Bond Market’s Rout Makes Forecasting Fun Again

(Bloomberg Opinion) -- Interest-rate forecasting rarely rewards the bold. Yes, a bond bull like Steven Major at HSBC Holdings Plc will occasionally be vindicated, like when he went firmly against the consensus in 2014 to predict that Treasury yields would tumble. But from 2015 to 2017, you’d have been better off guessing no change at all: the 10-year U.S. benchmark moved a minuscule 10, 17 and 4 basis points in those years.

Of course, 2018 is on track to shake the world’s biggest bond market out of its rut. The 10-year Treasury yield is up 75 basis points since the start of the year, on pace for the third-largest jump since the turn of the century. Almost half of that is due to a recent sell-off, which pushed yields to multiyear highs and helped spark a sharp decline in global stock markets last week.

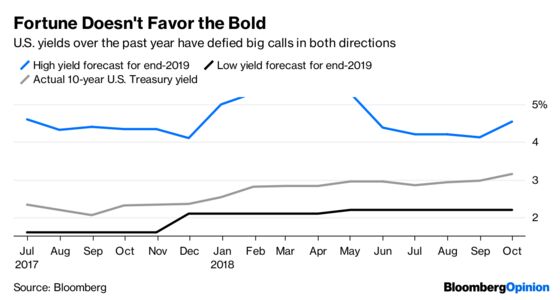

This latest bout of volatility is re-energizing analysts, who had for months been gravitating closer to prevailing market levels, according to survey data compiled by Bloomberg. But in the latest monthly update, on Oct. 11, the high-yield forecast for year-end 2019 jumped to 4.55 percent from 4.12 percent, widening the dispersion of the survey to 2.35 percentage points. That’s the biggest difference of opinion since May — the last time the Treasury market broke through key levels. The median estimate is about the highest it has ever been in the surveys, at 3.49 percent.

Now, you won’t find many who agree with John Dunham at Guerrilla Economics, who made that 4.55 percent call — though JPMorgan Chase & Co.’s Jamie Dimon has said 10-year yields rising to 5 percent is “a higher probability than most people think.” Still, his big upward revision (from 3.88 percent in September) exemplifies the type of bombastic calls that bond traders have come to expect around big swings in the Treasury market.

That goes both ways. Just this week, Barclays Plc inspired a popular Bloomberg News article titled “Treasury 10-Year Yield Above 3% May Not Be Long for This World.” The bank’s rates strategist, Rajiv Setia, recommended buying 10-year Treasuries, targeting a 2.95 percent yield. Strategists at Citigroup Inc., JPMorgan, Nomura Holdings Inc. and UBS Group AG also saw the sell-off as a buying opportunity, albeit to varying degrees.

Calling a bottom is hardly surprising after the losses reversed last week. But if this Federal Reserve tightening cycle has taught us anything, it’s that these sort of prognostications haven’t panned out. From April: “Citigroup Says Buy 3% 10-Year Treasuries, Target Rally to 2.65%.” They never reached that level. In March: “Have Yields Peaked for 2018? BMO Thinks So With 10-Year at 2.8%.” They made multiple new highs after that. I remember those predictions because I wrote about them. I’m sure there are more.

And yet strategists continue to make bold calls, and investors gobble them up. Perhaps not necessarily because they’ll be right, but because they’re fun. And, in fairness to Barclays, they’re backed up by reasonable analysis.

Setia said long-term real rates had risen to levels that are “not consistent with underlying activity over the medium to long term.” To him, the prospects for U.S. growth remain strong, but that’s largely because of fiscal stimulus and “should have little bearing on long-term structural factors, such as worsening demographics and subdued productivity growth.”

It’s hard to truly argue against any of that, especially on the heels of the International Monetary Fund downgrading its estimate of global growth for the first time since July 2016. It now expects an expansion of 3.7 percent this year and next, down from 3.9 percent just three months ago.

On the other hand, Setia says “a reversal could be fairly quick” because speculative traders are betting heavily against Treasuries, meaning they could be forced out of their positions if the market turns. Sound familiar? As I wrote in August, everyone likes the idea of a short squeeze, but it just hasn’t happened this year. To predict otherwise, and to have it inform your trade suggestion, ignores recent history.

The best strategy might just be to take a cue from the Fed and expect gradual but consistent increases to interest rates, including long-term Treasury yields. It might not be that fun, but until something truly changes, you’d probably be better off just sticking to the averages.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.