Tewoo Debt Plan Shows China Is Allowing State Firms to Fail

China’s Tewoo Seeks Debt Haircut of Up to 64% on Dollar Bonds

(Bloomberg) -- Being state-owned in China no longer means being supported by the state, if the case of a troubled commodities trader is anything to go by.

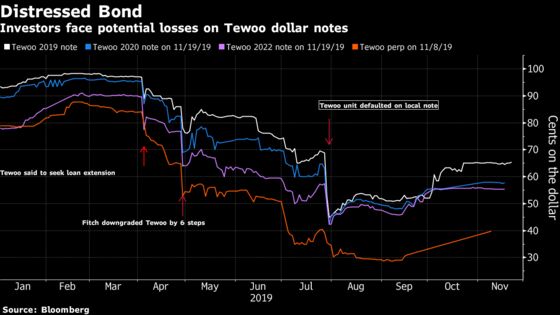

Tewoo Group Corp. proposed Friday that investors either suffer losses as much as 64% or accept delayed repayment with sharply reduced coupons on $1.25 billion of dollar bonds.

The debt restructuring plan is the first of its kind for a state-owned enterprise, and increases the prospect of a default, which would at the very least be one of the biggest by an SOE in the dollar bond market in two decades. The company’s woes also raises fresh alarm about the health of Tianjin, the northern port city in which it’s based.

A de facto default by Tewoo would be considered a “landmark case,” said Cindy Huang, an analyst at S&P Global Ratings. Central government support for SOEs is likely to be selective in the future, while local government aid will be limited by the slowing economy and weaker fiscal position, she said.

The “distressed exchange offer” for Tewoo’s three dollar bonds due to mature over the next three years as well as a perpetual note comes as the borrower is slated to honor repayment on a $300 million bond next month. A large Chinese state bank helped the troubled firm pay a coupon on a $500 million bond last week.

Since the first SOE bond default emerged in China’s domestic market four years ago, 22 such firms have failed to make good on a combined 48.4 billion yuan ($6.9 billion) onshore bonds as of the end of October, according to Guosheng Securities Co. Tewoo’s subsidiary Tianjin Hopetone Co. also missed a coupon payment on a local note in July.

However, despite periodic scares such as late repayment, Chinese SOEs have yet to suffer any high-profile default in the dollar bond market since the collapse of Guangdong International Trust and Investment Corp. in 1998.

Tewoo’s proposed debt restructuring increases investors’ skepticism about state support for such state-linked firms and any default could have wider implications on how investors assess and price their bonds in the future, said Judy Kwok-Cheung, director of fixed-income research at Bank of Singapore.

“Investors would be going back to basics in assessing credit risk in that the company’s stand-alone ability to repay is the first line of defense when it comes to non-repayment risk,” said Kwok-Cheung.

Debt Burden

Aside from the significant “haircut” in cash payment, Tewoo will allow investors to swap its four bonds for corporate papers issued by Tianjin State-owned Capital Investment and Management Co., the city’s state asset manager in charge of managing Tewoo’s offshore debt.

Tianjin has the highest debt burden among megacities and provinces in China, S&P Global Ratings said in July. Earlier this year, Fitch cut ratings on several government-related entities from the city, which is reliant on heavy industry and commodities trading.

Tianjin’s local economy grew by 3.6% last year, the slowest in China, according to United Credit Ratings Co. At the end of last year, Tianjin’s government had 407.9 billion yuan worth of debt outstanding, or about 22% of the size of its economy, said the Chinese credit risk assessor.

Tewoo operates in a number of industries including infrastructure, logistics and mining, according to its website. The commodities trader ranked 132 in 2018’s Fortune Global 500 list.

As of 2017, the company had annual revenue of $66.6 billion, profits of about $122 million, assets worth $38.3 billion, and more than 17,000 employees, according to Fortune’s website.

Neither S&P nor Moody’s Investors Service rates Tewoo. Fitch withdrew its credit risk assessment of Tewoo in July, citing insufficient information and after cutting the firm’s rating by a rare six levels in April.

--With assistance from Rebecca Choong Wilkins and Tongjian Dong.

To contact the reporters on this story: Ina Zhou in Hong Kong at hzhou179@bloomberg.net;Shen Hong in Singapore at hshen87@bloomberg.net

To contact the editor responsible for this story: Richard Frost at rfrost4@bloomberg.net

©2019 Bloomberg L.P.