A Watershed’s Coming for China’s $11 Trillion Bond Market

A Watershed’s Coming for China’s $11 Trillion Bond Market

(Bloomberg Opinion) -- A watershed moment is approaching for China’s $11 trillion bond market: The 10-year sovereign bond yield looks poised to tumble below 3 percent.

The yield slumped to as low as 3.08 percent this month from 3.7 percent in September as the government fixed-income market rallied. The last time it fell below 3 percent for a sustained period was in 2016, when China was battling deflation.

Some mainland investors expect the 10-year yield to go as low as 2.5 percent. If that’s the case, buyers aren’t too late to join the rally. Breaching 3 percent can also be expected to spur an increase in debt sales, aiding Beijing’s efforts to expand the corporate bond market.

Once again, the specter of deflation is around the corner. In November, producer prices rose only 0.9 percent from a year earlier, the slowest pace since 2016. Business sentiment across the board is poor; hiring freezes and job cuts are even affecting the red-hot technology sector.

This round of price declines may well be more stubborn. Back in 2016, the root cause was overcapacity, largely addressed by supply-side reforms that included closing money-losing factories and giving tax breaks to growing industries. This time, the trouble is more structural. The market is already maturing in consumer discretionary segments such as cars, so tax cuts can only go so far.

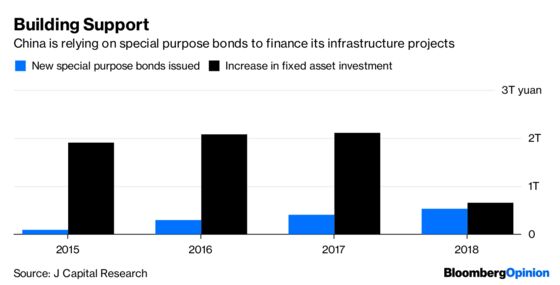

More importantly, Beijing has an incentive to keep its benchmark bond yields low. Increasingly, the government is relying on the debt market to finance infrastructure projects. Special purpose bonds accounted for more than 80 percent of the incremental increase in infrastructure spending last year, up from only 5 percent in 2015, the year of their introduction. Issuance will only be higher this year.

Local government financing vehicles – off-balance-sheet shell companies that carry out stimulus work – have sold debt enthusiastically since 2016. Close to $290 billion will need to be refinanced this year, given that many of these notes have a three- to four-year tenor.

In the fixed-income world, traders look more at spreads than absolute coupon rates. For instance, local government bonds offer an attractive 40 basis points more than sovereign securities of the same tenor, according to Citi Research. A lower base translates to a cheaper cost of financing for borrowers higher up the risk ladder.

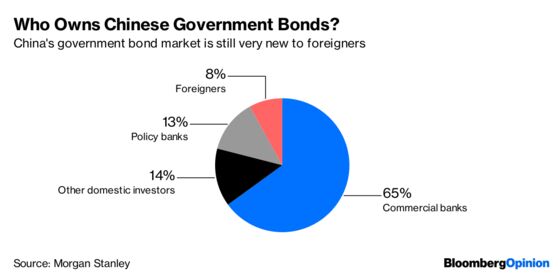

One caveat is whether the government can control the 10-year yield. There should be little doubt on that score. Foreigners hold only 8 percent of Chinese government bonds, versus the combined 35 percent of the U.S. Treasury market that China and Japan own. Beijing merely has to tell state-owned commercial banks to pile in.

China this week allowed the Beijing-based unit of S&P Global Ratings to conduct credit assessments on the mainland, a signal that the government wants foreigners to help finance more infrastructure projects. If overseas investors have no trouble buying the high-yield dollar bonds of Chinese developers, it’s just a matter of time before they venture into the domestic debt market too.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.