Bond Rally Gone Too Far But Trade War Risk Keeps Schroders Long

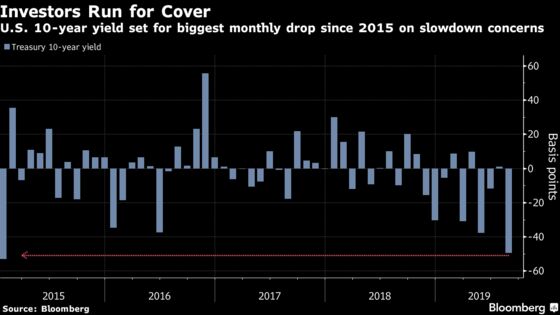

Intensifying fears of a synchronized global slowdown has sent investors piling into the safety of government bonds.

(Bloomberg) -- The global debt rally is no longer justified by economic fundamentals but escalating trade war risks are keeping the managers of one of Australia’s top-performing bond funds from exiting long positions.

Bonds are pricing in a recession which is not likely in the near term, according to Simon Doyle, head of fixed income and multi-asset at Schroder Investment Management Australia Ltd., and Stuart Dear, deputy head of fixed income. While they have turned more defensive, the fund managers still favor long-duration exposure in the U.S., Australia and to a lesser extent Europe.

“In some ways you can argue yields have probably gotten a little bit ahead of fundamentals and it’s being driven by sentiment,” Doyle said in an interview in Sydney. “But we are still on the long side at the moment until we see something change on the trade side.”

The pair’s A$2.5 billion ($1.7 billion) Schroder Fixed Income Fund/Australia has beaten 97% of its peers over the last year.

Intensifying fears of a synchronized global slowdown amid the worsening U.S.-China trade dispute has sent investors piling into the safety of government bonds in recent months. In August, U.S. Treasuries saw their strongest rally since the height of the 2008 financial crisis as 10-year yields tumbled below 1.5%. Bond yields also slid to record lows in Europe and Australia.

Zero Rates

Schroders hasn’t ruled out the possibility that rates could move “significantly lower,” Doyle said. Still, for U.S. yields to hit zero, it would probably require a recession, something that is only likely on a one-to-three year view, he added.

“Zero is not out of the realms of possibility, but there are a few things that need to happen for that to occur,” he said. “It’s not a given that this all kind of flows into recession, so we are keeping an open mind. We are playing it from the long side, from the long duration side.”

Schroders has trimmed some of its holdings slightly into the bond rally, and one of the reason that it remains long duration is because risk assets were fully priced, according to Doyle.

“If you work your way through markets there’s not really a lot of risk premium being embedded in asset markets anywhere,” he said. As yields head lower, “it gets harder and harder. You are not going to see those returns repeated,” he said.

Long Sterling

The fund manager sees corporate bonds from transport companies and REITs as attractive, as well as infrastructure securities and inflation-linked notes. In currencies, it favors being long yen and short the Australian dollar, and has a small long position in sterling.

“We think it’s discounted pretty bad scenarios and notwithstanding the machinations of the U.K. parliament, it hasn’t really moved that much,” Doyle said. “It is so cheap that if you do get even a semi-positive resolution to Brexit that it does have quite a lot of upside.”

--With assistance from Nancy Moran.

To contact the reporter on this story: Andreea Papuc in Sydney at apapuc1@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen, Joanna Ossinger

©2019 Bloomberg L.P.