BNP Picks Up the Pieces as Europe’s Banks Sever Hedge Funds Ties

BNP Picks Up the Pieces as Europe’s Banks Sever Hedge Funds Ties

(Bloomberg) -- Bank after bank across Europe has decided it’s not worth the trouble to try to compete with Wall Street in the high-speed, high-risk world of equities trading. BNP Paribas SA begs to differ.

The French lender last week agreed to take on the hedge fund clients of Credit Suisse Group AG after the Swiss bank decided to exit the so-called prime brokerage business in the wake of $5.5 billion in losses from a single relationship. For BNP, it’s the third recent transaction to boost its equities unit and follows a similar deal with Deutsche Bank AG two years ago.

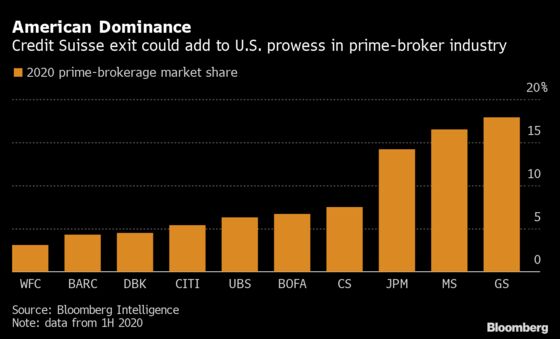

The moves make BNP one of the last European holdouts in a business dominated by U.S. banks such as Goldman Sachs Group Inc., Morgan Stanley and JPMorgan Chase & Co. They illustrate the strategy of Chief Executive Officer Jean-Laurent Bonnafe to use the financial strength of Europe’s most profitable lender over the past three years for opportunistic, bolt-on transactions, including in businesses that peers find too risky or capital-consuming.

“We want to become the European leader in global equities –- competing directly with the major U.S. players,” said Olivier Osty, the head of BNP’s trading unit. “Our asset management and hedge fund clients tell us every day that they need a strong European financing counterpart to diversify their reliance on U.S. banks.”

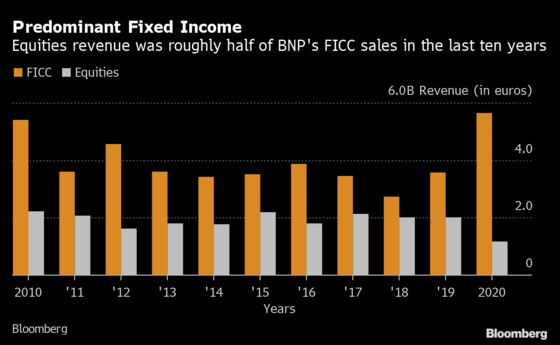

Prime brokerage units lend cash and securities to hedge funds and execute their trades. They’re typically housed in the equities units of large investment banks and contribute on average about a third of the equities revenue. The relationships with hedge funds can be lucrative, both for the trading business and for other businesses such as wealth management.

They can also carry big risks, as evidenced by the collapse of Archegos Capital Management this year, which prompted a major shakeup and soul-searching at Credit Suisse. Nomura Holdings Inc. stopped offering cash prime-brokerage services in the U.S. and Europe after also losing billions of dollars in the Archegos blowup. Deutsche Bank narrowly escaped Archegos losses after it had already decided in 2019 to exit equities trading altogether because it wasn’t competitive.

For Osty and Yann Gerardin, BNP’s chief operating officer who oversees the investment bank, the exit of rivals is an opportunity to bulk up an equities business that had long been in the shadow of the larger fixed-income unit. Two years ago, BNP’s equities trading ranked fifth among European banks, trailing firms such as UBS Group AG, Societe Generale SA and Barclays Plc. Now it’s setting its sights on becoming the top player in Europe and a major competitor for Wall Street.

“BNP is now the last European lender to resist the U.S. hegemony in the prime brokerage space,” said Jerome Legras, managing partner and head of research at Axiom Alternative Investments.

Even losses from complex equity derivatives last year didn’t deter BNP from strengthening the business, as it was quicker than SocGen and Natixis to recover from those hits. Early this year, BNP announced it was seeking to acquire the remaining 50% it didn’t already own in Exane, a firm with which it had partnered since 2004 in equities.

The Exane transaction followed on the heels of a 2019 agreement with Deutsche Bank, under which the German firm is transferring its prime brokerage assets to BNP along with 1,000 jobs. The transaction is expected to be completed by the end of this year and should bring about 400 million euros in additional annual revenue to BNP’s equities unit, Chief Financial Officer Lars Machenil said in July.

The impact from the agreement with Credit Suisse is less clear, because it only encourages its clients to move to BNP. Still, the Swiss lender had the fourth-highest market share last year among major banks in prime brokerage, according to Bloomberg Intelligence. It expects to lose $300 million in revenue this year from exiting the prime business, and $500 million to $600 million next year, indicating the potential upside for BNP.

“While BNP, like other French banks, had a strong legacy in equity derivatives, it was less interested in cash equities, which it let Exane handle, and it didn’t have any significant prime business initially,” said Matthew Clark, equity analyst at Mediobanca. “Now BNP is pushing to provide the full range of equity services.”

Even with the added revenue, the French lender has a way to go until it catches up with the Wall Street giants. So far this year, BNP’s quarterly equities revenue fluctuated roughly between $800 million and $1 billion, while JPMorgan, Goldman Sachs and Morgan Stanley never saw theirs fall below $2.5 billion.

There are other caveats. For one, Europe’s fragmented capital market makes it difficult to compete with the U.S. in a full-service equities business, said Mediobanca’s Clark.

And after nearly a decade of increasing regulations and capital requirements, investment banking deals don’t always provide quick returns on investment. Prime brokerage, though lucrative, still requires significant capital as a buffer against potential losses, as well as effective risk controls.

That, however, is where Bonnafe may have an advantage over his European rivals. Unlike Deutsche Bank, where investment banking is typically the largest revenue source despite years of cutbacks, BNP can rely on the relatively stable income from its retail and financial services operations, which contribute about two thirds to the top line.

That’s helped smooth out volatility from the trading business, even when stock traders were blindsided at the onset of the pandemic. Cumulative over the past 12 quarters, the French lender has made more profit than any other peer in Europe, according to Bloomberg calculations.

BNP “is one of the last banks in Europe that can afford to allocate capital and make deals to boost its investment bank,” said Legras at Axiom. “Still, there’s a hell of a competition” from the U.S.

©2021 Bloomberg L.P.