China’s Developer Bond Slump Deepens as Selling Spreads Onshore

China’s Developer Bond Slump Deepens as Selling Spreads Onshore

(Bloomberg) -- The selloff in Chinese property dollar bonds intensified on Thursday amid signs of cracks emerging in the nation’s much larger onshore market.

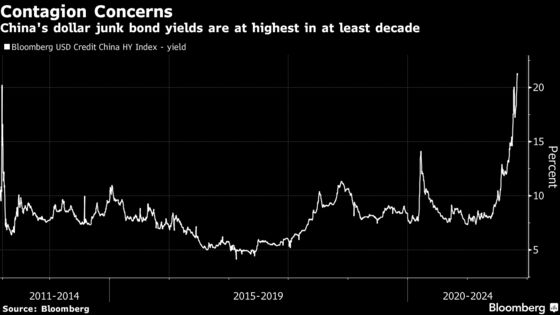

Kaisa Group Holdings Ltd. led declines in the nation’s offshore bonds as a financial product it guarantees missed a payment, while Shimao Group Holdings Ltd.’s 4.75% dollar note due 2022 was poised for its biggest drop on record. China’s dollar high-yield debt fell for the 10th day in 11 after yields climbed above 21%. Trading was halted in two yuan bonds after they plunged more than 20%.

China’s property firms are caught in a vicious circle where surging borrowing costs make refinancing upcoming maturities prohibitively expensive, thereby triggering further losses in their bonds as traders price in potential haircuts. A slowing property market and strict rules on leverage are adding to their challenges, while credit assessors are downgrading the industry’s companies at the fastest pace on record.

“The massive rating downgrades and lack of substantial easing of property curbs triggered the plunge in domestic bonds,” said Zhijun Zhang, chairman of Beijing Dingnuo Investment Management Co. “Concerns are growing about an increasing number of private developers, especially after the dramatic sales slowdown.”

Residential prices fell for the first time in more than six years in September, while the rate of land parcels left unsold surged to the highest since at least 2018.

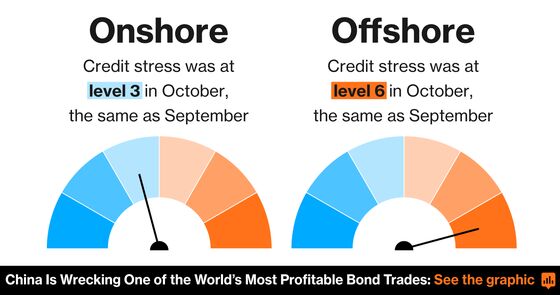

So far the turmoil has been largely limited to China’s offshore bonds. Any evidence contagion is spreading to the nation’s $12 trillion domestic credit market may prompt policy makers to take action to avoid a potential cash crunch. The central bank, which at the end of October injected almost 1 trillion yuan ($156 billion) into the banking system, has been draining liquidity this week.

“The real estate sector is clearly not out of the woods, and sentiment in the onshore market may turn as fragile as offshore,” with more than 300 billion yuan of real estate bonds maturing through the first quarter of 2022, according to Wei Liang Chang, macro strategist at DBS Bank Ltd.

Confidence in the real estate sector -- that by some estimates accounts for nearly a quarter of gross domestic product -- has been worn down by China Evergrande Group’s cash crunch. Chinese borrowers have defaulted on more than $9 billion of offshore bonds this year, with real estate firms accounting for a third of that. The government’s plans to expand property tax trials to cities beyond Shanghai and Chongqing has also frayed investors’ nerves. Officials have yet to provide details on where the tax will be levied or how large it will be.

Key moves:

- Kaisa’s dollar notes plunged and its shares tumbled 15% to a record low as the builder said a wealth-management product it guarantees had missed a payment. The company, China’s third-largest dollar debt borrower among developers, added it’s facing “unprecedented pressure on its liquidity.”

- Shanghai Shimao Co.’s 3.6% yuan note due 2023 closed down 10% at 68.17 yuan and Xiamen Yuzhou Grand Future Real Estate Development Co.’s yuan bond due 2024 dropped 19% to 47 yuan. Both were halted for a time Thursday after falling more than 20%, and they closed at record lows.

- China Aoyuan Group Ltd. shares dropped 7% to a four-year low after Fitch Ratings downgraded the builder by two notches to B+, citing its lack of funding access, “large” maturities and “high” leverage.

There was little sign of panic in China’s domestic financial markets. The CSI 300 Index of stocks closed 1% higher and the yuan rose nearly 0.2% against the dollar.

©2021 Bloomberg L.P.

With assistance from Bloomberg