Bull Market Saved, Central Banks Now Risk an Investor Backlash

Bull Market Saved, Central Banks Now Risk an Investor Backlash

(Bloomberg) -- Central bankers had markets celebrating this week. But to a growing band of skeptics, all they did was extend an artificial sugar high.

Dovish monetary pronouncements from the likes of the Federal Reserve and European Central Bank reignited the bull market this week, sending the S&P 500 Index to a record and U.S. bond yields to depths not seen in two years.

Yet for doubters, it was just more monetary fuel on an already raging fire.

Their fear is that fresh stimulus, in the form of cheaper credit or even further bond-buying, won’t be enough to spark an uptick in chronically low inflation. Instead, it risks pumping up already pricey assets, potentially creating bubbles along the way.

It’s a familiar gripe in the post-crisis era, and just the latest sign of suspicion surrounding this year’s $10 trillion equity rally. But it has a visceral appeal in a week when officials capitulated to market calls for stimulus and the stockpile of negative-yielding bonds swelled to a record $12.5 trillion, recharging the hunt for yield across risky assets.

“This reliance on central banks will take its toll on investors that take too much risk with their portfolios,” said Paul Flood, a multi-asset fund manager at Newton Investment Management, which oversees about 50 billion British pounds ($63 billion). “This will be a huge policy error that’s led to huge unintended consequences.”

The upshot is not all investors think policy makers have the ammunition to spur price growth laid low by the economic fallout of the financial crisis and still hobbled by structural obstacles like aging populations and rising debt.

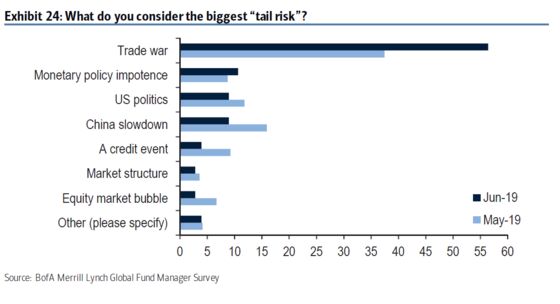

Fears of monetary-policy impotence are increasingly preoccupying money managers with $528 billion between them, according to Bank of America’s June survey. It’s now second only to tariff negotiations on their list of biggest tail risks, and is one reason the U.S. bank reckons sentiment is more bearish than at any time since the crisis.

“After more than 710 interest rate cuts and $12 trillion of balance-sheet expansion since the crisis, central banks have failed to stop deflationary forces,” said Jared Woodard, investment strategist at Bank of America. “Investors are alarmed about the U.S. reliance on monetary policy to stimulate growth and demand-driven inflation because they know the history of Japan and Europe.”

Since the Fed dropped a reference to being “patient” on the policy stance Wednesday and forecast a larger miss of its 2% inflation target this year -- widely seen as the prelude to a rate cut -- bonds have surged. The yield on benchmark 10-year Treasuries dropped below 2% for the first time since 2016 on Thursday.

Bets on a new era of easy money are likewise pumping up stocks and credit this month. In Europe, assets are continuing to surge after ECB president Mario Draghi all but pledged new stimulus for the region’s sluggish economy on Tuesday.

But follow the money, and you can see big bets on the impotence of central banks, according to Woodard.

“The investment playbook is a simple return to the deflation versus inflation trades of the last several years: long government bonds, corporate credit, large-cap equities (esp. growth); short commodities, inflation-protected bonds, value stocks,” he wrote in an email.

In other words, Wall Street is continuing its obsession with casting central bankers as the masters of financial universe, responsible for all manner of gyrations from commodities and long-dated bonds to cheap stocks.

Investors are piling into more defensive stocks amid fears of an economic slowdown -- an implicit bet looser policy can’t redress late-cycle excess. Record inflows into government debt are making the likes of BNY Mellon’s Newton Investment Management curb their exposure to developed-market bonds in favor of emerging markets, citing bubble-like valuations.

One of the biggest question marks hangs over Europe, where there has long been a bearish mantra that the ECB is low on ammunition. The region’s deposit rate was cut to an unprecedented low of minus 0.4% in 2016, while the stimulus program hoovered up so many government bonds that supply became an issue.

Roelof Salomons, chief strategist at Kempen Capital Management NV, says any ECB policy reduction from here will yield little benefit to the real economy.

“We fear that one or two cuts won’t be enough and they’ll have to cut even more because there’s already more weakness in the economy than we see,” said Salomons. His firm cut equities to underweight in May due to growth concerns, and favors emerging-market debt.

Still, fresh QE could pack a punch for financial assets, boosting the credit rally anew. ING Groep NV strategists including Jeroen van den Broek suggest that the ECB could deliver stimulus by restarting its corporate-buying plan, expanding it to include bank bonds.

“Even though a restart of QE would fall into the category ‘more of the same’, we would be very cautious calling Draghi an emperor with new clothes,” they wrote. “In our view, the emperor is not naked at all; he has corporates, and banks.”

To contact the reporters on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net;David Goodman in London at dgoodman28@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, ;Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.