Traders

(Bloomberg Opinion) -- It’s a tough time to be a trader on Wall Street. (Cue playing of the world’s smallest violin.)

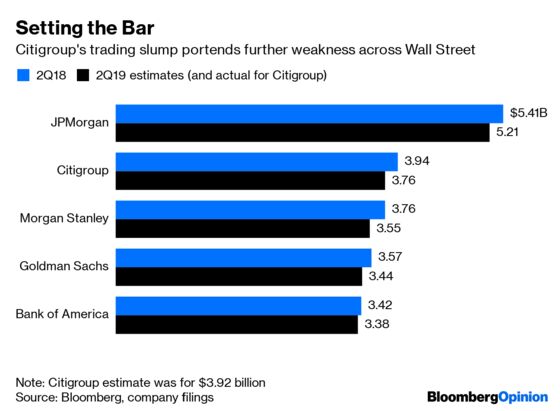

That much was clear after Citigroup Inc. reported its second-quarter earnings on Monday, kicking off a week that will reveal the financial health of the biggest U.S. banks. Trading revenue fell about 5% after excluding the one-time windfall from the bank’s stake in Tradeweb Markets, which went public in April and bought out Citigroup’s equity holdings. That drop was bigger than expected. The bank’s equity markets revenue was particularly disappointing at $790 million, compared with estimates of $824 million. Chief Financial Officer Mark Mason also cited a challenging trading environment in fixed income, currencies and commodities.

It’s true that Chief Executive Officer Michael Corbat joined other bank leaders in forecasting such a decline as far back as May. He reiterated on Monday that his bank reflects trends in the broader industry. But Citigroup holds the honor of going first this earnings cycle, and the results suggest that investors shouldn’t expect traders to deliver above and beyond expectations, which have already been set at a low bar.

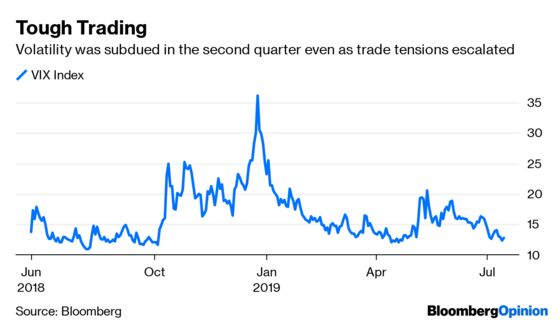

The Chicago Board Options Exchange Volatility Index, known as the VIX, pretty much summarizes why traders have fallen upon tough times. It closed above 20 only once during the second quarter and averaged about 15. For context, it spiked as high as 36 in late December. The second quarter was comparatively tranquil, which is just about the worst type of market for Citigroup traders to turn profits by lining up buyers and sellers. Mason in part blamed the U.S.-China trade war’s influence on investor sentiment and said the bank experienced declining volume and leverage in cash equities.

Even the bank’s fixed-income markets revenue was disappointing. While the VIX was contained in the second quarter, the same can’t be said for the Merrill Option Volatility Estimate, which is the U.S. Treasury market’s equivalent measure of volatility. It jumped in mid-June to the highest since December 2016 as bond traders rapidly priced in aggressive Federal Reserve easing. Those sorts of price swings might be over now that Chair Jerome Powell left no doubt that he’s on board with lowering interest rates to get ahead of any sort of global growth slowdown.

On the bright side, as Bloomberg News’s Jenny Surane noted, Citigroup cut costs deeper than analysts expected and its consumer division posted its strongest second quarter since 2013. Expenses fell 2% to $10.5 billion, which was almost $100 million lower than the average estimate from analysts, while revenue from consumer banking climbed 3% to $8.51 billion, topping projections. The issue with both of those elements, of course, is that the health of the U.S. consumer has already been well established, while investors are always a bit uneasy about the sustainability of reducing expenses to generate profits.

Citigroup shares were little changed Monday, which seems about right, given the stream of takeaways in analysts’ notes. The earnings were described as “decent,” “essentially in line” and creating “somewhat mixed feelings.” One of the most-anticipated figures from banks this week is the net interest margin, which measures the spread between revenue from customers’ loan payments and what it pays depositors. At Citigroup, it dipped to 2.67% from 2.72% in the first quarter and 2.7% a year earlier. Corbat said to expect the figure to remain around that level.

That’s not catastrophic by any means, but it further plays into the ho-hum commentary that seems likely to define U.S. banks in this earnings cycle.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.