BlackRock Searches for Hidden Gems in Europe’s Unloved Junk Bonds

BlackRock Searches for Hidden Gems in Europe’s Unloved Junk Bonds

(Bloomberg) -- As European high-yield bonds splinter around the haves and have-nots, BlackRock Inc. is planning to target riskier credits in a bid to secure market-beating returns next year.

“It’s finding diamonds in the rough that we think will present the best alpha generating opportunities in 2020,” James Turner, the firm’s head of European leveraged finance, said in an interview. The portfolio manager, who oversees $12 billion of bonds and loans, is also on the lookout for “oversold” names that have plummeted in price and that stand a chance of recovery.

Like many other high-yield investors this year, Turner said he has been underweight cyclical names and sectors due to end-of-cycle fears. But price dispersion among high-yield bonds is throwing up buying opportunities in areas that credit pickers have typically steered clear of.

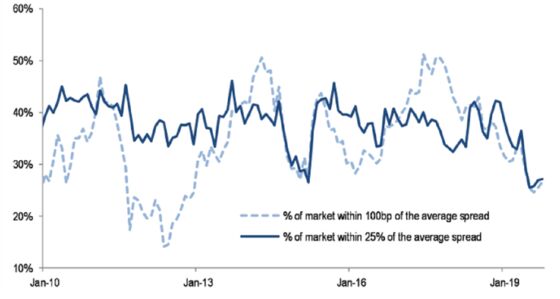

The proportion of notes trading with 25% of the high-yield index spread is close to its lowest level this decade, “which tells us that the high yield market has become extremely bifurcated,” JPMorgan analysts wrote in a client note last month. The large variance of monthly bond returns “reflects an opportunity for investors to generate (or lose) ‘alpha’ via stock selection,” they added.

“With the increased dispersion there are some cyclical names or names in less loved sectors with appropriate leverage that are coming onto our radar as good investments,” Turner said, adding that this strategy is more credit specific than industry focused.

This bifurcation is also on display in the new issue market where Eircom Finance DAC last month priced a euro-denominated senior secured bond with a 1.75% coupon. Meanwhile EG Group and Monitchem HoldCo 3 SA (CABB) printed secured bonds at 6.25% and 5.25%, respectively. All three issues have at least two single-B ratings.

“We’re still in a relatively low default environment, and while I think there will be a small pick up in defaults next year, when compared to historical levels defaults will still be low,” Turner said. “If you don’t believe there will be a recession in 2020, this could be a good time to start looking at names that have dropped in price or have had to come with a relatively high coupon.”

Credit Selection

For much of this year investors have shied away from buying names with higher leverage or weak credit ratings givenconcerns around slowing economic growth and rising defaults. Corporate defaults for European high-yield could rise to 1.8% from 1.1% currently by year end, and are expected to almost quadruple to 4.1% by August 2020, according to Moody’s Investors Service.

“Sub 2% returns won’t satisfy many high-yield investors over the long run so barring a huge sell off it’s unlikely the same strategy that’s worked this year will work next year,” Turner said.

But there are signs in recent months that investor caution is beginning to thaw. Casino Guichard-Perrachon SA managed to boost the size of its latest debt offering even though chairman Jean-Charles Naouri placed its parent company under protection from creditors in May. Similarly, Teva Pharmaceutical Industries Ltd. upsized its bond to about $2.2 billion despite potential liabilities from lawsuits earlier in the year related to the U.S. opioid crisis.

That’s not to say that the risks are not high for junk bond investors in Europe next year, given historically low yields and the late stage of the cycle.

“We still think there will be a number of credits that will struggle next year and we continue to be laser focused on avoiding the losers,” Turner said.

To contact the reporter on this story: Laura Benitez in London at lbenitez1@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.