China Local Government Unit Sparks Fresh Bond Default Alarm

Chinese Local Government Unit Triggers Fresh Bond Default Alarm

(Bloomberg) -- An obscure Chinese local government financing arm is facing uncertainties over a domestic bond repayment, renewing concerns about a group of risky borrowers that have so far avoided any public debt default.

Yingkou Coastal Development Construction Group Co., a local government financing vehicle from the northeastern Liaoning province, has insufficient cash to cover both the principal and interest totaling 528 million yuan ($74.4 million) on a local bond due May 18, according to a Wednesday report by China Chengxin International Credit Rating. The ratings firm said it maintained Yingkou Coastal’s AA rating but has put the borrower on its watch list.

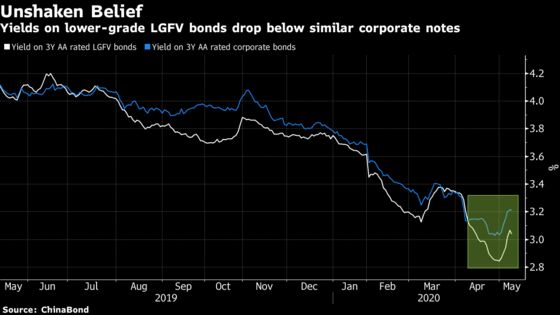

A few small LGFVs have in recent years caused brief scares in China’s bond market, narrowly escaping debt failures after state bailouts. How Yingkou Coastal resolves its imminent crisis will offer important clues on the magnitude of Beijing’s backing for these town builders that are pivotal to its effort to use another infrastructure boom to salvage a recessionary economy.

“Given the policy goal of risk prevention and preserving stability during these special times, the relevant parties’ willingness to look for ways to settle the repayment ought to be fairly strong,” said Yang Hao, a fixed income analyst at Nanjing Securities.

If it ends up with a default, it will have a “big impact” on investors’ sense of security toward the entire LGFV bond market, Yang added. Calls to the debt financing office of Yingkou Coastal went unanswered.

The LGFV had a cash position of 37 million yuan as of March 31, said China Chengxin, adding that there is uncertainty whether the firm can arrange funds for the repayment. The company faces liquidity pressure as its profitability has worsened and cash flow has “dropped significantly”, it added.

Established in 2005 and responsible for local infrastructure projects, Yingkou Coastal is the second LGFV from the rustbelt province of Liaoning that has shown signs of stress in just about a month.

In mid April, Wafangdian Coastal Project Development Co., another small LGFV from the region, issued a new bond to replace old debt, in what analysts described as a first for such borrowers amid concern about their financial strain.

Hohhot Economic & Technological Development Zone Investment Development Group, a peer from the less developed northern region of Inner Mongolia, triggered brief panic in markets late last year after missing an early bond repayment. The company secured an extended deadline from investors a few days later.

Credit Outlook

As Beijing ramps up infrastructure spending to build its way out of the worst economic contraction in decades, these local government financing arms have returned under the limelight.

Chinese LGFVs sold 918.9 billion yuan of local bonds in the first three months of the year, the biggest quarterly gain on record, according to data compiled by Bloomberg.

While easing monetary and credit conditions have thrown lifelines to help LGFVs manage their refinancing needs, the refinancing risk has only been postponed rather than eradicated, according to a report by S&P Global Ratings. The credit outlook on the LGFV sector is biased toward negative, it said.

The local authorities’ capacity to support LGFVs is becoming more divergent, as some lower-tier governments face deteriorating fiscal positions, S&P said.

Buoyant fund-raising will steepen future maturity walls, while weaker LGFVs will continue to see wider spreads and “restrained” access to long-term funding.

Yingkou Coastal reported a net profit of 110.3 million yuan for 2019, down 28.6% from a year earlier, according to the company’s financial statement. Its total assets in 2019 reached 27.5 billion yuan, with total liabilities of 12 billion yuan. Both little changed from the previous year.

©2020 Bloomberg L.P.

With assistance from Bloomberg