China's Rich Rush to Shelter $1 Trillion From New Taxes

The reforms, which take effect Jan. 1, are meant to reduce the tax burden on people by making the rich pay more.

(Bloomberg) -- Wealthy Chinese are rushing to shelter assets and income in overseas trusts before new tax rules go into effect next month, including provisions that target offshore holdings.

The Bank of Singapore has seen a 35 percent surge in Chinese clients interested in offshore trusts since the second half of 2018, according to Woon Shiu Lee, head of wealth planning at the bank. The rate of inquiries leading to the establishment of a trust, which offers “tax-planning opportunities” by giving ownership to third-party trustees, has doubled since August, he said.

The reforms, which take effect Jan. 1, are meant to reduce the tax burden on lower-and middle-income people by making the rich pay more. They are also feeding into business for consultants, private bankers and lawyers who specialize in setting up trusts that put ownership of overseas assets at arms-length from a tax perspective.

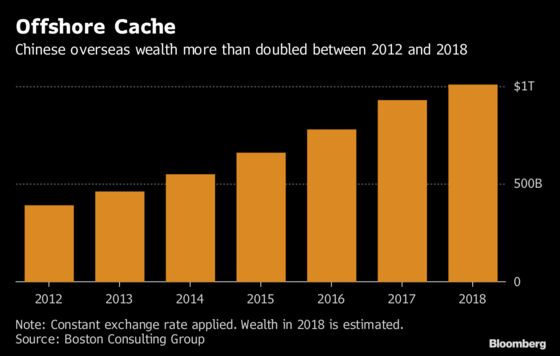

As China’s rich have gotten richer -- the nation’s personal wealth swelled to an estimated $21 trillion last year -- the practice of holding wealth abroad or changing their tax residence status has become commonplace. Even as the government strengthened controls on taking money out of the country last year to reduce risky outbound M&A deals and prevent capital flight, overseas holdings will reach $1 trillion this year, Boston Consulting Group estimates.

“The interest in setting up offshore trusts and canceling Chinese household registration has been enormous,” said Peter Ni, a Shanghai-based partner and tax specialist at Zhong Lun Law Firm. “High-net-worth individuals are rushing to make it before the 2019 deadline.”

Tax Havens

Some of China’s wealthiest are already using trusts.

Wu Yajun, a developer with an estimated net worth of about $7.5 billion, held almost half of her real estate empire, Cayman Islands-registered Longfor Group Holdings, through a family trust. Last month, she moved assets to another trust set up in her daughter’s name, according to a filing.

Other wealthy trust holders include Zhang Shiping, who uses one in the Cayman Islands to hold a majority stake in one of China’s biggest aluminum makers, China Hongqiao Group.

How Trusts Work

| Elements | Process | Result | |

| Third-party trustee | Client, also known as Settlor, conveys ownership to trustee | May leave client with less tax liability | |

| Offshore | For taxpayers in places where wealth-planning trusts don’t exist | Adds layer of protection against third-party claims | |

| Beneficial owner | Eventually, the trustee should distribute income or capital to the beneficial owner | Effectively defers taxes |

Trusts put assets under the ownership of third-party trustees. That can sometimes limit an owner’s ability to make some decisions, but can also help steer away from taxes as high as 20 percent on profits of what Chinese authorities consider “controlled foreign corporations.”

Broader Crackdown

Wealth planning offices aren’t the only ones busied by the reforms. China’s tax authority is also swamped with inquiries.

A representative for the national government’s tax hotline said they are busier this year handling queries.

Alan Jia, chief executive officer at wealth-planning adviser Ishtar Consulting Inc., started helping clients set up trusts well before the latest tax reforms came into view.

“Setting up a trust takes time,” Jia said. “Many of our clients had anticipated the tax reform and reacted earlier on.”

China’s State Administration of Taxation didn’t respond to a faxed request for comment.

In September, China implemented an international data-sharing agreement called the Common Reporting Standard, making overseas money much more visible to mainland officials.

Celebrity Targets

That step meshes with a broader crackdown that swept up some high-profile wealthy Chinese closer to home.

In October, the government made an example of film and TV star Fan Bingbing, hitting her and several affiliated companies with a record $129 million in penalties and back taxes. Other celebrities could face penalties if they don’t come clean on unpaid taxes, the government said at the time.

“Some recent cases in China have further spurred panics,” said Jason Mi, a partner at Ernst & Young in Beijing, who is helping clients plan for the new rules. “Chinese business people are nervously looking at what can be done at the last minute.”

--With assistance from Blake Schmidt, Venus Feng, Alfred Liu, Pei Yi Mak, Yinan Zhao and Shawna Kwan.

To contact the reporter on this story: Jinshan Hong in Hong Kong at jhong214@bloomberg.net

To contact the editors responsible for this story: Young-Sam Cho at ycho2@bloomberg.net, Dave McCombs, Jason Clenfield

©2018 Bloomberg L.P.