Buy-the-Dip Is Failing in S&P 500, Evoking Bear Market Memories

Buy-the-Dip Is Failing in S&P 500, Evoking Bear Market Memories

(Bloomberg) -- For the first time in more than a decade, buying the dip isn’t working in the stock market.

As a way of measuring it, Morgan Stanley looked at rolling five-day declines in the S&P 500 Index this year and found that on average, the sixth day also generated a loss: of 0.05 percent. While the drop is small, it’s a big departure from the past 16 years, when dips gave way to gains.

It happened again Monday as the S&P fell 0.9 percent as of 10:30 a.m. in New York following a decline last week.

The pattern reflects a subtle deterioration in investor psychology that may not be obvious when you gauge the market by the index’s price level, or through Wall Street forecasts. Despite two 10 percent corrections, the S&P 500 is still up for the year. And 18 out of the 25 strategists tracked by Bloomberg predict the S&P 500 will end 2018 above the record high of 2,930.75 reached in September.

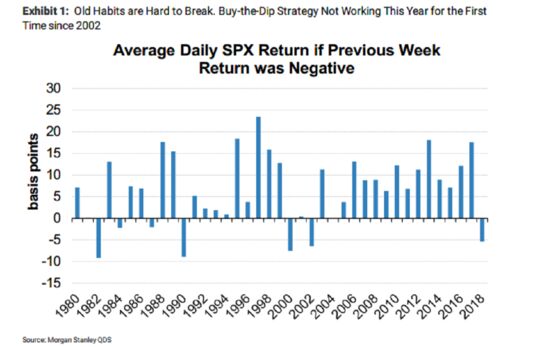

Yet investor sentiment by some measures has reached levels not seen during market crashes. Since 1980, the years when the buy-the-dip mentality was missing all involved bear markets: 1982, 1990, 2000 and 2002. To Mike Wilson, Morgan Stanley’s chief U.S. equity strategist, it’s a sign the market is sussing out troubles ahead, be it economic growth or corporate earnings.

“While 2018 is clearly not a year of recession, the market is speaking loudly that bad news is coming,” Wilson wrote in a note to clients. “Our view is that the market is sniffing out an earnings recession and a sharp deceleration in economic growth.”

With a year-end forecast of 2,750 for the S&P 500, Wilson has been the most bearish strategist on Wall Street. Calling it a rolling bear market, he has predicted that higher interest rates and a less-synchronized global economic expansion would deal a series of blows to financial markets in a pattern that will ultimately hurt leaders such as technology.

Computer and software makers led the October rout after posting gains that more than doubled the market in the first nine months of the year. With the latest tech wreck, over 40 percent of the S&P 500 stocks have fallen at least 20 percent from their recent peaks, meeting one definition of a bear market.

Wilson estimates that 90 percent of the valuation damage from the rolling bear market is done now that the S&P 500’s forecast price-earnings ratio has contracted 18 percent from its December peak. Still, he urged investors to stay away from stocks that have fetched higher multiples.

“The risk from here is much more at the stock level and will likely be concentrated in the higher multiple stocks that do not deserve a valuation premium but have simply benefited from a crowding effect,” he said. “Nvidia’s price action last week is a good example of that remaining risk.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Chris Nagi, Richard Richtmyer

©2018 Bloomberg L.P.