Carry Trade Regains Oomph With Emerging Markets Dodging Fed Squeeze

Central bankers have juiced up carry returns through hikes.

(Bloomberg) -- The hunt for higher yields is all set to return to emerging markets in 2019 as central banks zealously guard their interest-rate advantage over the Federal Reserve.

From Indonesia to South Africa, Mexico and Russia, policy makers have countered Fed tightening with rate hikes this year, sometimes even preemptively. That’s left their currencies with greater risk-adjusted returns for traders who borrow in dollars and invest in developing nations.

Expected carry returns for the next 12 months are rising at a time when the worst rout since 2015 has made currency valuations too low to ignore. But perhaps the biggest surprise is that even after drawing down foreign exchange to bolster their currencies, emerging markets have escaped any serious dents in their reserve buffers.

That means greater probability of returns at lower risk for investors.

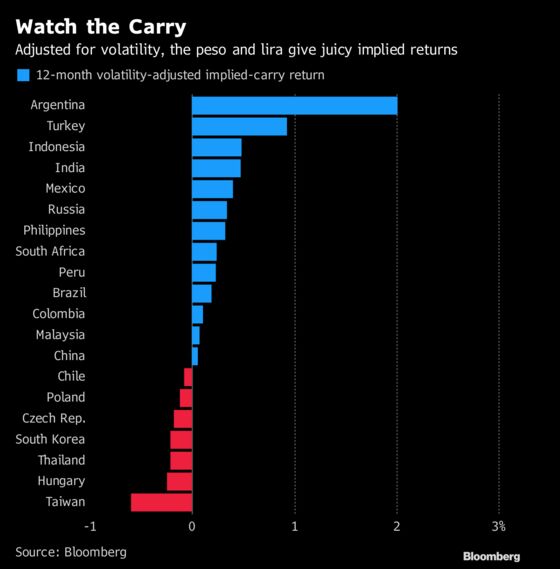

Arbitrage Opportunity

Potential carry returns in the next 12 months, as signaled by non-deliverable forwards and currency options, have risen to multi-year highs in some cases. Thirteen of the 20 major emerging-market currencies assessed by Bloomberg project positive gains even after adjusting for volatility.

- Mexico’s peso and Turkey’s lira offer implied carry returns that are near the highest in a decade as the currencies stabilize after political upheavals

- For Argentina’s peso, the arbitrage opportunity is the best in three years, while for Russia’s ruble, it’s the highest since February

- Countries whose central bankers have stayed dovish and project negative carry are: Hungary, where short-term bond yields are now negative, and Taiwan, which has the worst promised returns across emerging markets

How we got the data: |

|---|

| Bloomberg calculated the difference between one-year implied yields of EM currencies and one-year Libor, and adjusted it for one-year implied volatility. |

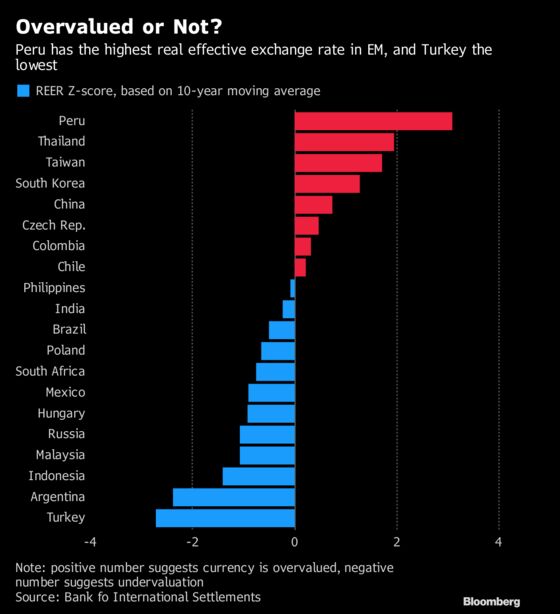

Value Beckons

The 2018 sell-off hit all emerging-market currencies, but the worst was reserved for eastern European, African and Latin American currencies. The outperformance of Asian currencies has left them overvalued. Hence bargain hunters may look elsewhere in the new year.

- Even after their rebound since September, the Argentine peso and Turkish lira are the lowest valued currencies relative to their own past

- The Chinese yuan, Thai baht, Korean won and Taiwanese dollar are looking expensive. That may lend weight to those speculating Beijing will weaken its currency beyond 7 per dollar, especially if the recent trade truce with the U.S. proves short-lived

- With great carry and a cheap currency, Russia is beginning to look irresistible, provided the U.S. doesn’t ramp up sanctions

How we got the data: |

|---|

| Bloomberg analyzed the standard scores of real effective exchange rates from the Bank of International Settlements, based on 10-year averages. |

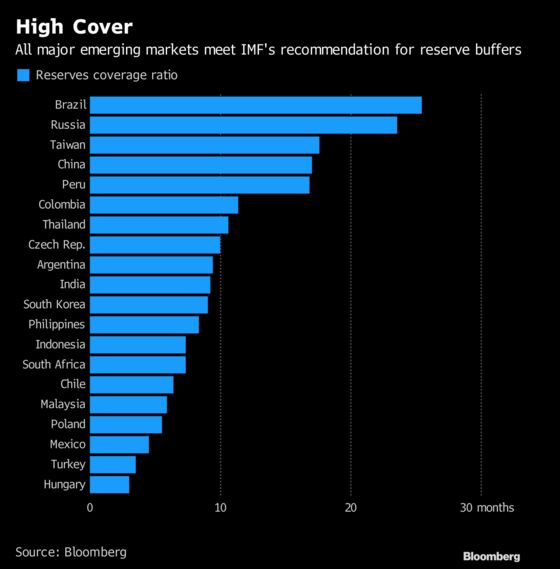

Low Risk

Policy makers in emerging markets have plenty of firepower to defend their currencies if they need to. Central banks for all the 20 currencies have foreign reserves equivalent to more than three months of imports, which is the International Monetary Fund’s recommended threshold.

- Brazil, Russia, Taiwan and China look especially resilient, with coverage ratios of more than 15 months

- Turkey and Hungary have much lower buffers. But Turkish reserves have risen 9 percent since hitting a low in October

How we got the data: |

|---|

| Bloomberg took the local-currency value of each country’s foreign reserves and divided that by the value of monthly imports. |

To contact the reporter on this story: Paul Wallace in Lagos at pwallace25@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Srinivasan Sivabalan, Robert Brand

©2018 Bloomberg L.P.