Bonds to Fight New Virus Help Chinese Firms Repay Old Debt

Bonds to Fight New Virus Also Help Chinese Firms Repay Old Debt

(Bloomberg) -- Chinese companies are flocking to issue new bonds in the name of fighting the coronavirus, taking advantage of a policy easing by Beijing to mobilize financial resources to contain the nation’s worst public health crisis in 17 years.

But a closer look at the latest boom of the so-called “anti-epidemic bonds” shows that the borrowers will use the bulk of the proceeds for rolling over old debt, instead of directly funding efforts to get the epidemic under control.

Speedy regulatory approvals of the new special debt, as well as lower borrowing costs due to support from state-backed investors, also have prompted some issuers of regular bonds to market their deals by adding a flavor of the fight against the disease.

Regardless of the issuers’ motivation, the frenzied rush to raise funds betrays the huge pressure on Chinese firms to secure refinancing as a weakening economy, now hit further by the epidemic, heightens the risk from an expanding pile of corporate debt.

Since late last month, top regulators from China’s central bank to the country’s securities watchdog and economic planning agency have rolled out schemes collectively known as the “green passage” that encourages bond financing for the fight against the deadly virus.

Companies either hit by the epidemic or those involved in the campaign to contain it qualify for applying for such bond sales, with regulators pledging to expedite and streamline the approval process.

At least 11 companies, ranging from drug makers to airlines and construction firms, have either sold or applied for selling the “anti-epidemic bonds” as of Monday, targeting to raise a combined 9 billion yuan ($1.3 billion) from the debt issuance, according to data compiled by Bloomberg.

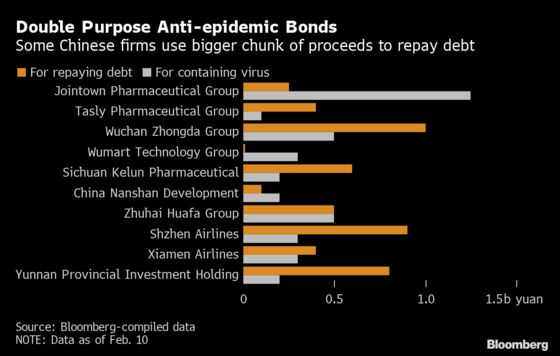

Among the total, 3.95 billion yuan, or 44%, is earmarked for disease control, ranging from manufacturing of medical equipment to building hospitals and outright donations, the data show. The rest, however, is for refinancing.

Easing Debt Pressures

Chinese regulators appear to have varied and relatively vague criteria for the use of such bond sales: the country’s economic planning agency allows borrowers to use proceeds to repay loans meant for containing the virus outbreak; the interbank market regulator says at least 10% of the funds must go to disease control, while the Shanghai Stock Exchange doesn’t publish quantified criteria.

“In terms of the use of proceeds, the ‘green passage’ bonds would to some extent relieve the companies’ short-term debt repayment pressure, in addition to supporting their funding for fighting the epidemic,” Sun Binbin, an analyst at Tianfeng Securities Co., wrote in a recent research note.

For example, Yunnan Provincial Investment Holdings Group Co., a local government investment arm of the southwestern province, said it will use one fifth (200 million yuan) of the 1 billion yuan bond it plans to issue to purchase medical devices and drugs, as well as for using its hotels to accommodate stranded tourists. The remainder of the funds raised will be for repaying existing debt, it added.

Tasly Pharmaceutical Group Co., a traditional Chinese medicine producer, announced that it aims to use 80% (400 million yuan) of its 500 million yuan “anti-epidemic” bond for refinancing.

Similarly, Shenzhen Airlines Co. and Xiamen Airlines Co. also have earmarked 75% and 57%, respectively, of the proceeds of their planned bond sales for servicing old debt.

Appealing Label

The strong regulatory backing for the “anti-epidemic” bonds also appears to have given issuers of regular corporate notes incentives to promote their fundraising plans by associating themselves with the public health campaign.

When marketing its 1 billion yuan regular bond deal, Guangxi State Farms Group, a sugar miller and alcohol producer, flagged its decision to adjust its alcohol production line to manufacture more disinfectants as part of its contribution to the fight against the virus outbreak. The bond’s marketing materials highlighted that the borrower is one of the biggest disinfectant producers in the region so as to gain support from investors, according to people close to the deal.

An official at Guangxi State Farms Group’s financing department said the company has used bank loans for containing the virus outbreak, adding that proceeds from the bond sale aren’t meant for such purposes.

“We can’t rule out that some companies may use the anti-epidemic concept to facilitate their bond issuance but there are certain criteria for ‘anti-epidemic bonds’ and only those with designated use of proceeds can be called that,” said Zhou Yue, an analyst at Sinolink Securities Co.

Echoing concerns about potential abuse of the special new bonds, the state-run China Securities Journal appealed in a front-page article Thursday for “good use” of such bonds and preventing “some people from catching fish in muddy water.”

Debt Wall

The collective enthusiasm about issuing such bonds reflects a larger problem faced by the world’s second-largest economy: A total of 6.8 trillion yuan worth of corporate bonds are set to mature this year, the second-biggest amount after last year’s record 7.6 trillion yuan, according to data compiled by Bloomberg.

Early results suggest the new initiative is paying off: most issuers managed to sell their special new bonds at cheaper costs due to robust demand from state-run banks and financial institutions, often at the authorities’ encouragement.

In such an example, a 800 million yuan “anti-epidemic” bond sold by Sichuan Kelun Pharmaceutical Co. last week fetched a coupon of 2.9%, 107 basis points lower than the rate on a similar note issued by the company in August.

Investors from the private sector, however, remain cautious.

“It’s easier for companies with the label of anti-epidemic bonds to receive regulatory approval but I think the help is limited when it comes to raising funds in the market,” said Wang Hu, a partner at Shanghai Junxi Capital, a private investment fund. “At the end of the day, investors still pay attention to the fundamentals of a company.”

To contact Bloomberg News staff for this story: Tongjian Dong in Shanghai at tdong28@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net;Zheng Li in Shanghai at zli698@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, Shen Hong, Chan Tien Hin

©2020 Bloomberg L.P.

With assistance from Bloomberg