BofA Survey Signals Cyclical Boom Behind 2021 Rally Has Peaked

BofA Survey Signals Cyclical Boom Behind 2021 Rally Has Peaked

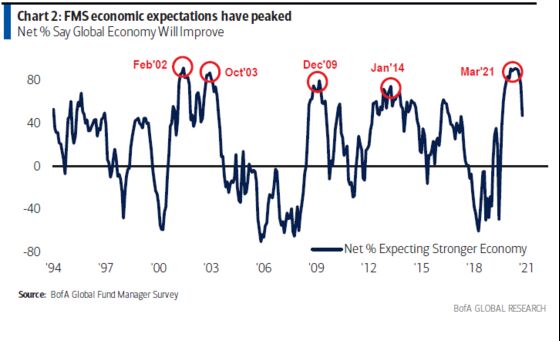

(Bloomberg) -- Global investors who have been optimistic about the economic recovery for most of this year are now scaling back their expectations, signaling that the cyclical boom behind this year’s rally is running out of steam.

This is the takeaway from the Bank of America Corp.’s monthly fund manager survey in the week through July 8. Participants with $742 billion under management slashed their outlook for global growth and corporate profits, while predictions of a steeper yield curve fell to a two-year low.

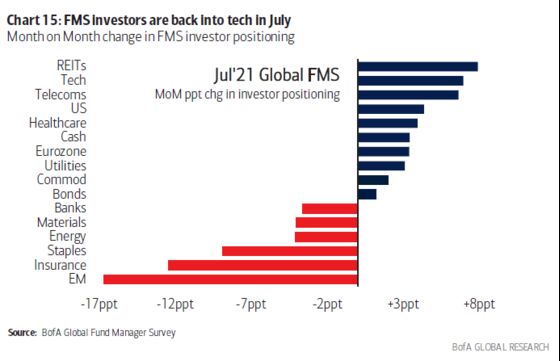

The change in preferences reflected the souring mood on the pace of economic recovery as BofA said market players trimmed their exposure to cyclical, value and small cap stocks -- some of this year’s top performers -- and shifted into technology, growth and large-caps.

Investors around the world are mulling their next steps as equities trade at record highs while concerns over the rapid spread of the delta variant and possible curbs on stimulus measures weigh on appetite for risk assets. Cyclical and cheaper stocks have been underperforming companies with higher profit growth over the past month as market participants turn more cautious.

Fund managers also pared back their expectations for a U.S. infrastructure stimulus package to $1.4 trillion in July from $1.7 trillion last month, BofA said. Among surveyed investors, 70% expect the Federal Reserve to signal tapering in August-September, while at the same time most predict the first Fed rate hike only in January 2023.

To be sure, fund manager positioning relative to history remains tilted toward cyclical assets, such as Eurozone stocks, industrials and materials, as well as commodities, according to BofA. And while the survey’s allocation to equities fell in July, it remains high at 58% overweight, and the bond allocation was a net 68% underweight. Exposure to cash rose to a net 12% overweight, the highest since October 2020.

This seemingly conflicting investor mood, according to BofA strategists led by Michael Hartnett, is best explained by the view that elevated uncertainty in economic growth and markets will mean slow tapering, while inflation is seen as a “transitory” tail risk and the delta variant as a distant threat.

Other BofA global fund manager survey highlights include:

- Allocation to U.S. stocks rose 5 percentage points to net 11% overweight, while exposure to U.K., Japanese and EM equities dropped

- Allocation to Eurozone shares increased 4 percentage points to net 45% overweight, highest since January 2018

- In terms of sector allocation, investors rotated out of utilities and staples and into technology, banks, pharma, and industrial stocks

- Inflation topped the list of tail risks, followed by taper tantrum, asset bubbles, China slowdown, and Covid-19

- Among most crowded trades, long tech topped the list, followed by long ESG, long Bitcoin, long commodities

©2021 Bloomberg L.P.