Dreams of Higher Treasury Yields Fade as Fed Fuels Flatter Curve

Treasuries have further to rally in the wake of Fed meet and plunging stock markets are signaling a greater chance of recession.

(Bloomberg) -- Talk of a 10-year Treasury yield heading toward 4 percent or higher is starting to seem like a distant memory.

The Federal Reserve on Wednesday opted to implement its fourth interest-rate hike this year and said it still expects to tighten policy in 2019, albeit at a slower pace. U.S. stocks have taken a hit, pushing investors into havens such as longer-dated Treasuries, with the benchmark 10-year yield falling below 2.75 percent for the first time since April.

“We’ve seen the peak of Treasury yields,” said Tano Pelosi, a portfolio manager at Antares Capital. “The carry trades that were popular in the last few years, I think there are clear open questions now on whether they can continue.”

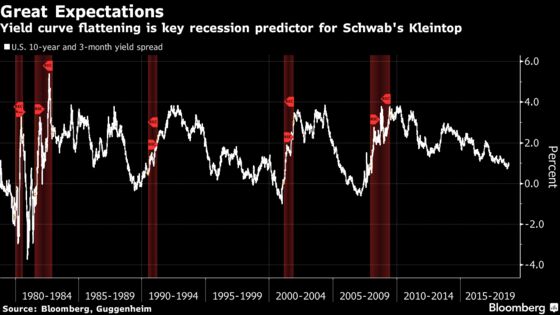

The worry among investors is that the more the Fed hikes, the closer it takes the U.S. economy toward a recession. That’s manifesting itself in a yield curve close to its flattest levels since before the global financial crisis.

“As the curve keeps flattening on us, it’s telling us that monetary policy is being too restrictive and that we don’t have enough reserves in the system to stimulate the economy,” said Scott Minerd, chief investment officer at Guggenheim Partners.

Wall Street forecasters had anticipated that Fed officials would lower their median rate projection for 2019, which they did, although the central bank did indicate continued confidence in the economic outlook. Investors’ faith in the Fed’s tightening path has crumbled in recent weeks amid tumbling stocks and doubts about global growth.

“The stock market is recognizing the heightened risk of recession,” said Jeffrey Kleintop, a strategist at Charles Schwab & Co. “It’s the Fed that really holds the key to the overall market and economic direction in 2019.”

Here’s what others are saying:

BlackRock (Not responsive enough)

What markets are showing us “is really concern. Concern that the Fed is not being responsive enough in terms of the financial conditions tightening,” said Jeffrey Rosenberg, BlackRock’s chief fixed-income strategist.

“They are disappointed and they’re worried that the Fed missed the opportunity to halt the negative risk tone across all markets.

“There’s a strong desire by the Fed, as Powell reiterated here, to not let the balance sheet became an active tool of monetary policy. And there’s a good reason for that, because they don’t know how to calibrate that tool.”

Bank of Singapore (Steady yields)

“The reduction in dots was in the right direction,” said Rajeev De Mello, chief investment officer. “But they could have been a bit more sympathetic to some of the signals in the market. I expect Treasury yields to be where they are now -- for me, that’s fairly positive for a few assets, notably higher-yielding emerging market bonds such as Indonesia’s and also higher-yielding Asian credit.”

“Credit spreads have widened out, and if yields on U.S. Treasuries stay stable, that should make for interesting opportunities.”

Well Fargo (EM currencies to struggle)

Strategist Brendan McKenna favors the Mexican peso and the Brazilian real. And expects emerging-market currencies to struggle in a scenario of two Fed hikes next year due to slowing global economic growth, an environment typically not favoring emerging-market currencies.

Perpetual (Wider outcomes)

“We’ve de-risked and positioned our portfolio for tightening liquidity as central banks unwind their balance sheets and interest rates go up,” said Vivek Prabhu, head of fixed income. “I think a lot of the volatility we’ve seen in markets is partly due to the liquidity withdrawal that’s seen with the Fed and other central banks like the ECB. Whilst the Fed’s base case may still have a lot of validity, I think the range of economic outcomes in 2019 will be a lot wider.”

Prabhu’s fund has doubled holdings of top-rated Australian corporate bonds and increased allocation to securitized assets.

More Fed Coverage

Fed Raises Rates, Trims Forecast for Hikes in 2019 to Two

Powell Enters Era of Rate-Hike Caution as Growth Headwinds Mount

The Fed’s Not Ready to Retire Forward Guidance: Daniel Moss

Fed Sees Hikes Boosting Unemployment in Time for 2020 Election

More Than One Reason Traders May Have Disliked the Fed’s Message

That’s Seven Strikes for Powell Since He Took Over

Prospect of Fed Cut in 2020 Firms, in Traders’ Eyes at Least

--With assistance from Michael G. Wilson, Aline Oyamada, Cormac Mullen, John Ainger, Benjamin Purvis and Mark Tannenbaum.

To contact the reporters on this story: Adam Haigh in Sydney at ahaigh1@bloomberg.net;Ruth Carson in Singapore at rliew6@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Keith Jenkins, Ven Ram

©2018 Bloomberg L.P.