BlackRock Sells Dollar For Asian Currencies Into U.S. Vote

BlackRock Inc. holds a “modest” short in the greenback against the likes of the Chinese yuan, Indian rupee and Indonesia rupiah.

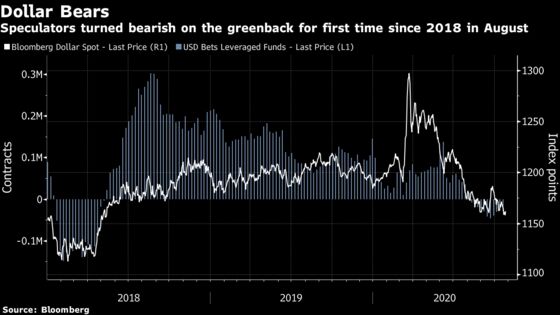

(Bloomberg) -- The world’s biggest money manager is shorting the dollar on expectations that unprecedented fiscal and monetary stimulus will prolong its losses -- regardless of who wins the U.S. election.

BlackRock Inc. holds a “modest” short in the greenback against the likes of the Chinese yuan, Indian rupee and Indonesia rupiah, said Neeraj Seth, head of Asian credit in Singapore. The three Asian nations are among those best positioned to benefit from a weakening dollar as investors seek out higher-yielding assets and growth.

“My base case is that we still have at least one- to three years of more moderate dollar weakness on the cards -- that’s not going to change,” Seth said in a phone interview on Thursday. “Regardless of the election outcome, some of the policy actions have already happened.”

The $7.3 trillion giant joins global peers including Goldman Sachs Group Inc. and UBS Asset Management that favor selling the dollar with just a week to election day. On Monday, BlackRock strategists downgraded their views on Treasuries on growing likelihood of significant fiscal expansion under a unified Democratic government.

A Bloomberg gauge of the dollar has fallen over 1% this month as Joe Biden extended his lead in polls over President Donald Trump. The yuan has risen 1.4% against the dollar, Indonesia’s rupiah has gained 1.5% while India’s rupee is little changed.

The downtrend in the greenback may see a “temporary pause” depending on the election outcome, but its weakness is likely entrenched over the long term, said Seth.

“The dollar still is on the expensive side from a fundamental standpoint,” he said. “I don’t think that direction reverses or changes because of elections.”

Here some comments from Seth on other asset classes:

Credit Bets

There are three broad areas in Asia which look appealing -- high yield, China credit and private credit. Asian high yield overall looks attractive on both a relative and absolute basis compared to U.S. or Europe. We are also looking at illiquid opportunities in countries where there is a shortage of credit, but reasonable growth potential.

Asia Rates

In Indonesia, we do like the intermediate part of the curve so maybe toward the 10-year. In the case of China the positioning is broader so it is across government bonds, banks, higher quality state-owned enterprises, some local government and credit exposure. For India, it’s more toward the five-to-seven year part of the curve.

Downside Hedges

Rather than take a lot of duration risk at these levels in U.S. Treasuries, we are trying to overall look at portfolio structures, portfolio beta and cash levels. Nothing stands out cheap when you think of hedges today. Depending on the mandate and portfolio, we do look at a combination of CDS or equity options or FX for that matter as potential ways to hedge downside.

India Opportunities

We have a cautious and selective view in terms of our positioning in India given that the rebound after Covid shock is still at a very early stage. We do see the central bank potentially having room to ease further as we go into the next quarter. The gap in the on-shore credit markets provides some interesting investing opportunities for global investors. Especially in the illiquid space, we do see India actually providing fairly good opportunities along with China.

©2020 Bloomberg L.P.