Bored With Shorting VIX? New ETF Offers a Credit-Volatility Bet

Bored With Shorting VIX? New ETF Offers a Credit-Volatility Bet

(Bloomberg) -- The short-volatility complex is coming to corporate debt ETFs.

An exchange-traded fund that will test appetite for credit volatility as a standalone asset class arrived this month, smack in the middle of the calmest junk-bond markets since October.

Tabula Investment Management is behind the London-listed fund, offering traders a fresh way to bet against gyrations in the global credit cycle on the heels of dovish central banks and the Goldilocks-lite economy.

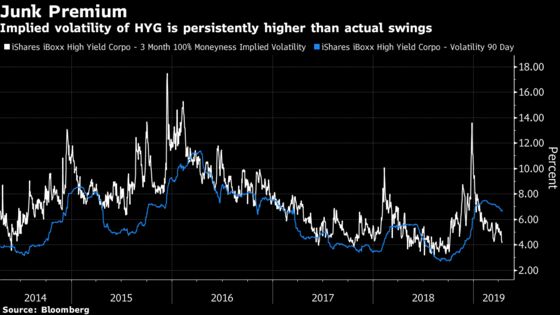

The 50 million euros ($56 million) product, ticker TVOL, aims to deliver steady gains so long as markets demand a higher cushion for price swings on speculative-grade debt compared with what comes to pass, or the volatility-risk premium.

This dynamic -- selling volatility when it’s high and waiting for it to deflate -- has spurred the post-crisis boom in financial instruments tied to shorting equity swings. Now it offers ETF traders income in the potentially more-stable world of fixed-income options.

“The premium available has been relatively persistent over the last 10 years,” Michael John Lytle, chief executive of Tabula, said in an email. “Most of the time it has also been larger in credit than in equity.”

The Tabula product tracks a JPMorgan Chase & Co. index that simulates the returns of selling a so-called options strangle on a pair of credit-default-swap indexes referencing high-yield markets. The underlying index has returned an average 2.9 percent over the past five years but has posted losses over the past 12 months, a period that coincided with the fourth-quarter meltdown in risk assets.

More Buyers

The relative dearth of options sellers on the swap indexes relative to options buyers is one reason why the trade potentially offers attractive risk-adjusted returns, according to the issuer.

The market-neutral strategy will make money as long as the swaps swing less than the expectations embedded in the price of the options. The risk -- as in all short-vol trades -- is that a volatility eruption will leave sellers holding the bag.

Equity traders learned that the hard way when an explosion of market tremors in February 2018 sent the value of several popular short-VIX exchange-traded products to zero.

One saving grace is that “drawdowns in credit have tended to be less severe than in equity,” according to Lytle.

The Tabula ETF seeks to open up a trade that’s been the province of specialists to a broader audience. Typically, shorting credit vol requires a manager. A systematic program of selling contracts on the swap indexes necessitates sophistication and infrastructure, as does the more widespread strategy of selling options on high-yield bond ETFs.

With shares initially priced at 10,000 euros each, the product is principally aimed for professionals. But the anemic trading volume is proving a barrier to some. At Credence Capital Management, Yannis Couletsis sees “potential” in the ETF but limited trading volumes could make selling the fund “strenuous if trying to get out on a nervous day,” he said.

“We think one has to trade that market,” said the volatility manager. “Get in, get out, revisit in the next opportunity.”

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2019 Bloomberg L.P.