Bond-Market Tourists Threaten to Bolt With $200 Billion at Risk

Bond-Market Tourists Threaten to Bolt With $200 Billion at Risk

(Bloomberg) -- In March, investors that usually buy riskier assets ended up snatching up U.S. blue-chip company debt, taking advantage of bargain-basement prices. Now that the easy money has been made, they’re likely looking to sell.

The investors, informally known as tourists, may end up unloading as much as $200 billion of high-grade securities over the rest of this year, according to a Bank of America Corp. estimate. The selling pressure could be one of the few headwinds the debt faces in the coming months, said Hans Mikkelsen, the bank’s head of U.S. investment-grade corporate bond strategy.

“Clearly by the end of the year, they’re going to leave,” Mikkelsen said, referring to the investors that dipped their toes in high-grade notes opportunistically.

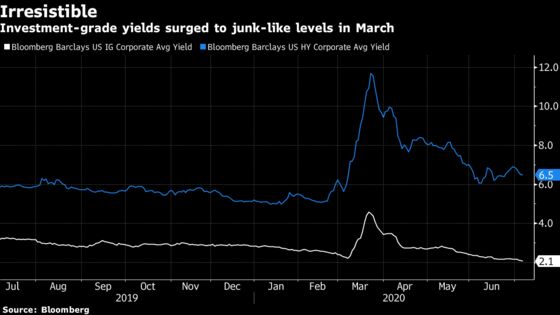

For many tourist money managers, including distressed debt managers and equity hedge funds, the temptation to buy was irresistible. In mid-to-late March, investment-grade corporate bond yields averaged as much as 4.58%, not far from where junk-bond yields had been just a few months earlier. Risk premiums for the notes, or spreads over Treasuries, surged to more than 3.7 percentage points, levels not seen in a decade.

A passel of investors jumped in. Angelo Gordon & Co. bought $500 million of mostly investment-grade debt in the U.S. and Europe the week beginning March 23, when the Federal Reserve said it was stepping in to support the market. JPMorgan Chase & Co. noticed generally that distressed debt funds were placing orders for new high-grade deals around the same time. Quant hedge fund Two Sigma Investments bought more than 1 million shares of BlackRock’s investment grade corporate bond ETF during the first quarter, according to its most recent 13-F filing, a holding that would have been worth about $150 million on March 31.

The market may well be able to absorb any selling from profit takers. The Federal Reserve is providing extraordinary support to credit markets, and foreign investors have been taking advantage of low hedging costs and snapping up U.S. corproate debt. So there are still motivated buyers for the notes, said UBS Group AG credit strategist Stephen Caprio.

About $24 billion of publicly traded investment-grade corporate bonds have been changing hands per day this year, according to the Securities Industry and Financial Markets Association, a trade group. So $200 billion of selling over six months probably won’t create a huge ripple in valuations.

Opportunistic investors “were taking advantage of investment-grade spreads that were approaching Great Financial Crisis levels,” Caprio said. “Now they’re handing off the baton to insurance companies and foreign buyers.”

Those who timed their high-grade-bond buying well have enjoyed a spectacular return for a relatively safe asset. Between March 23 and Tuesday night, the notes gained more than 17.8% on average, accounting for both interest and price gains. In the three months ended June 30, the securities recorded their best quarter in 11 years.

While the Covid-19 pandemic is weighing on earnings, most investment-grade-rated companies have room to suffer from weaker results and still pay their obligations. In 2019, the average high-grade corporate borrower had earnings before interest, tax, depreciation and amortization, a measure of the income available to pay debt obligations, equal to about 9.6 times their annual interest expense, according to Moody’s Investors Service.

READ MORE: Foreign Money Stampedes Back to U.S. Corporates, Seeking Yield

The window to buy high-grade bonds at such attractive levels has probably closed: the securities yielded just a bit above 2% as of late Tuesday, and risk premiums had shrunk to 1.4 percentage point. Now it’s a matter of when the tourist money will leave, said David Norris, head of U.S. credit at TwentyFour Asset Management.

“I think some of these investors have been taking profits and are looking to rotate into better opportunities now that spreads are tighter,” Norris said.

©2020 Bloomberg L.P.