Billions in Secret Derivatives at Center of Archegos Blowup

One reason for the widening fallout is the borrowed funds that investors use to magnify their bets.

(Bloomberg) -- The forced liquidation of more than $20 billion in holdings linked to Bill Hwang’s investment firm is drawing attention to the covert financial instruments he used to build large stakes in companies.

Much of the leverage used by Hwang’s Archegos Capital Management was provided by banks including Nomura Holdings Inc. and Credit Suisse Group AG through swaps and so-called contracts-for-difference, according to people with direct knowledge of the deals. It means Archegos may never actually have owned most of the underlying securities -- if any at all.

While investors who own a stake of more than 5% in a U.S.-listed company usually have to disclose their holdings and subsequent transactions, that’s not the case with positions built through the type of derivatives apparently used by Archegos. The products, which are transacted off exchanges, allow managers like Hwang to amass exposure to publicly-traded companies without having to declare it.

The swift unwinding of Archegos has reverberated across the globe, after banks such as Goldman Sachs Group Inc. and Morgan Stanley forced Hwang’s firm to sell billions of dollars in investments accumulated through highly leveraged bets. The selloff roiled stocks from Baidu Inc. to ViacomCBS Inc., and prompted Nomura and Credit Suisse to disclose that they face potentially significant losses on their exposure.

One reason for the widening fallout is the borrowed funds that investors use to magnify their bets: a margin call occurs when the market goes against a large, leveraged position, forcing the hedge fund to deposit more cash or securities with its broker to cover any losses. Archegos was probably required to deposit only a small percentage of the total value of trades.

The chain of events set off by this massive unwinding is yet another reminder of the role that hedge funds play in the global capital markets. A hedge fund short squeeze during a Reddit-fueled frenzy for Gamestop Corp. and other shares earlier this year spurred a $6 billion loss for Gabe Plotkin’s Melvin Capital and sparked scrutiny from U.S. regulators and politicians.

The idea that one firm can quietly amass outsized positions through the use of derivatives could set off another wave of criticism directed against loosely regulated firms that have the power to destabilize markets.

While the margin calls on Friday triggered losses of as much as 40% in some shares, there was no sign of contagion in markets broadly on Monday. Contrast that with 2008, when Ireland’s then-richest man used derivatives to build a position so large in Anglo Irish Bank Corp. it eventually contributed to the country’s international bailout. In 2015, New York-based FXCM Inc. needed rescuing because of losses at its U.K. affiliate resulting from the unexpected de-pegging of the Swiss franc.

Much about Hwang’s trades remains unclear, but market participants estimate his assets had grown to anywhere from $5 billion to $10 billion in recent years and total positions may have topped $50 billion.

“This is a challenging time for the family office of Archegos Capital Management, our partners and employees,” Karen Kessler, a spokesperson for Archegos, said late Monday in an emailed statement. “All plans are being discussed as Mr. Hwang and the team determine the best path forward.”

CFDs and swaps are among bespoke derivatives that investors trade privately between themselves, or over-the-counter, instead of through public exchanges. Such opacity helped to worsen the 2008 financial crisis and regulators have introduced a vast new body of rules governing the assets since then.

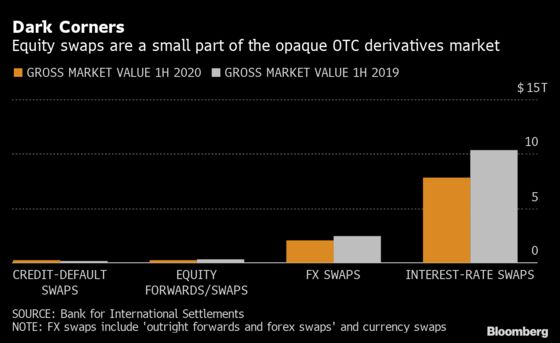

Over-the-counter equity derivatives occupy one of the smallest corners of this opaque market. Swaps and forwards linked to stocks had a gross market value of $282 billion at the end of June 2020, according to data from the Bank for International Settlements. That compared with $10.3 trillion for swaps linked to interest rates and $2.4 trillion for swaps and forwards linked to currencies.

Regulators have begun clamping down on CFDs in recent years because they’re concerned the derivatives are too complex and too risky for retail investors, with the European Securities and Markets Authority in 2018 restricting the distribution to individuals and capping leverage. In the U.S., CFDs are largely banned for amateur traders.

Banks still favor them because they can make a large profit without needing to set aside as much capital versus trading actual securities, another consequence of regulation imposed in the aftermath of the global financial crisis. Among hedge funds, equity swaps and CFDs grew in popularity because they are exempt from stamp duty in high-tax jurisdictions such as the U.K.

©2021 Bloomberg L.P.