China Creditor Squeeze Prompts Drop in Record Bond Defaults

China Creditor Squeeze Prompts Slowdown in Record Bond Defaults

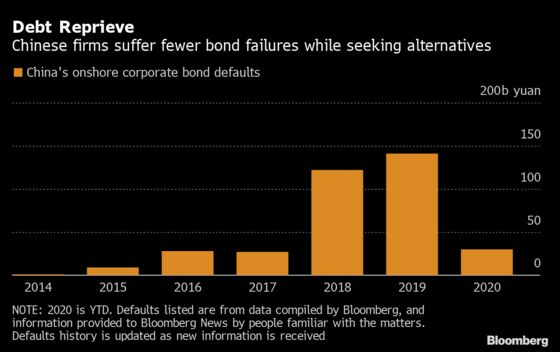

(Bloomberg) --

China’s painful economic shutdown was expected to have put the world’s second-largest bond market on course for a third straight record year of defaults.

But it’s not panning out that way. The 31.4 billion yuan ($4.4 billion) worth of debt that’s gone sour so far this year in the $4.5 trillion onshore corporate bond market marks a sharp 19% drop from the pace in 2019, according to data compiled by Bloomberg.

The turnaround follows a clear signal from Beijing that borrowers should be given leeway as they seek to restructure debt in the midst of an historic economic contraction. In the case of one hastily arranged bondholder meeting by a prominent conglomerate, the strong-arming resulted in an apology. Other deals have gone ahead with little public protest.

In one sense, it’s deja-vu all over again: policy makers had only started in recent years to allow defaults, and to push for bondholder protections in workouts. While nations the world over have moved to avert mass corporate bankruptcies amid the coronavirus pandemic, the risk is that the latest shift in China postpones the emergence of a Western-style bond market.

“Bond covenants lose meaning if bureaucrats may simply impose extra-legal solutions in a crisis,” said Brock Silvers, Hong Kong-based chief investment officer at Adamas Asset Management. “While these measures are certainly rational, they nonetheless clearly illustrate a deep risk for international investors.” Beijing’s influence is much stronger with regard to onshore deals, he added.

Since the start of the year, at least a dozen companies have succeeded or sought to relieve imminent pressure by delaying bond repayments, swapping old notes for new ones or canceling early redemptions, according to data compiled by Bloomberg.

“Deadline extensions and bond swaps can help companies under financial strain resolve short-term liquidity pressure under extreme circumstances,” said Ivan Chung, an analyst at Moody’s Investors Service in Hong Kong. “Behind these measures there’s actually implicit support and guidance by the government” as policy makers seek to stabilize the market, he said.

Among the signals and actions emanating from Beijing, China’s securities regulator said in February it would ask brokerages to “actively guide” investors to help bond issuers via repayment extensions and adjusted repayment cycles. The Shanghai Stock Exchange separately said it would “actively prompt” bond trustees to help issuers reduce liquidity risk by asking investors to accept compromises, such as withdrawing demands for early redemptions.

And last month, China’s interbank market regulator launched a trial project for bond swaps, “in a bid to offer a convenient mechanism for issuers to proactively manage debt.”

| To read more on China’s bond defaults: |

|---|

| Welcome to the $1.5 Trillion Minefield of Defaulted Chinese Debt |

| China Onshore Bond Defaults Ease to $4 Billion in First Quarter |

| China Credit Calm Masks Growing Risks in $5 Trillion Market |

| China Firms’ Bond Payment Plans Signal Shift In Policy Focus |

| China Epidemic Threatens a Broader Wave of Defaults in 2020 |

A slew of companies have succeeded in altering their payment profiles:

- Zhongrong Xinda Group Co., a coal and chemical producer, and Shandong Ruyi Technology Group Co., a high-end clothing giant, won repayment delays, along with agreements from creditors not to label missed payments as defaults.

- Beijing Sound Environmental Engineering Co., a waste-management firm, did a bond swap with investors last month after earlier failing to push through a maturity extension.

- Wafangdian Coastal Project Development Co., a small local-government financing vehicle from the northeastern Liaoning province, issued a new bond earlier this month that it said was for replacing an old security.

Not all borrowers have enjoyed an easy ride. HNA Group Co., one of China’s most high-profile distressed conglomerates, caused a stir last week after narrowly escaping a default by securing a bond repayment delay at a hastily arranged investor meeting.

The investor call was put together at such short notice that many investors found it impossible to even get themselves registered. HNA later apologized for the ill-prepared and widely criticized gathering.

“Investors in China’s bond market don’t have the upper hand,” said Qin Han, chief fixed income analyst at Guotai Junan Securities. “Long bankruptcy proceedings, which could last for several years, make them loath to going through such trouble.”

©2020 Bloomberg L.P.

With assistance from Bloomberg