Bull Market Was Already Wheezing When Trump's Trade War Landed

The trade war with China has come at a particularly delicate time for corporate America.

(Bloomberg) --

The trade war with China has come at a particularly delicate time for corporate America.

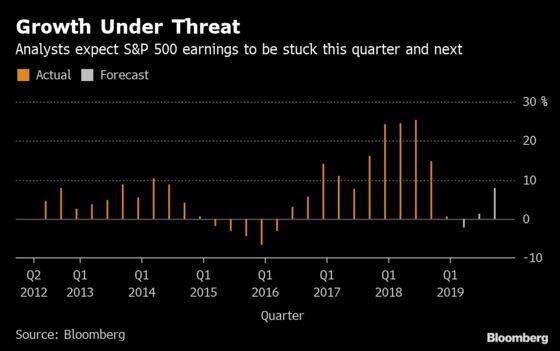

Beset by a down cycle in technology, earnings in the S&P 500 came very close to falling in the first quarter -- and it doesn’t get any easier from here. Growth is forecast to be virtually zero for this quarter and next, and the last thing bulls needed was an exogenous trauma making it worse.

Now, it seems, that is what they’re getting. For a taste of potential hazards, look at the technology industry. Days after the Trump administration’s ban on Huawei Technologies Co., chipmakers from Lumentum Holdings Inc. to Qorvo Inc. have slashed their sales forecasts, citing lost sales to the Chinese telecom giant. Meanwhile, analysts warned Apple Inc. could face retaliation amid growing national sentiment in China.

While growth was never going to be robust for the full-year, some Wall Street strategists say it may be non-existent.

“There’s the potential to have a negative impact on the economy from trade and you can see those earnings estimates continue to go lower,” said David Spika, president of GuideStone Capital Management. “The market’s got to price that in.”

Right now, companies in the S&P 500 are expected to earn $167 a share this year, an increase of about $7 from 2018, analyst estimates show.

In the case of a full-blown trade war, profits for the next 12 months could take a hit of $9 a share, sending the S&P 500 down to 2,550, JPMorgan estimates. Sanford C Bernstein & Co. says that a permanent increase in tariffs on Chinese goods would raise costs for American firms, shaving $4 to $8 from next year’s income.

For now, it’s not a scenario that traders are bracing for. Despite three consecutive weeks of losses, the S&P 500 has managed to hold the 2,800 level, sitting about 5% from its record high reached in April.

Trade tensions are flaring at a time when earnings sentiment is already fragile. Among S&P 500 components that have provided guidance for the second quarter, more than half said earnings are likely to be weaker than expected, according to Bloomberg Intelligence. That’s more than three times the number of companies that expected improvements.

With global demand already sagging and costs on everything from labor to shipment rising, the trade spat is probably the last thing executives want to deal with.

Retailers, in particular, have stepped up efforts to urge President Donald Trump to reconsider his belligerence. In an open letter earlier this week, Nike Inc. and some 170 footwear companies called his trade policy “catastrophic.”

Department-store chain Kohl’s Corp. partly blamed an 11% cut to its profit outlook on rising tariffs on Chinese goods. Home Depot Inc. estimated that the hit to product costs could be $1 billion a year. J.C. Penney Co. said further escalation -- especially if the latest proposals on apparel and shoes go into effect -- would have a “meaningful impact.”

Companies might be able to pass on the extra costs to consumers by charging more. While a 25% tariff on Chinese imports would crimp S&P 500 earnings by as much as 6%, the lost income could be recovered through a 1% increases in prices, according to estimates by Goldman Sachs.

Will they? Mike Wilson, a strategist at Morgan Stanley, says no. Given stubbornly low inflation, he argues, companies may be forced to cut labor costs instead to salvage margins, a move that could lead to a spike in unemployment and ultimately an economic recession.

Another hazard is that the trade war drags on and equities sell off in the face of persistent uncertainty, hurting consumer and corporate confidence. In recent days, analysts at Nomura, JPMorgan, and Goldman Sachs have rewritten their forecasts, saying the issue will take longer than anticipated to resolve. And a Chinese government expert predicts tensions could last until 2035.

“While at some point a market ‘circuit breaker’ may make concessions more likely on both sides, this path requires market stress and volatility preceded de-escalation,” Wilson wrote in a note. “That stress will only amplify the second order effect” and “add to an already difficult earnings growth environment,” he said.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.