Bulls Return to China’s Markets Just as Risks Start to Multiply

Bulls Return to China’s Markets Just as Risks Start to Multiply

(Bloomberg) -- The recent pummeling in China’s markets has made their valuations look attractive relative to almost anything, but bulls may find they need strong nerves to stay the course in a country that repeatedly shocked global investors this year.

The rationale for why much of the sell side is turning more confident on China right now is that things can’t get much worse. Analysts and investors are betting prices already reflect a slowdown in the property market, weaker growth and President Xi Jinping’s campaign to shake up private enterprise.

Yet the drumbeat of negative news threatens to drown out the increasingly upbeat tone found in analyst notes. On Wednesday, Beijing condemned the U.S.’s latest overture toward Taiwan. On Thursday, China’s intervention in coal markets sent futures down by the daily limit. A property stock sank a record 18% amid concern the company may struggle to refinance dollar debts that total $11.6 billion. Investors will find out if China Evergrande Group has staved off default when a deadline to pay a bond coupon comes due Friday.

Peter Garnry, head of equity and quantitative strategy at Saxo Bank, is staying cautious. Credit Suisse Group AG analysts agree, saying it’s “too early to return to China.”

“Our view on China has not changed,” Garnry said. “It is not cheap given the risks in the housing market, debt markets, and changing supply chains. China’s zero covid policy will also continue to create roadblocks for the economy. Plus China’s “common prosperity” will create more distribution, equality, and a less-positive climate for publicly listed companies.”

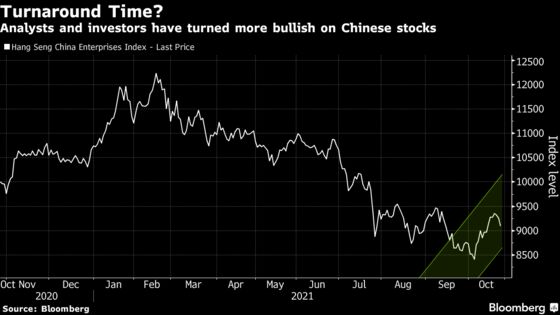

Others are far more upbeat. This month alone, HSBC Holdings Plc, Nomura Holdings Inc. and UBS Group AG turned positive on Chinese stocks, citing reasons including cheap valuations and receding fear of regulation from Beijing. Asset managers BlackRock Inc. and Fidelity International Ltd. are buyers, while Morgan Stanley recommended owning the nation’s speculative-grade debt because prices had fallen too far. Betting on a strengthening yuan is a no-brainer to many currency analysts.

The rebound in October is giving them confidence. Chinese stock gauges are heading for their best month since January. The nation’s junk bonds last week surged the most in 18 months. The yuan is near the strongest in five years against a basket of trading partners.

“Sentiment has largely taken a bigger knock than fundamentals,” wrote Fidelity portfolio manager Dale Nicholls on Oct. 6, one of the first global investors to publicly favor Chinese assets. “Investment is all about risk-reward and for many names, this is looking favourable.”

But growing optimism is no shield against losses -- as seen earlier this year when stock analysts were the most bullish in a decade and tech was so popular that Tencent Holdings Ltd. was briefly worth nearly $1 trillion.

There are plenty of risks. Unlike the rest of the world, China is sticking with plans to eliminate local transmission of Covid-19, even as it battles with sporadic outbreaks. The economy is showing signs of a further slowdown with car and housing sales dropping this month, and a number of economists have lowered their growth forecasts for this year and next.

China is reluctant to stimulate the economy because of a determination to deleverage the housing market and reduce financial risk. The policy has exacerbated the crisis at Evergrande and other indebted developers, with at least four missing dollar debt payments this month. Distressed property firms, which make up about one-third of China’s record dollar bond defaults this year, face a bigger test in January -- when maturities more than double from October, according to Citigroup Inc.

There’s no doubt that Chinese stocks and credit had lagged behind global peers. The MSCI China Index plunged 18% in the third quarter, its biggest underperformance versus the world in 20 years. Xi’s shock moves to take greater control over swathes of the private sector prompted concern that the nation’s stocks would be “uninvestable”. Cathie Wood, founder and chief executive officer of ARK Investment Management, warned that Chinese markets would be under pressure from a valuation perspective for “a long time.” Billionaire George Soros advised investors against bargain hunting in Chinese shares.

Panic turned so severe in the credit market that speculative-grade yields topped 20% and spreads over Treasuries widened to a record -- levels that made little sense to Morgan Stanley credit analysts.

With valuations this low, global funds are returning to China. The MSCI China index still trades at just 1.94 times book value, compared to a multiple of 3 for its global equivalent. The gap is near the widest on record. Investors had turned “too bearish,” wrote HSBC Holdings Plc strategists in a Oct. 26 note.

Buying Chinese assets after such heavy losses can be a winning strategy, as it was for those who did so early last year. The country’s stocks and currency, which had tumbled weeks before the pandemic shocked markets elsewhere, went on to outperform much of the world in 2020.

But in China, momentum tends to shift quickly.

“Reversal trading can conclude what we have observed in October,” Gilbert Wong, Morgan Stanley’s head of Asia quantitative research, wrote in an email Wednesday. “We remind investors again that this rally might prove short lived.”

©2021 Bloomberg L.P.