Bond Funds Learn to Exploit Ratings System to Buy Riskier Debt

Bond Funds Learn to Exploit Ratings System to Buy Riskier Debt

(Bloomberg) -- In today’s low interest-rate world, investment-grade bond funds face an all-too-familiar trade-off: buy risky debt to improve returns or play it safe and underperform.

But some of them, it seems, have managed to have it both ways.

In particular, funds are loading up on bonds where ratings firms are split on whether they’re investment grade or junk. While reasonable people can disagree about which one is right, for a growing number of firms, the answer is always the same: the higher one.

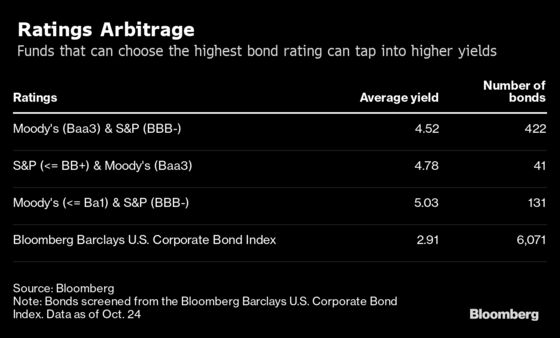

The practice has obvious advantages. With high-grade corporate bonds yielding less than 3% on average, managers can pick up an extra half-percentage point on split-rated debt. And funds can say they’re invested in safe assets while running a portfolio that actually looks a lot like a junk bond fund.

The downside for their clients, however, is it may obscure just how much credit risk they’re exposing themselves to.

“You don’t want the manager to just cherry pick grades,” said Thornburg Investment Management’s Lon Erickson. “You need to trust that they’re doing their due diligence and not just going out and fishing for yield.”

Granted, managers have always had the discretion and the flexibility to choose which ratings standards to follow. The methodology is there for all to read in the fund’s prospectus, though it’s often tucked into the fine print. Then, there’s the question of how much stock to put into ratings anyway. Many managers lean on their own analysis to determine a bond’s credit risk.

The potential for trouble, however, is clear. Of particular concern is whether managers are moving into investments that could be tough to sell if investors rush for the exits all at once. And in extreme cases like H20 Asset Management and GAM Holdings, consequences can be damaging. Definitive numbers are hard to come by. But as ultra-low rates have seemingly become a permanent fixture, it’s easy to see why bond funds play the split-ratings game.

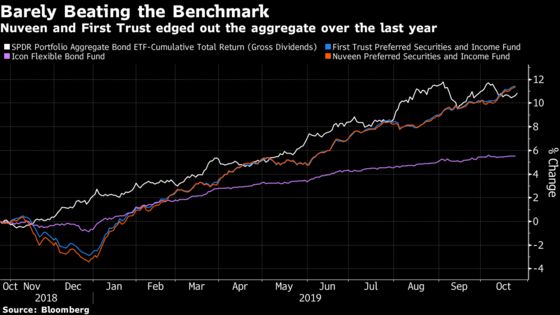

Three in particular stand out: the Nuveen Preferred Securities and Income Fund, First Trust Preferred Securities and Income Fund and the ICON Flexible Bond Fund. According to a Bloomberg analysis, the credit quality of each of the funds fell into junk territory when using a methodology that either averages the ratings or took the lower of the two instead.

The Nuveen fund is the largest of the three with $4 billion in assets. In its latest annual report for the year through September 2018, 58% of the fund’s holdings were rated BBB — the lowest high-grade tier — or higher. Yet based on Bloomberg’s composite ratings methodology, the weighted-average credit quality was BB+, the highest level of junk. It was still BB+ as of last month.

In all, about 12% of the Nuveen fund was in split-rated bonds where S&P Global Ratings and Moody’s Investors Service disagreed on whether they are investment grade or junk. That compares with 3.7% of bonds in a widely followed benchmark index for investment-grade debt. The fund considered all the bonds investment grade, while Bloomberg’s standard rated them junk.

“Our goal is to provide investors with the most relevant data to make informed decisions in alignment with their financial goals and risk tolerance,” the firm said in an emailed statement in response to questions from Bloomberg.

The weighted-average credit quality of First Trust’s $279 million fund was also below investment grade, based on Bloomberg composite ratings. And its holdings yielded 5.17% on average versus 2.91% for U.S. corporate bonds, data compiled by Bloomberg show.

“If split-rated bonds correspond to the yield of the lower rating, that gets to the incentive for managers to hold them,” said Craig McCann, a principal at Securities Litigation & Consulting Group.

In a statement, First Trust said its decision to use the highest available rating was due to the intricacies of the preferred and hybrid debt market, and called the approach the “industry standard.” The firm added that “ratings from agencies are only one input into a much larger internal credit review.”

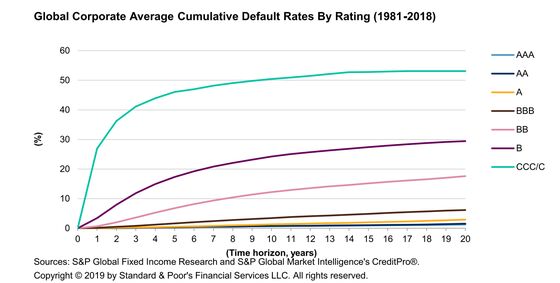

That extra yield comes with a price. Historical data from S&P shows that lower initial ratings correspond with higher rates of default. The gap is notably stark in the divide between investment grade and junk. Ten-year default rates on bonds with BB ratings are double those with BBB grades.

Often times, bonds that become split rated because of a downgrade aren’t split rated for long, according to Smith Asset Management’s Frank Smith. That means investors in a traditionally safe, investment-grade fund with a disproportionate number of the securities could wind up being exposed to many more junk bonds than they intended. If either S&P or Moody’s cut their ratings, “the odds are the other will soon downgrade” as well, he said.

It’s not clear whether the added risk is really worth it. While two of the three funds eked out slightly above-average returns in the past year, only one had a risk-reward profile that is better than a vanilla fund tracking investment-grade corporate bonds, data compiled by Bloomberg show. (The higher the Sharpe ratio, the more investors are being compensated for the risk their funds take.)

Jerry Paul, who runs the $154 million ICON Flexible Bond Fund, says he speaks candidly to his clients about his approach and added that he’s targeted split-rated bonds for decades to help give his fund an edge.

“We have limits on how much junk we can own, so the provision helps me with clearing that hurdle,” Paul said. “I had this in my prospectus back in the 1980s and it was really unusual back then. Now, everyone seems to have this provision that allows you to rely on the highest rating available.’’

“We're looking to take advantage of the inefficiency” to buy split-rated bonds that will eventually get upgraded to full investment-grade status, he said. The ICON fund, which has outperformed its benchmark over the longer-term periods, held split-rated bonds including those issued by Micron Technology Inc., Standard Industries Inc. and MPT Operating Partnership LP.

Thornburg’s Erickson says there’s still the risk some fund managers might not be as transparent.

“It’s one of those things, that’s not quite a technicality, and investors want to understand how the statements made in a prospectus are impacting the portfolio,” said Thornburg’s Erickson. “There’s certainly room to play games if they don’t clearly state how they handle split-rated issues.”

Bloomberg screened for U.S. bond funds with over $100 million in assets that aimed to invest primarily in investment-grade securities, based on their prospectuses. Of the more than 1,000 funds that met the criteria, Bloomberg identified over 120 funds that were considered non-investment grade based on their actual portfolio holdings. The holdings-based standard considers funds to be non-investment grade when less than 70% of assets have investment-grade ratings using Bloomberg composite ratings.(For any given bond, the Bloomberg composite system averages the grades from the four major credit ratings firms, Moody’s, S&P, Fitch and DBRS. When a bond has two ratings, the methodology takes the lower one if they differ. Bonds with only one rating are deemed unrated. Bloomberg excluded funds when less than 90% of their holdings had composite ratings.)Bloomberg then looked for funds with the greatest disparity between their stated investment-grade mandate and the credit quality of their holdings. Three funds listed in the article had weighted-average credit ratings that were below investment grade, based on the composite rating system.

To contact the editor responsible for this story: David Papadopoulos at papadopoulos@bloomberg.net, Michael TsangLarry Reibstein

©2019 Bloomberg L.P.