Bond Bulls Shake Off Trade Progress as Global Concerns Persist

While bond bulls absorbed a blow on Friday, they see little risk that yields are about to scream higher.

(Bloomberg) -- While bond bulls absorbed a blow on Friday, they see little risk that yields are about to scream higher.

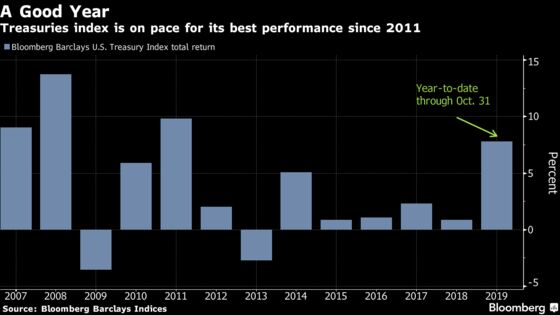

U.S. government debt is still headed for the best annual performance since 2011, and for strategists at Societe Generale and TD Securities, the bullish case is holding up fine: Growth is cooling overseas, the European Central Bank is embarking on a fresh round of quantitative easing and inflation is muted. Any climb in 10-year U.S. yields toward 2% will be capped, according to SocGen’s Subadra Rajappa.

“It’s definitely a positive, both jobs and better outcomes on trade, but I still struggle to see a sustained rise in yields,” said Rajappa, SocGen’s head of U.S. rates strategy. “The broader macro concerns still exist: slower global growth, ECB QE and lower inflation.”

Rates on 10-year Treasuries rose about 2 basis points on Friday to 1.71%, but were still 8 basis points lower on the week. Traders have pushed wagers on Fed easing deeper into 2020, with a full quarter-point cut not priced in until after mid-year.

For TD’s Gennadiy Goldberg, Friday did little to derail his expectation for a gradual grind lower in yields. He sees scant evidence of an improvement in growth overseas and is still waiting for a material breakthrough on trade, so he predicts 10-year yields will head toward 1.5% by year-end.

“We’re still looking for any signs of real progress” on trade, even after China and the U.S. signaled they’re getting closer to agreeing on the first phase of a deal, said the senior rates strategist. “We’ve been hearing about ‘agreement in principle’ for the past 12 months, but have only seen increases in tariffs materialize.”

In the days ahead, he’ll be keeping an eye on Germany’s industrial production release for signs that the trade fallout is spreading. In the U.S., Tuesday’s Institute for Supply Management report on service industries will show whether global uncertainty is starting to impact the American consumer, he said.

SocGen’s Rajappa is of a similar mind. While Fed Vice Chairman Richard Clarida said Friday that policy makers don’t see a crack in the consumer side of the economy, the weeks ahead will provide important clues, she said.

“The U.S. economy is not firing on all cylinders, it’s very much dependent on the consumer,” Rajappa said.

What to Watch

- The latest readings on the service sector will be among the highlights of a week featuring a parade of Fed speakers.

- Here’s the economic calendar:

- Nov. 4: Durable and capital goods; factory orders

- Nov. 5: Trade balance; Markit services PMI; JOLTS job openings; ISM non-manufacturing

- Nov. 6: MBA mortgage applications; unit labor costs and nonfarm productivity

- Nov. 7: Jobless claims; Bloomberg consumer comfort; consumer credit

- Nov. 8: Wholesale trade sales and inventories; University of Michigan sentiment

- Here’s the schedule for Fed speakers:

- Nov. 4: San Francisco Fed’s Mary Daly

- Nov. 5: Richmond Fed’s Thomas Barkin; Dallas Fed’s Robert Kaplan; Minneapolis Fed’s Neel Kashkari

- Nov. 6: Chicago Fed’s Charles Evans; New York Fed’s John Williams; Philadelphia Fed’s Patrick Harker

- Nov. 7: Kaplan; Atlanta Fed’s Raphael Bostic

- Nov. 8: Daly; Governor Lael Brainard

- It’s a busy auction calendar:

- Nov. 4: $45 billion 13-week bills; $42 billion 26-week bills

- Nov. 5: $28 billion 52-week bills; $38 billion 3-year notes

- Nov. 6: $27 billion 10-year notes

- Nov. 7: 4- and 8-week bills; $19 billion 30-year bonds

--With assistance from Emily Barrett.

To contact the reporter on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum

©2019 Bloomberg L.P.