Buying Cheap Stocks in India Can Prove Very Expensive, ISec Says

“There’s a very low probability for a stock to reclaim its previous high if it has slumped more than 75% from its peak.”

(Bloomberg) -- Buying cheap stocks isn’t rewarding as some bargains may be too good to be true, according to a unit of India’s second-largest private bank.

There’s a very low probability for a stock to reclaim its previous high if it has slumped more than 75% from its peak, analysts led by Vinod Karki at ICICI Securities Ltd. wrote in a note. Only eight of the 228 stocks, which fell more than 75% over a two-year period since 2010, have been able to reach their previous high, the report said.

“The key reason for this behavior is the adjustment to the new reality after original beliefs of the attractiveness of the business model and prospects are shaken, resulting in permanent de-rating of stocks,” the analysts wrote.

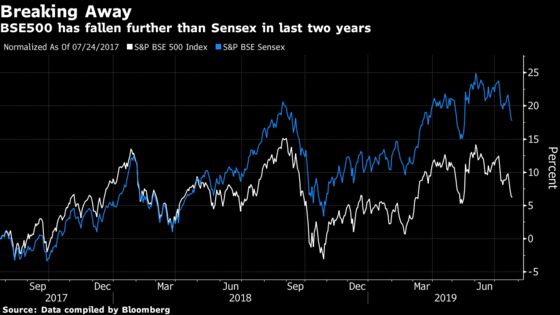

While India’s frontline indexes have posted modest declines from their recent peaks, thanks to gains in only a handful of stocks, the broader market has seen a meltdown in companies with risky debt and poor corporate governance policies. About a third of the S&P BSE 500 Index members have slid at least 50% from their two-year peak, while 41 stocks have seen their market value erode by more than 75%, according to ICICI Securities.

“It is impossible to gauge how low the stock price can go if it is caught in vicious cycle of deterioration in one or a combination of the following factors -- declining operating environment, deteriorating sentiment toward the stock, systemic risk, questions on corporate governance and risk of default,” the analysts wrote.

To contact the reporter on this story: Nupur Acharya in Mumbai at nacharya7@bloomberg.net

To contact the editors responsible for this story: Lianting Tu at ltu4@bloomberg.net, Ravil Shirodkar, Anto Antony

©2019 Bloomberg L.P.