China’s Stock Run-Up Throws New Challenge at Credit Market

China’s Hot Stock Rally Throws Fresh Challenge at Credit Market

(Bloomberg) --

Given the option between tapping a recently soaring stock market for fresh funds or selling debt at a higher cost, China’s cash-hungry firms are making the obvious choice.

The divergence in performance between China’s two capital markets has accelerated this month after Beijing encouraged the fastest run-up in stocks since the 2015 bubble burst. Investors are dumping safer assets to buy stocks, triggering another leg higher in corporate yields after a June selloff in government debt spilled over to the credit market.

The yield spread between higher quality five-year corporate bonds and corresponding government papers widened the most in two years this week. At the same time, the ChiNext Index and the CSI 300 Index of stocks both jumped to the highest since 2015.

That’s having a knock-on effect on companies’ issuance plans, in a further blow to the debt market. Chinese firms last month shelved the biggest amount of domestic bond sales in almost three years -- a trend that’s continuing this month -- while equity fundraising is having its biggest year in terms of initial public offerings since 2010.

“The bull market for stocks has just started while the bond market has gone from a small bear market to a big one,” Guotai Junan Securities Co. analysts including Qin Han wrote in a recent research note. “Investors should accept this reality and pursue investment opportunities in equities to make easy money.”

Bonds have been hit by expectations that the central bank will be less generous with credit easing to avoid stoking asset bubbles, and as the economy looks set to return to growth. Shanghai Pudong Innotek Group Co. and Air China Ltd. canceled plans to issue bonds last week, citing market fluctuations and the need to control financing costs, according to filings.

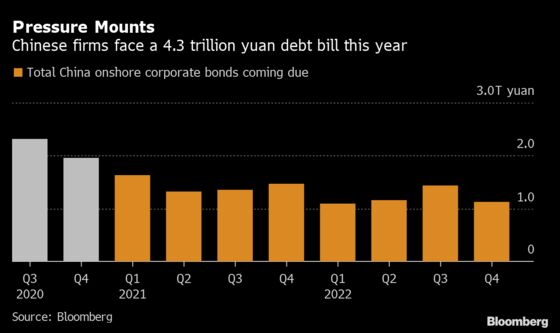

Those market fluctuations couldn’t come at a worse time for issuers of local debt. Borrowers face a hefty maturity wall this year, with firms needing to refinance or repay some 4.3 trillion yuan ($615 billion) of domestic notes, Bloomberg-compiled data show. That’s 13% of all outstanding debt.

On the other hand, Beijing has promoted equity financing as a funding avenue for companies and is keen to maintain a slow bull market to make it sustainable. China’s total fundraising volume from IPOs jumped 223% year-on-year to 208 billion yuan as of Thursday, the most for the period since 2010. On Thursday morning, Semiconductor Manufacturing International Corp. surged 246% on its Shanghai debut, in an offering that is set to be China’s largest in a decade.

One risk to Chinese stocks is that a deluge of new issuance could put pressure on the market later on, when the lock-up period for shares sold in placements or IPOs expire. That’s typically from six months’ time to three years.

“The stock rally is a golden opportunity for companies to build up war chests for business expansion and reduce debt burdens through equity financing,” said Jiang Liangqing, a fund manager at Beijing-based Ruisen Capital Management. “But when lockups expire, such massive fundraising could potentially result in a sell-down of restricted shares.”

| Further reading |

|---|

| China Corporate Bond Selloff Deepens as Funds Move to Stocks |

| China’s Stock Market Is Closing In on $10 Trillion Milestone |

| Chinese Firms Rush to Cancel New Bond Plans as Yields Surge |

| China Set to Post Return to Growth After Easing Lockdowns |

With Beijing imposing some limits on speculative stock trading and taking steps to cool the rally, the window for selling equity at high prices could soon narrow. The CSI 300 Index was 1% lower as of 10:36 a.m. Thursday after losing 2.2% in the previous two days.

For now at least, the recent bullish sentiment in Chinese stocks is allowing the equity market to play a larger role in supporting corporate funding needs.

“The substantial run-up in stocks has given companies more leeway to raise equity funding,” said Wei Liang Chang, a macro strategist at DBS Bank Ltd. in Singapore. “That should help ease liquidity concerns for listed firms.”

©2020 Bloomberg L.P.

With assistance from Bloomberg