Cboe Chief Says Early Hedging of U.S. Election Is ‘Unprecedented’

The chief executive officer of Cboe Global Markets Inc. made the observation at a luncheon in New York on Thursday.

(Bloomberg) -- In 30 years at the premier U.S. options exchange, Ed Tilly has never seen an election sow more anxiety than the 2020 presidential race.

The chief executive officer of Cboe Global Markets Inc. made the observation at a luncheon in New York on Thursday. Tilly highlighted elevated demand for protection around important dates in the primary campaign and general vote showing up in the term structure of implied volatility.

“The demand for hedging and hedging vehicles is really amazing,” he said. It’s “unprecedented” this early in an election cycle.

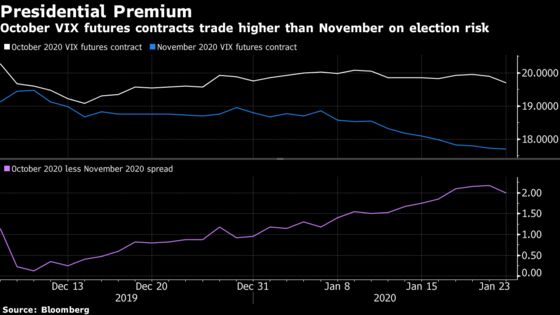

Futures and options tied to the Cboe Volatility Index are among the exchange’s proprietary products. The VIX, or so-called “fear gauge,” measures the 30-day implied volatility of the S&P 500 based on out-of-the-money options prices.

Open interest in the October VIX 2020 futures contract has surged since Jan. 8 to reach 5,866. By Super Tuesday in 2016, the October contract’s open interest was below 400.

These futures are generally in a uniformly upward-sloping curve structure known as contango. But the October 2020 contract, whose expiration value will be linked to options that expire after the general election, trades at a premium of more than 2 percentage points to the November contract.

Back in 2016, the October VIX contract rarely traded at a premium to the November contract.

Wall Street strategists have also observed that the February contract, which will derive its expiration value from options encompassing the Super Tuesday primary votes, has remained stubbornly high because of the eventful political calendar.

Won’t Get Fooled Again

The surprising results of the 2016 election spurred a variety of rare, so-called multi-sigma moves across different asset classes. This time, equity investors aren’t going to be caught making the same mistake. Though, naturally, they could be just as wrong about the market impact this time around.

Pravit Chintawongvanich, Wells Fargo’s equity derivatives strategist, highlighted a bid for implied volatility around the September to December 2020 period as early as August 2019; a high premium around Super Tuesday had built up by November.

The 2016 election “couldn’t keep a bid” in volatility futures because it was presumed that either Hillary Clinton or a generic Republican would win, according to the strategist. After Donald Trump captured the Republican nomination, the former secretary of state was a presumptive “shoo-in” in the eyes of market participants.

“The 2016 elections were not regarded as a real event because the outcome was presumed to be ‘known,’ while the 2020 elections are regarded as a true event,” he said. “The 2020 elections are being very closely watched as each of the plausible scenarios could mean quite different things for future U.S. fiscal policy, foreign policy, the regulatory environment, and by extension U.S. and global economic growth.”

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Lananh Nguyen in New York at lnguyen35@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi, Rita Nazareth

©2020 Bloomberg L.P.