Carry-Trade Laggards May Win Out Once Volatility Eases

Carry-Trade Laggards May Become Winners in Era of Low Volatility

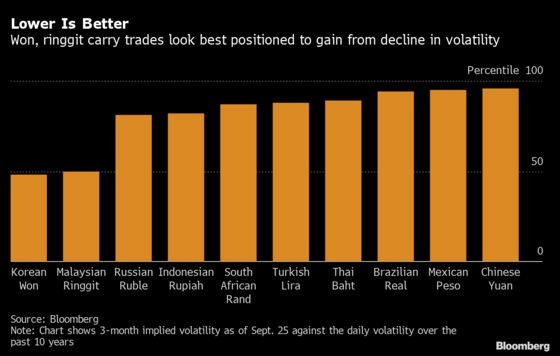

(Bloomberg) -- When the recent spike in volatility starts to ease, watch for these unlikely candidates to emerge as potential carry-trade winners: the low-yielding South Korean won and Malaysian ringgit.

That’s according to a Bloomberg study of 10 emerging-market currencies looking at how current volatility compares with levels prevailing in the last period of super-low interest rates in 2012 and 2013. The analysis found fluctuations in the won and ringgit were closest to the lows from that time, meaning they offer a greater chance of dropping back even further and delivering more stable returns as carry-trade targets.

At the same time, a rush among central banks around the world to cut interest rates to combat the coronavirus has compressed the extra yields offered by countries such as Brazil, Indonesia and South Africa. This is reducing the allure of the more typical favorites for carry trades, a strategy that involves borrowing in a low-yielding currency and investing in one that offers higher returns.

“Many of the usual high-yielding currencies are not that high yielding any more with rates coming down but they’re still volatile, so that makes the carry adjusted by volatility not always very favorable,” said Marcin Adamczyk, head of emerging markets debt at NN Investment Partners in The Hague, whose team oversees $16 billion.

Investors would probably be better off looking at traditional low yielders that have much less volatility, which make the relative risk-reward of going long more attractive, he said, naming the yuan and other currencies in North Asia where growth is rebounding.

Powell’s Pledge

The search for longer-term yield returns comes amid a pledge by the Federal Reserve Chair Jerome Powell to keep interest rates in the world’s biggest economy low for longer even if inflation picks up. The JPMorgan Emerging Market Volatility Index has had a choppy ride this year, surging to an eight-year high in March amid the pandemic outbreak before sliding through the middle of the year and then picking up in recent weeks amid uncertainty over the U.S. elections and a resurgence in virus cases.

The won’s three-month implied volatility measure stands at its 48th percentile compared with its daily average over the past 10 years, while that for the ringgit is around the 50th. In other words, their price swings have been higher more than half the time over the past decade. Similar gauges for the Mexican peso and Chinese yuan are over the 95th percentile.

The Fed’s low-rate regime may help bring down currency fluctuations for the won and the ringgit even further-- closer to the levels last seen during the period from September 2012 through April 2013, when the U.S. central bank engaged in its third round of quantitative easing.

Methodology

- Currency volatility is measured via three-month at-the-money implied volatility options, with the extent of liquidity potentially affecting the pricing of some implied volatility measures

- The average currency volatility is analyzed for the period between September 2012 to April 2013, and is then ranked against daily currency volatility data for 10-years up to Sept. 25, 2020

NOTE: Marcus Wong is an emerging-market strategist at Bloomberg News. The observations he makes are his own and not intended as investment advice.

©2020 Bloomberg L.P.