Burst of Buyout Deals Set to Stir Sluggish M&A Debt Financing

Burst of Buyout Deals Set to Stir Sluggish M&A Debt Financing

(Bloomberg) -- A flurry of M&A activity has filled out the pipeline for potential leveraged loan syndication in Europe, as private equity firms put money to work in big chunks.

Financing banks have been discussing some of these situations for many months, going back into late 2018, whereas others have appeared on the radar more recently and now promise a welcome uptick in acquisition-linked loan volume.

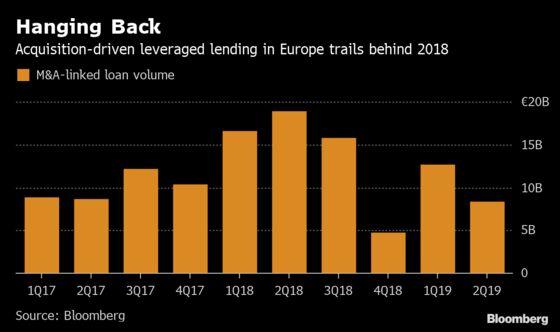

So far this year, M&A-backed issuance in Europe’s leverage loan market is down 41% on the year, at 21 billion euros ($23.7 billion), according to data compiled by Bloomberg. There are still no deals in the pipeline comparable in size to the $13.5 billion package syndicated last September to back the buyout of Refinitiv, but investors could see several large deals come to syndication.

This week brought confirmation that sponsors Bain Capital and Carlyle Group LP have made a bid for Osram Licht AG, while Bain also entered exclusive talks to buy WPP Plc’s Kantar unit. Last week, Merlin Entertainments and BCA Marketplace were the target of take-private bids by equity sponsors. These deals could bring more than 8 billion euros of debt to be placed in the U.S. and Europe, in loans and high-yield bonds--assuming they all go ahead.

Sponsors are also engaged in a number of auctions that could lead to large transactions later in the year, such as Bayer AG’s sale of its animal nutrition unit and BASF SE’s construction chemicals divestment.

Public-to-private buyouts or off-the-run proprietary M&A situations can give private equity firms the chance to spend their dry powder without necessarily having to pay the kind of super-charged valuation that may result from an auction. Of course, these deals don’t always come off, and bankers can work for months on take-privates that eventually fall away.

It’s not entirely smooth sailing for all. Investors’ resistance to the financing for Advent International Corp.’s acquisition of Evonik Industries AG’s plastics division demonstrates that the debt markets are wary of cyclical credits, while banks took their time in agreeing financing terms for the Osram Licht buyout. But a powerful bid from the expanding CLO investor base, coupled with broader demand for the yield offered by sub-investment grade credit, means there is currently deep appetite for leveraged debt.

In the Pipeline

- Osram Licht AG: Bain, Carlyle have made a EU3.4b bid

- Banks Said to Offer Financing for Osram Buyout by Bain, Carlyle

- Kantar: Bain in exclusive talks, valuation ~$4b including debt

- Merlin Entertainments: Blackstone, Kirkbi, CPPIB bid at GBP5.91b enterprise value

- Merlin Debt Financing Includes USD, EUR Term Loans, Bonds

- BCA Marketplace: TDR bid values BCA at ~GBP1.91b

- BCA Marketplace Buyout: Banks Provide GBP1.12b 1L, GBP265m 2L

- Sotheby’s: to be bought by Patrick Drahi in $2.7b deal

- Patrick Drahi May Tap High-Yield Market for Sotheby Funding (1)

- Metro: Investors bid $6.6b for German retailer

- Metro Bid Debt Is Said to Be Set for Leverage Finance Market

- Oriflame: founder family members bid ~$1.3b

- Oriflame Bidder Plans to Raise EU800m-Equiv. Permanent Debt

- Wessanen: PAI makes EU885m take-private bid

- Wessanen Buyout by PAI to be Partly Backed By EU445m of Debt

Read more: EU LEVFIN PIPELINE: LGC, Unit4, Etraveli

(Ruth McGavin is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

To contact the reporter on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, V. Ramakrishnan

©2019 Bloomberg L.P.