Bond Traders Prefer to Pick Up the Phone for Portfolio Deals

Bond Traders Prefer to Pick Up the Phone for Portfolio Deals

(Bloomberg) -- The corporate bond market has been steadily going electronic for years, but traders in one of the fastest-growing parts are bucking the trend.

Most money managers say they still prefer to negotiate portfolio trades, where they can buy or sell hundreds of bonds in one go, through phone calls and instant messages with dealers rather than through electronic platforms. Barely a concept three years ago, portfolio trades nearly doubled from December to March, and now account for around 3% of corporate debt trading volume, according to an informal poll of dealers.

Investors like being able to discuss which securities will be in the basket of bonds that they trade, conversations that can take weeks. And dealers like being able to buy or sell large numbers of securities in one fell swoop, which reduces the chances they will lose money from a single bad note, according to money managers. Their preferences underscore how human traders are still useful even as markets grow increasingly electronic.

“The electronic vendors are basically a toll road you pay to connect with dealers” that become unnecessary if a firm has the adequate analytic tools to support their portfolio trading deals on their own, said Ray Uy, head of fixed income trading at Invesco. “There isn’t a huge advantage to go through that route if you have other means of connecting with dealers directly.”

Electronic venues like MarketAxess Holdings Inc. and Tradeweb Markets Inc. have yet to capture more than 10% to 15% of the market. Portfolio trading makes up a low single-digit percentage of total credit trading volumes that have averaged around $45 billion in the first half of 2020, according to the Securities Industry and Financial Markets Association.

There’s no clear way to discern what constitutes a portfolio trade, but market watchers generally look through trades recorded on reporting system Trace for at least 15 individual bonds that transacted at the exact same time, and are also of a large enough size to rule out retail trades, among other criteria.

“The electronic-trading platforms have an extraordinarily powerful incentive to develop a solution for this, it’s a growing source of credit market liquidity at scale,” said Ken Monahan, a senior analyst covering market structure and technology at Greenwich Associates. “The platforms so far have gotten some traction but there is still a long way to go.”

Platforms Invest

Tradeweb has done more than $100 billion worth of portfolio trades globally since launching that business in January 2019, with more than $60 billion of that coming this year, the company said earlier this month.

“We’re definitely investing heavily in portfolio trading. It’s really bringing new innovations that didn’t exist,” said Chris Bruner, head of U.S. credit at Tradeweb. “We get that clients will choose us for certain things and not for others, but we want to invest in each protocol that’s dominant in credit.”

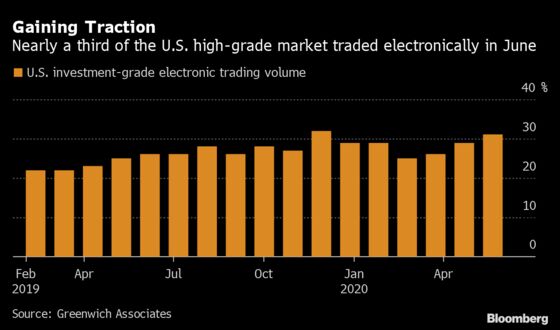

Meanwhile, MarketAxess said it transacted more than $1 billion in portfolio trades in the first quarter. Traders of investment-grade corporate bonds now use electronic networks for about a third of their transactions, up from a quarter at the start of last year, according to Greenwich.

High-yield electronic trading volumes have nearly doubled to 21% in the same period, the data show. In 2017, only about 20% of all bonds traded electronically.

But for bigger portfolio trades, so far investors find it easier to transact by voice, said Matt Berger, global head of fixed income and commodities at Jane Street, a market-making and trading firm.

“There’s a lot to be gained from that negotiation,” Berger said. “If someone wants to trade an ETF, it’s pretty straightforward. But in a portfolio, it’s not necessarily obvious what should be in it, and how to minimize the cost while still getting you the exposure you want.”

Bloomberg LP, the parent company of Bloomberg News, competes with companies including Tradeweb and MarketAxess in providing fixed-income trading services.

‘Human Component’

Of the more than 160 participants who engaged in a Goldman Sachs Group Inc. market structure survey this month, 46% said they don’t plan to execute portfolio trades on a third-party platform since there’s no need.

Tradeweb and MarketAxess acknowledge that clients may prefer to transact elsewhere, but also see a big opportunity to grow their business. Dealers echo the sentiment, and added that there are benefits to executing portfolio trades off the platforms.

In years to come as more investors become familiar and comfortable with portfolio trading, the convenience of electronic trading might push more of the business toward exchanges. For now, though, it’s still a fragmented market.

“There’s often a human component,” said Maryanne Richter, head of credit electronic trading strategy at Morgan Stanley. “You need a quarterback to pull it all together.”

©2020 Bloomberg L.P.