China Issues 37 Directives in One Day to Cool a Wild Market

China’s bond market these days - Unprecedented volume, dozens of trading suspensions and daily circuit breakers.

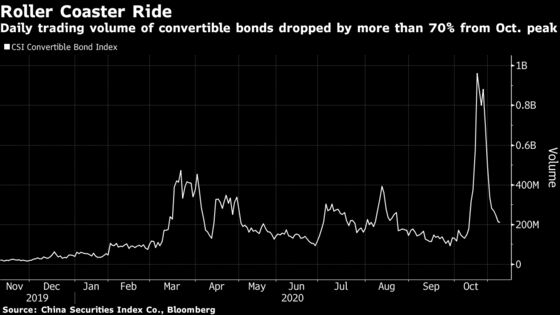

(Bloomberg) -- Unprecedented volume, dozens of trading suspensions and daily circuit breakers: China’s convertible bond market turned so chaotic that regulators released 37 new directives in a day just to calm it down.

While the market is no stranger to bouts of speculation followed by crackdowns from Beijing, wild moves last month included one note that surged as much as 180% in a day before losing more than half its value. Activity has cooled since the China Securities Regulatory Commission released its draft rules on Oct. 23, with Tuesday’s trading volume more than 70% lower than last month’s record high.

The frenzy was blamed on day traders seeking quick profits before the U.S. election. But it was also intensified by the way the market is structured: unlike stocks, there are no price limits on convertible bonds and the securities can be bought and sold on the same day. The mechanism, known as T+0 trading, is favored by speculators because they can profit from intraday fluctuations.

Beijing is considering rolling the mechanism out to its fast-moving equity market, which at $10.4 trillion is more than 100 times larger than the value of outstanding convertible bonds onshore. The concern is that taking equity deregulation so far too quickly could encourage whirlwind trading -- like it did for convertible bonds. In early July, stocks added more than $1 trillion in value after China made it easier to buy shares with debt.

“It could be dangerous to roll out the T+0 trading mechanism to the whole market without sufficient safeguards,” said Jiang Liangqing, a fund manager at Beijing-based Ruisen Capital Management. “Retail investors will face much higher risks, especially for trading small-cap stocks, which are likely to face even higher volatility.”

China’s securities regulator has in the past year removed many of the curbs designed to keep out speculators from its stock market, signaling an end to the highly restrictive era that started when a bubble in the country’s equities burst in 2015.

In the meantime, the regulator has also stepped up efforts to improve the quality of listed companies, so as to shore up investor confidence amid ongoing reforms. The CSRC pledged to improve corporate governance and enhance scrutiny of initial public offerings, according to a statement on its website dated Tuesday.

Different from markets like the U.S. and Hong Kong, China’s stock market carries a T+1 trading mechanism, which means investors can only sell their stocks the day after purchase. Convertible bonds, however, are traded in T+0 and have no daily limit -- similar to corporate bonds and some other derivatives in China. The market watchdog has recently relaxed daily trading limits for some stocks, but is yet to fully remove the restrictions.

| More |

|---|

| China Drafts Rules on Convertible Bonds to Ease Speculation |

| Chinese Convertible Bonds Trigger Trading Halts After 20% Jumps |

| China Convertible Bond Hype Sees $620 Billion Hunt Each Deal |

| China Airline Sets Record With $2.4 Billion Convertible Bond |

Regulators have recently given hints that T+0 trading is coming to the stock market, as part of the efforts to deepen reforms and open up to global investors. Former CSRC chairman Xiao Gang in August said China could pick blue-chip stocks for same-day trading trials, after the Shanghai Stock Exchange said it’s studying a partial “T+0” trading mechanism for its Star board.

But observers call for gradual change. “If T+0 rules are introduced all of a sudden, many small cap stocks may face crazy speculation considering the much larger size of the A-share market compared with the convertible bond market,” said Zou Kun, analyst at Huaan Securities Co.

“If the problems seen in the convertible bond market are anything to go by, the regulator should be cautious.”

©2020 Bloomberg L.P.

With assistance from Bloomberg