Bond Rout That Kicked Off 2022 Lights Fuse for Europe Volatility

It’s going to be an action-packed year for bond markets if the first week of 2022 is any guide.

(Bloomberg) -- It’s going to be an action-packed year for bond markets if the first week of 2022 is any guide.

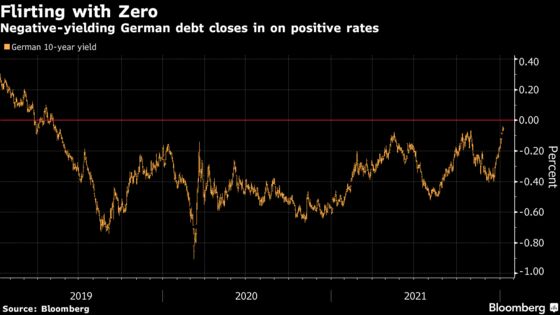

Treasuries had their worst-ever start and German debt followed to send yields to the highest since 2019. Now they are threatening to break above 0% as traders bet European Central Bank policy makers will have to act to rein in inflation that has accelerated to record levels.

The overall theme is one many foresaw coming in 2022: of markets repricing as inflationary pressures force the hand of central bankers. As bond issuance gets going this month and the policy speeches roll in, that’s likely to lead to more volatility and divergence between rates.

“The first week of this new year has surely not disappointed investors looking to trade central bank news,” said Gaetan Peroux, a strategist at UBS Global Wealth Management. “With every communication and decision it appears increasingly clear that most G-10 central banks’ normalization schedules are becoming more advanced.”

| Read More: |

|---|

|

The Federal Reserve is leading the way, with market expectations for at least three rate hikes and a reduction in the bond assets on its balance sheet. While the ECB’s debt buying continues, its total quantitative easing this year is expected to fall to just over 500 billion euros ($570 billion), almost half the level seen in 2021, according to TD Securities.

That will turn net euro-area bond supply positive this year, once redemptions and QE are taken into account, at 75 billion euros, compared with a shortage of 392 billion euros last year, according to Danske Bank A/S.

Shorting Bunds

“Increased duration supply is likely to support the bearish move in rates,” said Pooja Kumra, a senior European rates strategist at TD Securities. She is targeting German 10-year yields -- the only such tenor below zero in the euro area -- to turn positive and reach 0.30% at year-end. The median in a Bloomberg survey is for about 0.1%, with investors historically wary of getting burned by shorting bunds.

Sub-zero rates have been a common feature in the region for years, and the prospect of the ECB tightening policy is slowly reversing that. The pool of regional debt with yields below zero nearly halved from its pandemic-era peak to 4.5 trillion euros this week.

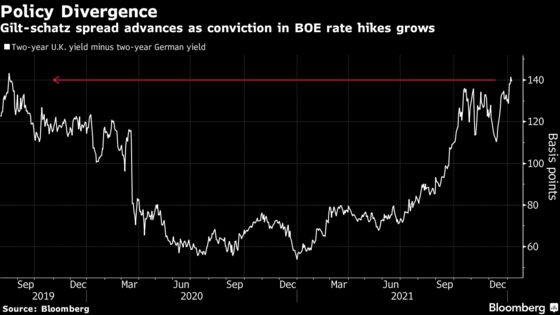

The selloff in German bonds has been outpaced by the U.K. That’s driven the spread between two-year U.K. yields and equivalent German rates to over 140 basis points for the first time since 2019.

The widening rates differential reflects investors’ belief the Bank of England will outdo the ECB when it comes to tightening. Money markets are now pricing in around 100 basis points of U.K. rate hikes by the end of this year, compared with less than 15 basis points by the ECB.

Investors will increasingly be looking for these relative rates trades as central bank action varies around the world.

“Rate hikes don’t mean sellers of rates volatility will lose this year, given the current elevated levels,” said Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence. “The potential for higher equity volatility this year has also boosted the cost of hedging in the options market given investor demand for protection.”

The U.K.’s higher yields may also be drawing some investors to its currency. While foreign-exchange trading hasn’t been as volatile as bonds so far, sterling has been an outperformer. The pound is the only Group-of-10 currency to have gained against the U.S. dollar in 2022.

At nearly $1.36, it’s already outstripped median forecasts for gains this quarter, with a Bloomberg survey seeing it reaching $1.37 by year-end. Some strategists think its rally is unsustainable, with Morgan Stanley describing the performance as “surprisingly resilient.”

It “could have been driven by a bear-steepening of the U.K 2s10s curve and an increase in expectations for Bank of England policy rate increases,” Morgan Stanley strategists said in a note.

Next Week

- European sovereign bond sales are set to pick up next week. Commerzbank AG sees upside risk to its total euro sovereign supply projection of about 30 billion euros

- Sales are expected from the Netherlands, Austria, Germany and Italy. Ireland, Portugal, Belgium and Spain could also come to the market, while the U.K. is set for its first bond sale of the year on Tuesday

- The data calendar in the euro area is thin with a focus on labor market figures on Monday

©2022 Bloomberg L.P.