Bonds Calling the Shots for Stocks as Rate Cuts Outweigh Trade

Bad news is good again. As long as it doesn’t involve China.

(Bloomberg) -- For investors who see this year’s stock rally balanced on the twin pillars of easy money and peace in the U.S.-China tariff war, well, at least one’s still standing. For the last three days, that’s been enough.

The worst stretch since Christmas, sparked by the crumbling trade truce, has been followed by the second-best run this year as traders priced in diminished rate expectations. Will it last? Who knows. But with Twitter quiet and the 10-year yield hovering at 2.4%, it hasn’t taken long to put last week’s battered bulls back on the scent of a melt-up.

“There’s potential for appreciation in the stock market, and I do think we could be looking at another positive year,” said Chicago-based Susan Schmidt, head of U.S. equities at Aviva Investors. “If anything, the Street now expects there might even be an interest-rate cut, which is the polar opposite of where we were six months ago.”

At that time, the worst quarter for stocks in a decade was underway with 10-year Treasury yields above 3%. Now, money lost during the fourth-quarter rout has been entirely restored, and odds of an easier Fed have brought rates down to multi-month lows.

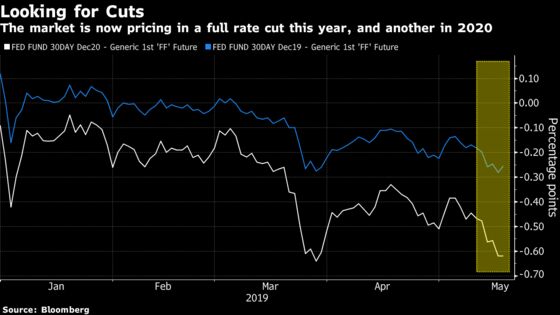

Bad news is good again. As long as it doesn’t involve China. Weak retail sales and industrial production prints Wednesday sent yields on two-year notes to the lowest levels in more than a year, and those on 10-year bonds are not far above where they sat in late 2017. Fed funds futures are now pricing in a full rate cut by year-end, and more than two by the end of 2020.

Meanwhile, the stock market’s on a tear. The S&P 500 rose 0.9% for a third straight day of gains, bringing the benchmark roughly 2.5% from its all-time highs. Equities have now fully priced in the direct cost of higher tariffs, according to Bloomberg Intelligence. And with investors in wait-and-see mode ahead of next month’s G-20 meeting, that puts the focus back on the Fed and economic data.

For Canaccord Genuity chief market strategist Tony Dwyer, a lower effective Fed funds rate is a crux in the case for equity bulls like himself. He sees the S&P 500 ending the year at 2,950, in line with the median strategist forecast. For 2020, he’s forecasting a jump higher to 3,350 by the end of the year.

“We continue to expect a rate cut, sooner than most expect,” he wrote in a note this week. “This is the whole bull story -– slowing growth that remains positive, lower inflation, and a Fed reversal of last year’s hike.”

That’s why at this point, some traders are interpreting “bad news” as “good news.” It’s largely understood that U.S.-China trade uncertainties won’t force the Fed’s hand alone, but a subtle turn in economic strength could. And not only could it activate the Fed put, it too could bring urgency to the tariff negotiation table.

Weak economic data Wednesday was met with equity-market gains, not the typical vanilla reaction one might expect. Yes, a delay in auto tariffs on the EU and Japan helped, but continually soft numbers could encourage the Fed to backpedal.

“The way the Fed operates, they’re not going to cut rates merely because they’re concerned about the trajectory of the trade outlook coupled with weakness in the equity market,” said Tony Roth, chief investment officer at Wilmington Trust, which manages $93 billion. “They’re going to cut rates because they’re going to be more responsive to the bond market if they see credit spreads really start to widen out, and they’re going to be obviously most responsive to poor economic data.”

To that, a question: Can stock market resiliency remain if a rate cut falls out of the range of plausibility? While Fed Funds futures markets are emphatically pricing in easier policy, the central bank itself has taken a far more conservative tone, preaching patience, data-dependence, and a time for pause.

And not all are convinced a Fed rate cut is certain. Rather, Goldman Sachs Asset Management International believes the bond market has rallied too far, too fast. Yields on the U.S. 10-year should end 2019 closer to 2.7%, according to James Ashley, the firm’s head of international market strategy. Growth may be moderating, but it’s still positive.

“The markets are factoring in too much of the potential for a cut,” said Nathan Thooft, Manulife Asset Management’s head of global asset allocation. “If the market quickly priced that back out, that could cause some issues for equities. No doubt about it.”

--With assistance from Vildana Hajric.

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.