China Industrial Firms in Refinancing Fix as Debt Wall Looms

China Industrial Firms Face Refinancing Risks as Debt Wall Looms

(Bloomberg) -- Refinancing pressure is mounting at China’s industrial firms following unprecedented pandemic-induced shocks to the sector and a dearth of bond issuance in the past three months.

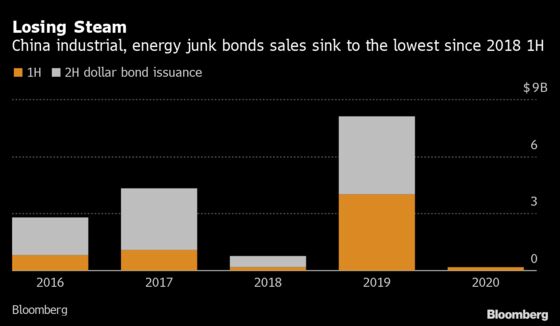

Offshore bond sales from high-yield energy and other industrial companies hit a two-year low in the first half of 2020, with no sales from April to June, according to Bloomberg-compiled data. It couldn’t have come at a worse time for them as $3.1 billion of bonds, or more than a quarter of their debt, need to be repaid or refinanced over the next 12 months, the data show.

Signs of stress are coursing through the industrial sector in the wake of a historic crash in the oil market and a March rout in global credit markets that’s left borrowers in a funding crunch. Potential downgrades will keep investors away from these issuers, which means liquidity may become a problem when the time comes to repay maturing bonds, according to Hong Kong Asset Management Ltd.

“With the global real economy still struggling due to the effects of COVID-19 and the volatility in commodity prices, some issuers in the affected high-yield industrial sectors such as energy services and airlines will continue to struggle,” said Abhishek Rawat, portfolio manager at Hong Kong Asset Management, who is cautious on high-yield industrials from China.

Hilong Holding Ltd. became the latest dollar bond defaulter from the oil sector in June, after an oil refiner from the eastern Shandong province missed a principal installment of a $1 billion loan earlier that month. Hong Kong-listed oil explorer MIE Holdings Corp. defaulted on a dollar note in May.

While yields on China’s junk rated companies have come off multiyear highs, issuance of such debt outside of property has been slow to return in the offshore primary market. Even though oil has recovered and is back at levels last seen in early March, the rebound in fuel consumption has been patchy at best.

While high-yield industrial firms globally are under pressure, firms in Europe and the U.S have not faced the same slowdown in debt sales seen among their Chinese peers, with a 17% and 25% year-on-year pickup in issuance respectively in the first half, the data show.

Investors remain cautious about Chinese firms from the sector, even as UBS Asset Management Hong Kong Ltd. sees yield-starved investors moving into Asia’s junk bond market.

There were seven rating downgrades and negative outlook changes made during the first half of this year, the highest number of negative actions for this period since 2016, according to data from S&P Global Ratings on the Chinese commodities firms they rate.

©2020 Bloomberg L.P.

With assistance from Bloomberg