Brazil Stocks Win Over Fund Managers as Chile Is Left Behind

Brazil Stocks Win Over Fund Managers as Chile Is Left Behind

(Bloomberg) -- Money managers are betting Brazil’s stock rally will continue, while Chilean shares still look expensive even after a terrible first half of the year.

Latin American stocks beat the emerging-market average in the six months through June, lifted by outsize gains for utility, consumer and finance shares. But the performance of individual markets varied widely, from a 38% jump for Argentina’s Merval to a 1.3% drop for the benchmark in Chile. Investors say geographic allocation will be key to outperforming in the second half.

“Valuation is the primary driver on my underweight in Chile,” said Will Pruett, a Boston-based money manager at Fidelity whose $553 million Latin America fund has returned 27% over the past year, easily beating the region’s benchmark. “Brazil is clearly early cycle, coming out of a recession. Inflation is low, rates are low and potentially coming down.”

Investors have been rewarded with an 18% jump this year for the Ibovespa. The benchmark stock index for Latin America’s largest economy may see further gains on the back of government efforts to shore up its finances as well as tame inflation and record-low interest rates. Traders are paying close attention to how a relatively robust social security reform -- which is seen as crucial for the nation to tackle its budget deficit -- fares in a divided congress.

JPMorgan Chase & Co. is optimistic on the country. For the first time, all of its analysts’ top picks in the region are Brazilian companies -- except for the sectors that don’t have stocks from the country.

“Behind these choices is the view that reform approval paves the way for higher growth and lower country risk,” Emy Shayo, a Sao Paulo-based strategist, said in a report last month.

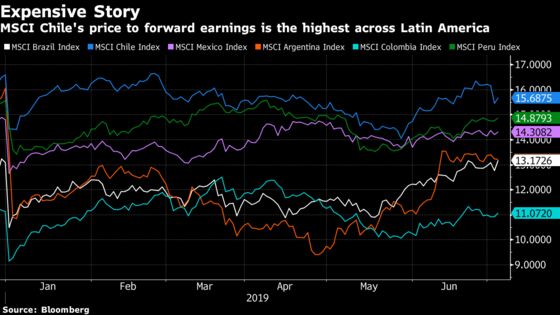

For Chilean stocks, Itau BBA sees little to be excited about given weak earnings momentum. Even after a poor first half, the price-to-estimated-earnings ratio for stocks in the MSCI Chile Index is 15.7, the richest multiple in the region.

“We see unsupportive market dynamics for pulp prices and cooper, which is likely to weigh on earnings this year,” strategists led by Pablo Ordonez wrote in a report from July 1.

Here’s what some other investors have been saying about Latin American stocks:

BTG Pactual, Cesar Perez-Novoa

- Optimistic on Brazil and Peru.

- In Chile, a drop in consumer and business confidence has hurt investments.

- Global uncertainty limits allocation to the Chilean market.

Fidelity, Will Pruett

- Valuations are high in Chile; recent rate cut should be good for economic activity, but the currency is susceptible to trade flows.

- Positive on Brazil as rates can potentially come down; economic slack in the system may increase margins when demand picks up.

- Mexico is more attractive now than it was six months ago; there are well-run banks trading at an attractive valuation.

- Pruett also likes Prevuan banks.

- “It’s all about the election” in Argentina.

JPMorgan, Emy Shayo

- Second-half focus should be on the implementation of policies that drive faster growth.

- “Brazil is doing it, Chile and Colombia are trying to, and Argentina wants another chance to do it.”

- Approval of pension reform should drive Brazil investors to focus on growth rebound and the next batch of macro structural changes.

Mirae Asset, Malcolm Dorson

- Underweight Chile, overweight Brazil, slightly underweight Mexico.

- “We are more favoring other countries than avoiding Chile.”

- Valuations are high in Chile and exposure to cooper adds another layer of volatility.

- If Chile can move forward with significant reforms, it would boost sentiment among investors.

- Chile’s recent rate cut makes a compelling story for a few stocks, like Mallplaza, Cencosud and Falabella.

- Colombia is cheap right now but it’s a proxy to oil prices; there are some internal reforms that could be very good.

- Remains on sidelines in Argentina.

- As Brazil moves beyond pension reform, there should be a boost in consumer confidence and a new capex cycle.

Victory Capital, Michael Reynal

- “We have been disappointed at the slow progress in pension reform and the negative revisions to GDP growth” in Brazil.

- “Ironically, we are overweight Brazil due to bottom up stock.”

Zurich Asset Management, Giovanna Musa

- Chile lacks local triggers; there aren’t turnaround stories.

- Doesn’t expect a significant change in macro trend and corporate earnings.

- Mentions operating leverage in Brazil.

- “Companies have been able to get a lighter operating structure.”

- There are more external risks in Mexico.

- Argentina is a binary case; it’s too early to predict the election results.

To contact the reporters on this story: Vinícius Andrade in São Paulo at vandrade3@bloomberg.net;Eduardo Thomson in Santiago at ethomson1@bloomberg.net;Maria Jose Campano in Santiago at mcampano@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Brendan Walsh, Richard Richtmyer

©2019 Bloomberg L.P.