Christmas Comes Early for Markets as Key Risks Get Taken Out

Suddenly, all the worries about a global recession are fading.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- It started last Friday, with a blowout U.S. jobs report that beat all expectations. Then in quick succession late Thursday investors got news that the guns will be holstered in the U.S.-China trade war, and that Britain is lifting itself out of the quagmire of a hung parliament.

Suddenly, all the worries about a global recession, yet another wave of tariff hikes between the world’s two largest economies and a messy U.K. breakup with the European Union are fading from view. It may be Friday the 13th, but those who made an early start on JPMorgan Chase & Co.’s call for risk-on trades in 2020 can count themselves lucky.

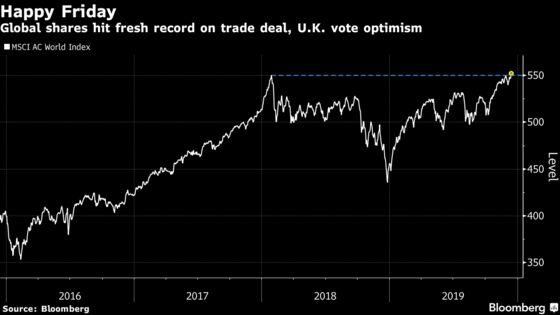

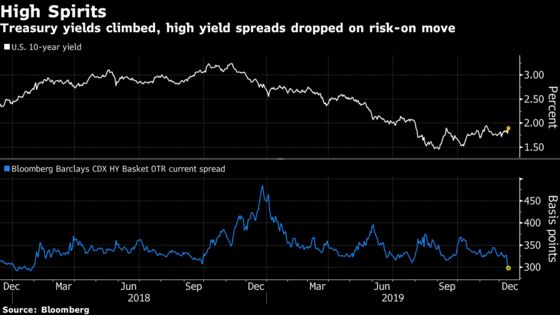

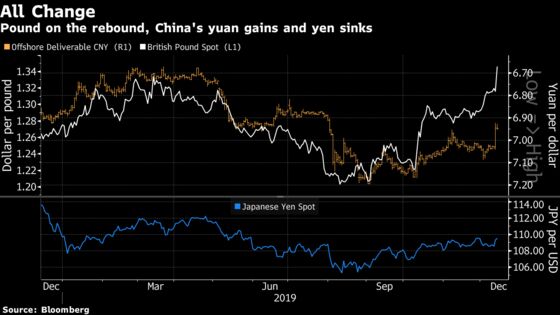

The S&P 500 Index and Nasdaq Composite logged record closes Thursday, helping push MSCI’s all-country world gauge to its first all-time high since the eve of the global rout in January 2018, back when a stocks “melt-up” was the narrative of the day. In currencies, the yen fell and the yuan soared. Bond yields climbed, with 10-year Treasuries around 1.9% and their Japanese counterparts in recent days straddling 0% for the first time since March.

The moves came on news that President Donald Trump signed off on a phase-one deal with China that averts the Dec. 15 introduction of another wave of U.S. tariffs. The S&P 500 swung between gains and losses in Friday trading, as neither side delivered sufficient details to assuage investors trade issues have been fully resolved.

In the U.K., Prime Minister Boris Johnson cruised to a big majority, an election result that should guarantee passage of his Brexit deal with the EU.

“The good news just seems to keep coming for markets,” said Kerry Craig, a Melbourne-based global market strategist at JPMorgan Asset Management. “Investors will be delighted to check their stockings and realize they won’t be receiving the lump of coal” they got last year, when global equities tumbled in the fourth quarter.

In a stark contrast to the liquidity crunch of late 2018, the Federal Reserve has been a major ally for those bullish on risk this year-end. The U.S. central bank started injecting liquidity in October at a pace of $60 billion of T-bill purchases a month, and Chairman Jerome Powell said Wednesday if needed the initiative could adjust to buying coupon-paying securities as well.

Bets on the Fed have shifted as risks eased over the past week. Futures trading suggests just a 69% chance of an interest-rate cut in 2020. Thursday last week, one cut was fully priced in, with a 13% chance of another one by the end of next year.

The ground is shifting for others, too. As recently as a month back, the Bank of Japan was seen by some as needing to head deeper into negative territory with its policy rate. But now, with the yen weakening past 109 per dollar and Japan’s government embracing a fiscal-stimulus package, things look different.

“We’re perhaps seeing the start of a strong yen decline -- Trump’s tweet, the Brexit results have flipped the yen on its head,” said Vishnu Varathan, head of economics & strategy at Mizuho Bank Ltd. in Singapore. “We could see haven demand wane into 2020. There might be even a last hurrah before the year-end as risk bulls get their way, and push the yen lower from here.”

Bringing hope to both Japanese institutional investors and those the world over is the reduction in the pool of negative-yielding bonds. It shrank to $11.5 trillion as of Thursday, down from the record $17 trillion hit in August when the trade war was raging.

How long the Christmas-time cheer will last remains a question. On three of the key risks, doubts remain. Brave is the analyst that predicts smooth sailing in the U.S.-China relationship ahead; no American presidential candidate is running on the “be nice to China” ticket. Johnson’s looming majority may guarantee the U.K. leaves the EU in January, but the two will still need to negotiate a trade deal, meaning the “hard Brexit” scenario could yet be on the horizon.

As for global recession risks, while the consensus is that growth will pick up in 2020 thanks to this year’s monetary easing and moves in a number of countries to embrace fiscal stimulus, that view isn’t universal. In Australia, an economy closely tied to demand for important inputs including coal and iron, asset managers even see the central bank adopting quantitative easing next year.

And some warn that the U.S. presidential-election season, set to kick into high gear next month in the leadup to the Feb. 3 Iowa caucuses, could pose dangers. The populist platform from onetime front-runner Senator Elizabeth Warren has triggered warnings about the record-setting U.S. bull market for equities coming to an end.

Even if all the good news stays intact, there’s the challenge of valuations. How much gas is there left in the tank after the S&P 500 soared 26% plus in 2019? In credit, U.S. spreads are also historically low.

“I wish we had kept some of the good news for 2020,” Mark Matthews, head of research Asia at Bank Julius Baer & Co., said on Bloomberg TV. “What this is going to do is cause a really powerful rally into the year end, so what’s going to be left over to get priced in to 2020?”

The plethora of riches this week includes Republicans and Democrats getting a bipartisan deal to fund the government before the Dec. 20 spending deadline. Meantime, investors have shrugged off the Trump impeachment story, confident that the Republican majority in the Senate means he’ll remain in office.

For emerging markets, a newly solid Chinese yuan and a retreat in the dollar to the weakest since July offers encouragement. A weakening yuan that dragged developing nations’ currencies down with it had made dollar debt more expensive to service. The yuan Friday traded past the 7-per-dollar line that had briefly spooked markets earlier this year.

“It feels like all the bricks in the wall of worry are falling at once,” said Peter Atwater, president of Financial Insyghts.

--With assistance from Garfield Reynolds, Cormac Mullen, Gregor Stuart Hunter, Tracy Alloway, Ruth Carson and Matthew Burgess.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Joanna Ossinger

©2019 Bloomberg L.P.