Bond Traders Take Stock After Rebound in U.S. Yields Stalls Out

Reports on actual and expected inflation, both at the heart of Federal Reserve policy making now, are also on traders’ radar.

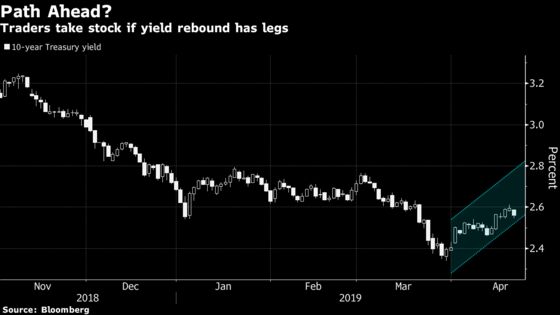

(Bloomberg) -- Bond bears have been ascendant for most of April, and now they’re looking to a key batch of data to determine whether 10-year Treasury yields’ rebound from a 15-month low has legs.

While the angst over a Chinese slowdown that drove last month’s bond rally has eased, questions linger about the global outlook as malaise in Europe persists. This week brings an update on the world’s biggest economy, with a read on first-quarter U.S. growth that’s expected to be less dire than originally predicted, though far short of a blockbuster. Reports on actual and expected inflation, both at the heart of Federal Reserve policy making now, are also on traders’ radar.

The benchmark 10-year yield touched 2.61 percent last week, the highest since the Fed surprised traders in March by shifting to a more dovish stance. It settled at 2.56 percent, up from 2.34 percent on March 28, the lowest since December 2017. Traders are now pricing in a bit more than half of a quarter-point rate reduction this year, whereas a few weeks ago they were ready for more than a full cut.

“We at this point in time don’t have a high level of conviction on the direction of interest rates,” said Margaret Steinbach, a fixed-income investment specialist at Capital Group, which runs American Funds, with $1.6 trillion under management. “But given what we know in terms of economic data still being pretty strong in the U.S., it seems the fall in yields was too extreme.”

Short-term rates are anchored given Fed officials’ message that they’ll likely stand pat this year, while any signs of rebounding growth should push up long-dated yields, Steinbach said in explaining her “high level of conviction that the yield curve will steepen.”

The gap between 3-month and 10-year rates dipped below zero last month for the first time since 2007, before widening back to 14 basis points. Inversions of this part of the yield curve are seen as a potential harbinger of recession, which underscores traders’ focus on this week’s growth figures.

While first-quarter gross domestic product is forecast to slow to a 2 percent annual pace, from 2.2 percent the prior period, it’s hardly flashing a recession signal. At the end of March, economists had predicted output last quarter would stall to 1.5 percent.

“Key downside risks to US growth are fading from view,” Goldman Sachs Group Inc. analysts wrote in a report released Thursday. “We’ve also turned more optimistic over the medium-term,” expecting expansion of greater than 2 percent through 2021.

Technical indicators also suggest odds are greater for yields to rise, said Marty Mitchell, an independent strategist. The 10-year yield’s dive to 2.34 percent was an “extreme,” as confirmed by the 10-day moving average moving above the 30-day, he said.

What to Watch

- The Fedspeak calendar goes dark this week in advance of policy makers’ May 1 decision. Most European markets are closed Monday following Easter.

- For U.S. economic releases:

- April 22: Chicago Fed activity; existing home sales

- April 23: FHFA house price index; Richmond Fed manufacturing; new home sales

- April 24: MBA mortgage applications

- April 25: Durable goods; initial jobless claims; capital goods shipments/orders; Bloomberg consumer comfort; Kansas City Fed manufacturing

- April 26: 1Q GDP, personal consumption and core PCE; University of Michigan sentiment, current conditions and inflation expectations

- Here’s the schedule for Treasury auctions:

- April 22: $42 billion of 3-month bills; $36 billion of 6-month bills

- April 23: $26 billion of 52-week bills; $40 billion of 2-year notes

- April 24: $20 billion of 2-year floating-rate notes; $41 billion of 5-year notes

- April 25: $32 billion of 7-year notes; 4- and 8-week bills

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Vivien Lou Chen

©2019 Bloomberg L.P.