Big Short Builds in U.S. Bonds on Wariness of Convexity Trigger

Big Short Resurfaces in U.S. Bonds, Wary of ‘Convexity Trigger’

(Bloomberg) -- Bond investors are piling back into short positions, motivated not only by the specter of inflation but also by the risk that yields are approaching a level that will unleash a wave of new selling by convexity hedgers.

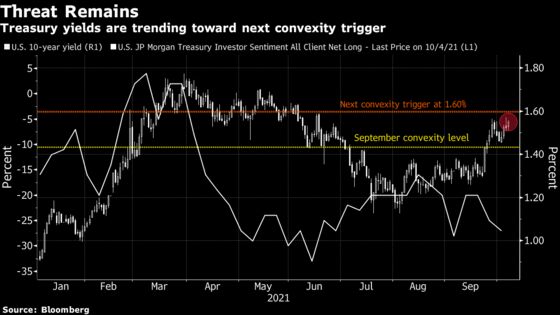

That level is around 1.60% in the U.S. 10-year Treasury yield, less than five basis points from its current mark and the highest since early June, according to Brean Capital’s head of fixed income strategy, Scott Buchta. It’s the midpoint of “a key threshold” in the range of 1.40% to 1.80%, an area “most critical from a convexity hedging point of view.”

Convexity hedging involves shedding U.S. interest-rate risk to protect the value of mortgage-backed securities as yields rise, slowing expected prepayment rates. It’s already begun to pick up as yields stretched past the 1.40% level. Another wave is expected at around 1.6% -- a point of “maximum negative convexity” in agency MBS, “where 25bp rallies and selloffs should have an equal effect on convexity-related buying and selling,” Buchta says.

Signs that short positions are accumulating include Societe Generale’s “Trend Indicator.” Among its 10 newest trades are short positions in Japanese 10-year debt, German 5-year debt futures, U.K. 10-year gilts, U.K. short sterling and U.S. 2- and 5-year notes. Meanwhile, CFTC positioning data for U.S. Treasury futures show asset managers dumped the equivalent of $23 million per basis point of cash Treasuries over the past week, winding up with a net short in the 10-year note contract. Hedge-fund shorts also remain elevated in the long end of the curve, as measured by net positions in Bond and Ultra Bond futures.

“Bond-bearish impulses remain in place,” Citigroup Inc. strategist Bill O’Donnell said in a note. Traders should be aware of short-covering rallies in the meantime. “Potentially extreme short-term positioning and sentiment setups could easily allow for a counter-trend correction under the right conditions,” he said.

U.S. 10-year yields topped at 1.57% this week, the cheapest level since June, spurring the breakeven inflation rate for 10-year TIPS to 2.51%, the highest since May. Friday’s September jobs report could add fuel to this inflationary fire, rewarding bond shorts.

©2021 Bloomberg L.P.