The $1.8 Trillion Global Payout Ride Is Coming Back to Earth

Bull Market's Trillion-Dollar Dividend Ride Comes Back to Earth

(Bloomberg) -- For Lode Devlaminck, it was the turning point -- the moment corporate titans and their shareholders had to pay for the excesses of the credit cycle.

In October, Anheuser-Busch InBev NV halved its dividend after the world’s largest brewer confronted mounting fears over a $109 billion debt burden. Just days later, General Electric Co. slashed quarterly payments to a penny a share in a dramatic bid by the leverage-laden behemoth to bolster its balance sheet.

“Those two were like, holy cow, what’s going on?” said Devlaminck, managing director of global equities at DuPont Capital Management. “And then people started looking and screening for other companies that might be at risk next year.”

As the sugar high from U.S. tax cuts fades and earnings growth eases, Wall Street is sounding more conservative on one of the bull market’s sure-fire ways to outperformance: Corporate payouts.

In the new era of prudence, shareholders who’ve enjoyed fatter and fatter dividend checks can rest easy no longer.

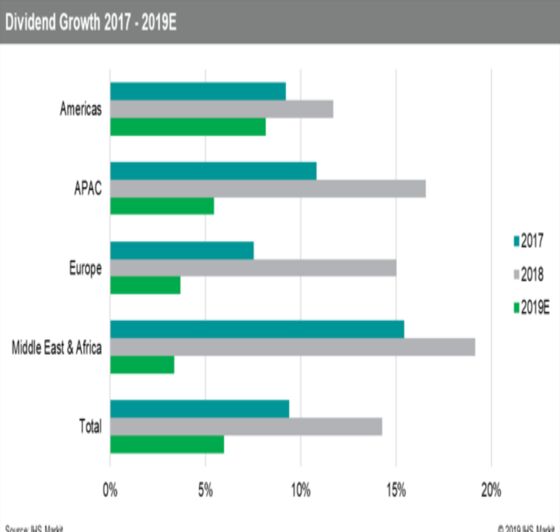

IHS Markit Ltd. last week projected a “significant slowdown” in global dividend growth this year, at 5.9 percent, totaling $1.8 trillion, according to a bottom-up analysis of over 9,500 firms. Thanks in part to mounting geopolitical risks, that’s a shift from the 14.3 percent boom in 2018 and 9.4 percent the year before.

The business-information provider reckons about 11 percent of firms will announce a dividend cut this year -- an uptick of almost 100 names relative to 2018.

“I believe that dividends of leveraged companies can suffer more,” said Willem Sels, a London-based chief market strategist at HSBC Private Bank. “The excessive focus on the shareholder value at the expense of bondholder value will be more muted.”

Goldman Sachs Group Inc., for its part, reckons the S&P 500’s dividend-per-share growth will come in at 6 percent this year versus the projected 11 percent in 2018.

As higher rates weigh on companies, sacrificing such payouts may be the last resort for those on the defense after exhausting cost-cutting measures.

Morgan Stanley last month cited Ford Motor Co. and Hoist Finance AB as potential candidates for cuts after the likes of GE, AB InBev and Dixons Carphone Plc.

“Some companies thought that they didn’t need to take care of their balance sheets, because they could borrow more at cheap rates,” said Jorik van Den Bos, a portfolio manager at Kempen Capital Management.

Shifting Sands

Still, for all the risk aversion in global markets, plenty of money managers are ready to support shareholder-friendly activities. Just last week Fox Corp. sold nearly $7 billion in bonds to help finance a special dividend related to its acquisition by Walt Disney Co. And the comeback in junk bonds and risky stocks in the new year suggests late-cycle disdain for debt may be overstated, for now.

Abruptly cutting dividends can also backfire, hitting equity values and borrowing costs.

“If you just reduce the extent of your stock buyback program -- relative to a record year last year -- then I think executives would hope that this wouldn’t be punished to the same extent,” said Michael Bell, global strategist at JPMorgan Asset Management.

All that said, treasurers have good reason to think the interests of bondholders and equity investors are increasingly aligned. With the median net debt to EBITDA ratio of the S&P 500 climbing to 1.8 times from 0.8 at the start of 2006, markets are punishing companies with elevated leverage, hurting equity holders in kind.

U.S. companies with weak balance sheets have underperformed those with strong financials in recent months, a reversal from the post-crisis trend. It’s easy to see why: Angst over corporate debt is at the highest since 2009, according to Bank of America’s most recent survey. Half of the respondents would prefer companies to use cash to improve their financials, with just 13 percent prioritizing payouts to shareholders.

The equity rout may have also given treasurers some cover, according to Kristina Hooper, chief global strategist at Invesco Ltd. “Most companies’ stock prices are at lower levels than they were a year ago, making their dividend yields higher and therefore taking pressure off companies to raise dividends,” said Hooper, who helps oversee about $888 billion of assets.

Over at DuPont Capital, Devlaminck is helping to scrutinize how the firm’s $26.7 billion in assets are exposed to this brewing shift in corporate behavior -- and sees late-cycle risks multiplying. He prefers defensive and quality shares over those that traditionally offer higher payouts.

“Cutting back on your dividend or buyback never solves your balance sheet issue, it just stops it deteriorating, or keeps it stable,” he said. “It’s not like all of a sudden you’re this great company."

To contact the reporter on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Sid Verma, Cecile Gutscher

©2019 Bloomberg L.P.